Archive for ‘Insurance’ Category

Lost & Found: Recover Unclaimed Money, Property, and Savings Bonds

Treasure Chest by Immo Wegmann on Unsplash

Treasure Chest by Immo Wegmann on Unsplash

There are many reasons to keep your paperwork organized, but I think the most compelling one is that many VIPs (very important papers) are the equivalent of money.

Your Social Security card, for example, is key to proving who you are, and if someone gets his or her hands on your card (or even just the number) and a little bit of other information, you may suffer from years of financial strife due to identity theft.

A lost last will and testament means that a family could have to spend months or years lacking access to resources promised to them because of the difficulty of proving the deceased’s intentions for funds and possessions.

If you lose your birth certificate, you may not be able to replace other essential documents if they go missing or get destroyed in a fire or natural disaster.

Lose your passport without enough time before an international trip, and your vacation or work plans could be scuttled, leaving aside the potential for identity theft of a more-than-financial nature.

Paper Doll has covered a wide variety of topics over the years on accessing lost documents, creating essential ones you lack, and keeping them all safe so they are not lost in the future. These posts include:

Ask Paper Doll: Do I Really Need A Safe Deposit Box?

How to Replace and Organize 7 Essential Government Documents

The Professor and Mary Ann: 8 Other Essential Documents You Need To Create

Protect and Organize Your COVID Vaccination Card

A New VIP: A Form You Didn’t Know You Needed

Today, we’re going consider options for recovering lost property. Consider it a treasure hunt!

RECLAIM LOST “PROPERTY”

When I say “property,” what do you think of? Perhaps real estate?

Maybe that reality show Property Brothers with Canadian twins Drew and Jonathan Scott?

When you hear “lost property,” it’s possible you think of the boilerplate language on one of those claim tickets you get when you leave your coat at the fancy coat check room at a swanky venue.

So What Is Unclaimed Property?

The term unclaimed property is what you’ll hear most often when searching for lost money in various types of accounts. Unclaimed property usually refers to funds that a government (federal, state, or local) or business owes you because you’ve, quite literally, left it unclaimed.

It’s possible that you’re so organized with your paperwork that you feel affronted that I’ve implied you might have just haphazardly left money sitting around. But I’m not saying you’re absent-mindedly leaving piles of cash wrapped in newspapers like Uncle Billy in It’s a Wonderful Life. (By the way, that $8000 deposit that ended up in Mr. Potter’s hands would be work $121,762 in 2023! Maybe Uncle Billy should have tied the money to one of those strings around his fingers.)

Thomas Mitchell as Uncle Billy, searching the bank’s trash cans for the lost Savings & Loan deposit.

There are all sorts of reasons money may get separated from its rightful owner.

Perhaps you put a security deposit down on an apartment when you were in college, but after graduation you were heading across the country to start your first job. Your roommate returned the keys to the landlords, got the OK that you hadn’t left the place in a horrifying state, and similarly disappeared into the adult world, leaving no forwarding address for either of you.

In many cases, by law, your security deposit was placed in an account (perhaps interest-bearing, perhaps not) and should have been returned to you when your lease ended. If your landlords were playing by the rules, rather than deciding to take the money and run, they should have turned it over to the state.

Similarly, it’s common to have to pay a deposit when opening an account for certain utilities. While some utilities keep these deposits until you move and close your account, others have (little-advertised) rules stating you can request your deposit be returned after a set period of good payment history. Sometimes, however, if you don’t actually request your deposit back, it just sits there, eventually going unclaimed, and being sent to the state.

When I helped one of my clients, a gentleman in his 60s, search for unclaimed property in his name, we found a life insurance policy that his parents took out in his name when he was an infant. It had long since stopped increasing in value, so he claimed it and cashed out.

Or maybe your Great Uncle Horace left you oodles of money in his will, but his last valid address for you was three states and 22 years ago? (My condolences on Horace. We always heard good things about him.)

Unclaimed property can be in the form of cash, uncashed checks (including stock dividends), insurance policies, abandoned bank accounts, forgotten security deposits, or even tangible property in the case of safe deposit boxes.

Life gets busy. It’s OK. Don’t play the blame game. Instead, play finders keepers and locate your missing money!

Where Can You Find Your Unclaimed Funds?

Unfortunately, there’s no central repository for all unclaimed property. Instead, you can search in each applicable state’s unclaimed property office.

Start with Unclaimed.org, the website of the National Association of Unclaimed Property Administrators.

Once there, scroll down and select your state by clicking on the location on the map. If you are from a United States territory like Puerto Rico or the U.S. Virgin Islands, or from one of several Canadian provinces (Alberta, British Columbia, New Brunswick, or Quebec), click on the appropriate link below the map, or use the yellow “Select Your State or Province” button. This will take you to a specific unclaimed property office, like the Office of New York State Comptroller’s Search for Lost Money page or Tennessee’s unclaimed property search (with a snazzy alternative address of ClaimItTN.gov).

To begin your search at any of these state sites, provide whatever information you have available, but at least a first and last name (or, if you’re searching money owed to a company or non-profit, the entity’s legal name). Some state search sites will also ask for a city in order to narrow the parameters.

If you want to search for multiple states simultaneously (let’s say you have lived in many locations, or you’re searching for abandoned accounts for a relative who has passed away and are unsure where they might have had lived), visit MissingMoney.com.

MissingMoney.com allows you to just type a first and last name, and all possibilities for that name, across all state databases, will come up.

Whether you use a state search or a multi-state search, the resulting page should provide a series of options. If you find a listing for yourself (or a relative), you’ll likely see some combination of the following information:

- the name of the owner of the unclaimed property

- any co-owner’s name, if applicable

- the last known address of the owner (possibly including the street address, city, state, and/or zip code, though some states hide some of the information)

- the state in which the unclaimed property is held (if you’re doing a multi-state search)

- the amount or value of money being held (which may be listed as an exact dollar amount, a range (like $50-$100, or >$500), or “undisclosed); if the property is tangible rather than monetary, you may or may not get a clue to what it might be.

How Do You Claim Your Funds?

If you find a match for unclaimed property on your state’s page or through MissingMoney.com, you’ll need to file a claim to prove that you own the account or property. Similarly, if you are claiming it on behalf of a relative who cannot act on their own behalf or a person who has passed away, you must prove their connection to the property as well as show that you are the party authorized to file a claim.

Whatever search method you choose, as long as you go through a government web site, know that searching for the unclaimed property is free, as is filing your claim. (Please don’t get scammed by a site promising to funds that are due to you anyway. While some services are valid and may relieve you of labor searching for large 5- and 6-digit recoveries, I encourage you to exhaust all free options first.)

Each state or province will have its own rules regarding claim submission. While most prefer you to submit your claim online, some still let you submit by mail. Answer all of the questions to the best of your ability, and assuming you are able to substantiate that you have a right to the funds, the account will be processed in due time and sent to you.

For individuals, businesses, and non-profits, you will have to submit proof of identity, address, and ownership. For individuals, your identity can usually be proven by a scan/copy of your driver’s license, passport, or Social Security number; please be cautious about transmitting your Social Security number through the mail and be sure you are using secure web sites marked HTTPS.

Proof of ownership of property will vary. Options might include your Social Security number, employment pay stubs, W2s or 1099s, or utility bills.

If you’re making a claim on behalf of someone who is living, you will need to provide the appropriate documentation, which might included a copy of a child’s birth certificate or legal adoption order (if the money is due to someone under 18), proof of a claimant’s age, and a court document or other signed legal documents proving you have the authority to act on the actual owner’s behalf. These could include letters of guardianship or conservatorship, a trust agreement, or a Power of Attorney document.

If you are making a claim on behalf of someone who has passed away, you’ll have to submit a death certificate as well as a will or other court documents, like a Small Estate Affidavit and a Table of Heirs. (These are state-specific.)

What To Do Once You Get Your Now-Claimed Funds?

After you submit your claim, if you are able to sufficiently able to prove your right to the funds, you will eventually be sent a check. Verifying your identity and rights to the funds can take a while, though many states try to complete the processing within thirty days.

Once you receive your money, usually by check, deposit the funds as soon as possible. Do not run the risk of losing the check and starting the whole process over!

Depending on the source of the funds, you may have to pay state and/or federal tax on the claimed money.

For example, if this is a deposit returned to you, you would not owe tax on the amount of your deposit, but tax might be due on any interest the account earned. The same is true regarding funds from abandoned bank accounts; the principal would not be income, but interest would likely be taxable. Of course, if the money would initially have been taxable had you received it on time (such as with stock dividends), it will still be taxable, but as income in the tax year in which you are receiving it.

What About Unclaimed Money in Other Countries?

Are you a fancy-schmancy world traveler? Maybe someone in your family lived abroad?

Unfortunately, there’s no central repository for tracking money left behind in your Tunisian bank account or a security deposit your mom paid during her semester abroad in Paris. (You may find some solace in the links collected by the Global Payroll Management Institute.)

However, the US government’s Foreign Claims Settlement Commission does oversee unpaid foreign claims for covered losses. That’s government-speak for money you are owed for lost funds or real property in the following circumstances:

- a foreign government “nationalizes” your property (whether that’s the money in your account or the house you owned)

- damage to property you owned that was caused by military operations

- injury to civilian and military personnel

If any of these apply to you, review the Unpaid Foreign Claims page and fill out a certification form (linked on that page). There’s also a link for Standard Form 1055, if you’re filing on behalf of someone who has died.

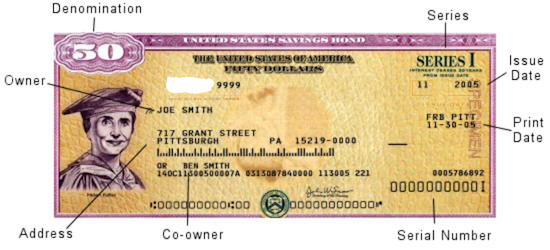

LOST SAVINGS BONDS

Once upon a time, it was popular to give United States savings bonds as gifts when people got married, had babies, graduated from college, got confirmed or Bar or Bat Mitzvahed, or otherwise had a rite of passage.

In ye olden days, you’d go to your bank to buy a savings bond, and get a receipt for your purchase as well as a paper certificate to give to the recipient. With the old EE savings bonds, you could purchase a bond at half the face value, and then a few decades later, your investment would double to the face value. If you waited a little longer, the bond would keep earning interest, at least for a while. (If your bonds are more than 30 years old, they have likely stopped earning interest.)

Nowadays, savings bonds are registered electronically, which makes everything much easier. However, with the old bonds, without the certificates in hand, the process gets complicated.

The problem was that these called SAVINGS bonds — but people often treated them as if they were called “throwing-them-in-a-box-hidden-under-the-bed” bonds. That’s fine for a while, but once your bond stops earning interest, it would make sense to cash it in and find another wise investment option. That’s hard to do if you don’t have the bond.

What Should You Do If You Can’t Find Your Savings Bonds?

If you’re sure you have savings bonds, but can’t find your paperwork, you have a few alternatives:

- Check your safe deposit box or fireproof safe — Free, except for the value of your time.

- Search through those boxes of stuff your parents or guardians gave you when they retired to Boca or Shadytime Retirement Village. Again, free except for the value of your time.

- Ask your family members to check their safe deposit box(es) and/or fireproof safe(s) and send you (via secure shipping) your bond certificates — Depending on whether you live across the street or across the country from your loved ones, this will come at variable cost in terms of their time, delivery service fees, and you getting roped into providing IT support for your parents now that they’ve got you on the phone.

- Contact the Feds — If you can’t find your bonds, or know they were definitely lost, stolen, or damaged, this may be your only alternative.

If you’ve lost your original savings bond’s nifty tangible certificate, you have two options:

- replace your original bond with a digital* bond (held in your Treasury Direct account); or

- cash in your bond (possibly losing value if you decide to cash it in before it has reached maturity)

*Note: If your lost bond is a now-defunct HH bond, you can get a substitute paper bond. For EE or I-series, they must be digital

If you’re really lucky, even if you’ve lost the actual bond, someone in your family may have kept track of the serial number of the bond. If not, you’ll have to help the government perform a search. Go to the U.S. Treasury’s website at www.TreasuryDirect.com and fill out Form 1048 to locate savings bonds registered all the way back to 1935.

Random Treasury Trivia

EE savings bonds took the place of World War II-era E-series or “Liberty bonds,” which date back to WWI!

HH-series bonds, popular as gifts for GenXers and Millennials, only came in the paper format and existed from 1980 through 2004, and they stop earning interest in 2024. That’s next year. Yes, really. So it’s a good time to start looking for your HH bonds! I-series bonds were introduced in 1998.

Interested in buying bonds but not sure how they work? Treasury Direct has a whole page comparing EE and I-series bonds. Be sure to check out the rules and options for buying savings bonds.)

On Form 1048, you’ll be asked to provide as much information as possible, including the:

- Issue date (or a range of dates, if you are uncertain)

- Bond certificate serial numbers (if you have them)

- Inscription information on the bonds, including names, addresses as Social Security numbers.

- Whether the bonds were lost, stolen or destroyed. If the bonds were stolen and a police report was made, you will need to append that, as well. The government wants to know all the gory details, so if your Great-Aunt Gertrude started a food fight at Thanksgiving and your savings bonds were drowned in gravy, explain. Or, y’know, explain if your town had a flood. Whatever.

- If you are not the named party on the bond certificate, you will have to explain your right to access the bonds; for example, are you the parent or guardian of a minor, the conservator or legal representative of another adult, or the executor of the will of a now-deceased party? (Note: if the person named on the bond is deceased, you will also need to include a certified copy of the death certificate.)

- Then, you’ll have to state whether you want substitute (digitally-held) bonds or payment in return for cashing in your bond.

You will need the form to be certified by a Notary Public. Review Paper Doll’s Ultimate Guide to Getting a Document Notarized for your options.

Finally, mail the form to:

Treasury Retail Securities Services

P.O. Box 9150

Minneapolis, MN 55480-9150

What If You’re Not Even Sure If There Were Savings Bonds?

All of the above tells you what to do if you know you received the bonds, but they’ve since been lost, stolen, or destroyed (as in irretrievably folded, spindled, or mutilated…or drowned in gravy).

But maybe you’re not sure if your hazily-recalled bonds ever existed? Maybe you (or someone on your behalf) purchased bonds but they never arrived. Maybe you got hit on the head with a falling anvil and can’t remember if you ever had a bond, or maybe you think a deceased loved one owned savings bonds but you can’t find them?

If any of the above situations apply, visit the Department of the Treasury’s Treasury Hunt link. Enter your (or your loved one’s) Social Security number and state, and if there’s a match, the site will let you know what to do next to locate matured savings bonds, those that are uncashed but no longer earning interest.

This just scratches the surface of the unclaimed funds, property, and financial instruments that can be recovered with a little bit of effort. Invest a few moments to let your fingers do the walking and see if you can recover what’s been lost.

If you DO find money owed to you, please come back and share the story (but not confidential information) in the comments.

Organize for an Accident: Don’t Crash Your Car Insurance Paperwork [UPDATED]

[Editor’s note: This post originally appeared on Paper Doll on 1/23/2020 and has been revised and updated as of 8/8/2022. As many college students are headed off or back to their universities with cars, this is an ideal time to discuss the finer points of auto insurance.]

(Image by Andrea Closier on Pixabay)

What happens when an unstoppable force meets an immovable object?

In January 2020, Paper Doll was sitting at a traffic light, preparing to make a turn, when the car behind me answered that physics question. Luckily, it was more of a THUD or a BAM than a CRUNCH. However, even the most minor of fender benders can be scary and overwhelming. It’s definitely not the time to wish you’d been more organized with your car insurance paperwork.

Even the most minor of fender benders can be scary and overwhelming. It's definitely not the time to wish you'd been more organized with your car insurance paperwork. Share on XToday, we’re going to look at the different kinds of paperwork you need, and how to organize it, to make sure you are protected and confident regarding your car insurance.

APPLYING FOR CAR INSURANCE

Whether you’re new to driving, are changing insurance companies, or are insuring a new car in your household, there are certain documents you’re going to need when you apply. Having everything in order ahead of time will make the process move more smoothly. You will need information about yourself, any other drivers covered on the policy, and the vehicle, such as:

Social Security Number(s) — You will need the SSN of anyone who is to be covered on your policy.

Your Driver’s License — Some insurance companies will only need the license number; more old-school agents may want a photocopy of your license. If, like me, you don’t like letting your license out of your hands, make a few photocopies of your license and you’ll have them when you need them.

Your insurance company isn’t just verifying that you are licensed to drive. They’re going to check your driving record — also called a Motor Vehicle Report (MVR) in some areas — to verify that your license hasn’t expired or been suspended, and to see whether you’ve had any accidents, convictions, or traffic violations. Most states look at your driving record for the last three years; however, there are exceptions. Kansas and New Jersey reports go back five years; Colorado, Indiana, and West Virginia look back seven years.

WalletHub has a state-by-state guide to getting a copy of your MVR, with links, in case you want to check it for accuracy before seeking insurance. In my state, I can get a copy for $5 in person or or online; nationwide, costs range from $2 to $25 (sometimes plus processing fees to use debit/credit cards) per report. Be prepared to use an authentication app, like Google Authenticator, or receive a text or email or verify your identity.

Do not be scammed into using a non-governmental service that promises to get your MVR online for you; they up-charge a significant amount and are usually not any faster than going through your state’s website.

Financial History — Insurance companies do standard credit checks, so it’s a good idea to check your credit history at AnnualCreditReport.com (and not one of the shady copycats), as well as your credit score, to make sure there are no mistakes.

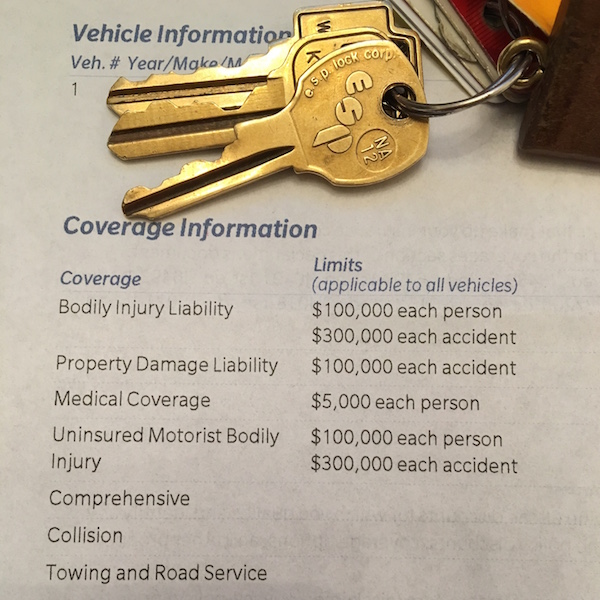

Your Current Insurance Declarations Page – You know that long page (or set of pages) in your policy with big numbers like $300,000/$500,000? (More on that, below.) Having that page will allow your new insurer to provide you with an apples-to-apples quote.

Vehicle Information Number (VIN) — This 17-character identifier is unique to your car and is built into your dashboard or imprinted in your driver’s side door frame. Your insurer uses this to verify that the car is not stolen and doesn’t have any problematic history.

Discount-Related Paperwork — There are a variety of ways to get a discount on car insurance. Your driving record (MVR) will verify if you qualify for a “good driver” discount, and you (or your teenager or college student) may be able to submit a current report card to qualify for a “good student” discount. To get the discount, students usually need to be under 25 and have no at-fault or moving violations on their MVR. A GPA of 3.0 (on a 4.0 scale) or Honor Roll/Dean’s List status is generally required.

You can also get multi-car discounts if you and your spouse both have cars, or multi-policy discounts if you carry homeowners’ or renters’ insurance with the same company.

If you’re over a certain age, you may be able to take a safe driver course, like one offered by AARP, to lower your rates.

You might be eligible for affinity discounts if you are a member of certain clubs, organizations, alumni associations, or sororities/fraternities. There are also often occupational discounts for members of certain professions, including first responders and medical professionals, educators, and government employees, so it’s worth asking your agent what discounts exist before you get too far in the application process.

ORGANIZING YOUR INSURANCE PAPERWORK

Once you have an auto insurance policy in place, you’re going to have paperwork. The more organized you can be, up-front, the less stress you’ll have to deal with in case of an accident or other issue.

Policy

This is the multi-page legal document that tells you everything about your coverage. It can be overwhelming. Make sure you go over it with your insurance agent so that you know and understand the essential elements of your policy, particularly the items on your declarations page, which spells out your coverage:

- Liability (also called Bodily Injury Liability) — These are the limits on your policy per person per accident. You may see $100,000/$300,000, which means you’re covered for any medical expenses and/or lost wages for anyone (including other drivers, passengers, and even bystanders) injured in an accident you cause, up to that amount.

- Property Damage — This pays to repair or replace things that get damaged (in an accident you cause), like other people’s cars, items in their cars that get damaged, actual property (like someone’s garage or mailbox). The dollar limit is quoted per accident. Be sure you understand the difference between collision and comprehensive. Collision covers damage to your car when it collides with another car, or a tree, or a Bob’s Big Boy. Comprehensive covers damage to your car caused by things like vandalism or theft by hooligans, or “natural” disasters (hail, tornadoes), a tree toppling onto your car, or Bambi taking a running leap at your hood.

Your policy may combine liability and property damage into one category, so you might see it listed with three numbers, like “100/300/50” which means $100,000 for injuries per person, $300,000 for total injuries per accident, $50,000 for damages to property.

Depending on your state, your policy may also have (or even require) special types of insurance options, like:

- Uninsured and underinsured motorist coverage — If someone hits you but doesn’t have enough (or any!) insurance, it will cover injuries if you or your passengers get hurt. Basically, you’re insuring yourself against people who aren’t responsible enough to have (enough) insurance. There’s also a line item for uninsured motorist property damage; as you may have guessed, it covers your car if the person who hits you doesn’t have insurance.

- Personal injury protection insurance (PIP) — If you live in a “no-fault” state, this pays out for medical expenses for minor injuries or lost wages for you or your passengers. (Liability coverage is only invoked if the costs go beyond what PIP covers.)

- Medical payment coverage — Like PIP, this covers you or your passengers’ accident-related injuries, no matter which driver is at fault. It doesn’t cover lost wages, and the limits tend to be $5,000-10,000.

Your policy may also cover things like glass replacement damage, towing and road service, accident forgiveness (to keep your rates from going up after an accident claim) and loss of use (for a car rental while a vehicle is being repaired).

I encourage clients to make a file folder for each insurance policy they own (auto insurance, homeowners, etc.) and keep it in the Legal section of your Family File System.

The declarations page is a good cheat sheet for all of your coverage. You may want to make a photocopy and keep it in your glove compartment, or take a photo/scan to save in Evernote, Dropbox, or a similar app accessible on your phone.

Notes for Canadian Readers

Please note that all of the above refers to purchasing auto insurance in the United States. In Canada, different language is used. For example, in addition to provincial and territorial mandatory coverage, there are optional policies including “collision, specified perils, comprehensive, and all perils.” If you are seeking information regarding auto insurance (and organizing insurance paperwork) in Canada, please confer with an insurance professional (or a member of Professional Organizers in Canada).

Bills for Premiums

Insurance companies usually give you the option of paying annually, twice per year, or monthly. The less often they have to invoice you, the more likely you are to get a discount, so paying every six months can save you a bit over monthly bills.

If you receive paper bills, mark the payment date, amount, method of payment (and confirmation number, if applicable) on the invoice and file it in the Financial section of your Family File System.

If you tend to go paperless, print a PDF or take a screen shot of the confirmation screen and keep it in a “paid invoices” folder on your computer, and be sure to able it clearly, like “2022-May Ins-Car.”

Re-shopping Insurance Policies

In April 2022, I made a few calls to investigate the rates of competitive auto and rental insurance policies. When I found an auto policy that was significantly lower than what I’d been paying (while not increasing my associated renter’s policy) for an equivalent policy with an equally reputable insurance company, I contacted my agent.

I was surprised, delighted, and then admittedly annoyed when my agent “magically” found me an even more competitive rate. (A reminder: companies generally do not go looking for ways to reduce consumer costs!) However, even though I was staying with my same insurance company where I’d been for 24+ years, my policy was technically with a new sub-company, and my “accident forgiveness” guarantee went away, as if I were a new policy holder. However, I was able to retain that status with a $20 one-time fee. Caveat emptor!

So, do consider shopping for better rates/discounts at least every couple of years. It’s not fun, but it’s not as inconvenient as you might imagine. If you like your current insurance agent/company, give them the opportunity to surprise, delight, and slightly annoy you by magically finding better rates.

Proof of Insurance Cards

This little card has your name and address, your car’s VIN, make, and model, your insurance company’s name and contact information, and your policy number. It is the only document that verifies the coverage on each of your cars, so keep your proof of insurance somewhere safe in case you need to present it to a police officer or someone with whom you’ve had a driving “misadventure,” or to have information handy if you need to file a claim or report damage to your insurer.

Most insurance companies provide two proof of insurance cards on one piece of paper with your policy renewal. Consider putting one in your wallet and one in your glove compartment. If your glove box is not always tidy, you may want to consider something that keeps important documents front and center, like this car insurance and registration card holder in a bright color.

fashion-forward options, like this sparkly one (available in black, pink, purple, rose gold, and silver).

I also encourage clients to take a photo of your proof of insurance card and keep it in the cloud, accessible via your cell phone in Evernote or Dropbox. If you tend to drive places where cell service is spotty, consider keeping it in a “VIP” album in your photos app.

By the way, most insurance companies now provide official proof of insurance inside your account on the website or the app, but I wouldn’t leave that as your only proof. If you are stopped by a police officer, or worse, in an accident, you don’t want to be at the mercy of wonky internet access.

Other Info

Right now, take a moment to put the following numbers and URLs in your phone:

- The police non-emergency line – if you have a minor fender-bender, there’s no need to call 911.

- Your insurance company’s Claim Filing telephone number. Most insurance companies have a 24/7 line to call if you’ve been in an accident. The Insurance Information Institute and BC Law Review maintain lists of most auto insurers’ telephone numbers for filing a claim. (This also may be useful if someone else causes your car damage; if another driver drags his feet about contacting his insurance company, or tries to convince to go to his cousin’s body shop or proposes some other hinky option, be prepared to call his insurance company to ensure things are handled on the up-and-up. Yes, I’m speaking from experience.)

- AAA or any other auto club’s number, URL, or app will make it easier to quickly call for a tow.

- Your insurance company’s direct claim filing/tracking URL – Navigate to your insurance company’s website, look for the “file a claim” link and bookmark it in your browser’s bookmark/favorite bar to find it quickly. While you may love your agent, she may not love you if you call her at 2 a.m. Most claim-filing departments have representatives on duty 24/7/365.

- The link to this post — Keep this link handy, if for no other reason than to avail yourself of the advice in the next section, should you need it.

WHAT TO DO IN CASE OF AN ACCIDENT

Photo by Praveesh Palakeel on Unsplash

Photo by Praveesh Palakeel on Unsplash

- Take some deep, calming breaths. My bumper tap was minor, but I still felt shaky. Don’t get out of your car until you feel steady.

- Pull over slowly to get out of the stream of traffic. Turn on your hazard lights. (If you’ve never had to use your hazards before, go check to make sure you know where they are! Ask your teen drivers to do the same.) If you can’t move your car out of the flow of traffic, get all passengers to a safe spot until emergency vehicles arrive.

You might want to consider getting emergency flashers/road flares to make sure the people and cars are safe and that other vehicles can see what’s going on.

- Assess any injuries requiring urgent assistance (your own, and that of your passengers, anyone in the other car, and bystanders, if applicable).

- Call the police and, if appropriate, 911 for medical care. Assuming the other driver is not belligerent or under the influence, call the non-emergency police line to report the accident and request that a police report be taken. (Your insurance company will need documentation of the accident.)

- Exchange information — Get the other driver’s name, contact details, and insurance information. (Taking photos of someone’s proof of insurance and driver’s license is faster than writing it down and you can text those photos to your insurance agent.) Take photos of your car, the other driver’s car, the situation, and road conditions. If it’s a serious accident, ask witnesses to provide their contact info or to stay around until the police arrive.

- Call the claims number and/or your insurance agent if you want to file a claim. Even if you weren’t at fault, you may wish to call your agent, just to put yourself at ease and ensure that you haven’t missed any steps.

As I often say, being organized can’t prevent all catastrophes, but it can make them less catastrophic. Organize well. Drive safely.

Paper Doll’s 10-Minute Tasks to Make Difficult Moments Easier

Lately, I’ve been considering that it’s a bit ironic that February, the shortest month of the year, is National Time Management Month. We collectively assign the month with the fewest days to figure out how to achieve goals that would solve so many frustrations.

Wouldn’t a 31-day month be better for that?

A Necessary Caveat About “Time Management”

Time management, obviously, is a misnomer. We don’t really manage time, which is fixed. Every person gets the same 60 seconds every minute, the same 60 minutes every hour, the same 24 hours every day, and of course, 525,600 minutes in a year.

(With apologies to all of you who’d rather watch the Broadway version, linked above, than Glee‘s, but YouTube is really cracking down on music videos being played anywhere but their own platform.)

Rather, we must try to manage our attention, our energy, and our labor. Though we have the same amount of time, none of us has the exact same quality of our time, nor the same obligations.

The single, healthy, unencumbered twenty-something with a salaried office job has more (financial, as well as temporal) resources than the mom of two working multiple retail jobs, or the person going to school while taking care of an elderly parent, or the individual struggling to make it through these crazy times with a chronic illness, visible or invisible.

Often, when the media has articles on time-saving tasks, they fail to acknowledge the complexities of life. If you are beyond the juggling and are full-on struggling, we professional organizers and productivity consultants see you. And we know that when the you-know-what hits the fan, you’ve got limited energy and time to deal.

So, today’s post has ten-minute tasks (or projects that can be handled as a series of ten-minute tasks) that will make things easier for you and your family when things get “ouchie.”

Check and Update Your Beneficiaries

You don’t even have to do these all at once, though if your paperwork is already organized, it should only take you a couple minutes for each. Though the time investment is small, the ease of mind it will bring (both now, and in the future) is tremendous.

And yes, you can even consider these two separate tasks (the checking and the updating) so you can make two different checkmarks on your task list.

Pull out the file folders or head to your online accounts and check to see who you previously listed as your primary and secondary beneficiaries for any of the following you may have:

- life insurance policies

- annuities

- pension accounts

- Individual Retirement Accounts (IRAs)

- 401(k)s, 403(b)s, and other retirement accounts

- profit-sharing plans

- brokerage/investment accounts

Obviously, a beneficiary is someone who gets a benefit. When we’re looking at financial documents, beneficiaries are the people (or sometimes entities) that the account holder designates as the recipient of any assets in that account when the account holder eventually shuffles off this mortal coil. (I know, nobody likes to use the world “death” or think about it, but that’s why we have life insurance policies, wills, and similar accounts and documents — to make things easier when someone has passed away.)

“The Reading of the Will” — central to any good murder mystery

In most cases, setting a beneficiary (and usually both a primary and secondary beneficiary) is part of the required paperwork. Some states (usually “community property states”) require you to list your spouse (if you have one) as your primary beneficiary for retirement and other accounts.

You may be wondering, if you have a will, why do you need to name beneficiaries? That’s a darned good question.

The main reason is that when a person dies, a will goes through “probate,” a legal process where the court in your jurisdiction supervises all the assets in your estate getting distributed hither and yon. Depending on the situation, it can be murky and complicated, and take a long time, which is pretty miserable if your people need those funds.

However, whenever you have a beneficiary set in your insurance policies and various financial accounts, that money can go straight to your intended recipient as soon as the insurance or financial institution gets proof that you are no longer among us. That usually just amounts to a certified copy of the death certificate and some proper ID.

If you set your beneficiaries for any of these accounts several years ago, you may have picked someone no longer appropriate — parents who are no longer living (or not able to manage their own finances), former spouses or significant others, or even friends who are not part of your active life anymore.

I went through the “check the beneficiaries” process with one client who was shocked to realize that she’d never gone back to revise the beneficiary on a small 401(k) plan she’d never bothered to roll over from a job decades earlier. (Note to readers: don’t do that. Roll over your retirement accounts so you don’t have to hope your former employers have stayed solvent and managed your funds properly.)

Imagine my client’s shock when she realized that her [expletive deleted], [expletive deleted]ing [expletive] of a [expletive deleting] ex-[expletive deleted] husband was still her beneficiary! Be assured it did not take her ten full seconds, let alone minutes, to get cracking on changing that beneficiary!

Imagine my client's shock when she realized that her *expletive deleted*, *expletive deleted*ing *expletive* of a *expletive deleted*ing ex-*expletive deleted* husband was still her beneficiary! Share on XIf you never set your beneficiaries before or your want or need to change them, you’ll need a few pieces of information, like their Social Security numbers, birth dates, and contact information (like phone numbers, email addresses, and mailing addresses).

EXTRA CREDIT: Here’s a time-saver so you don’t have to go through this entire process in the future:

- Create a spreadsheet (or even a handwritten note) with the first column listing all of your account names.

- Create a column and list all of the beneficiaries as they stand now.

- Create a column entitled “as of” and list today’s date.

- Any time you acquire a new policy, add a line to this list. Any time you revise a beneficiary, revise the spreadsheet.

This way, whenever you’re not sure whether you’ve updated your beneficiary, you’ll only have to look in one place.

EXTRA, EXTRA CREDIT: Checking your beneficiaries is easy and quick. Changing/updating them should be easy, but how quickly you can accomplish it depends on whether your insurance or financial institution will let you do this all online. But making this list is definitely easy and quick.

However, to take it a step further, fancy-up this spreadsheet with another ten-minute (or so) task.

Add columns for your account number, and the name, email address, and phone number of your insurance agents and financial brokers associated with each policy or account. Create a column to explain what kind of policy or account it is. And then make sure that someone you trust, like the person who has your Power of Attorney, has a copy or can access it when/if necessary.

Put Your Emergency Contacts On Ice

“Downtown Hospital Ambulance” by sponki25 is licensed under CC BY 2.0

In the early 2000s, first responders in the UK started suggesting that people list their “In Case of Emergency” contacts as “ICE” on their cell phones to make those contacts easy to locate. The idea quickly took hold in North America.

While first responders, themselves, generally don’t have the time (or authorization) to contact someone for you, nurses and hospital staff often do need to obtain important medical information when you are not able to provide it. That’s where your contacts come in.

As cell phones got fancier, the lock screens made accessing ICE contacts more difficult, but now, even if you are not able to respond, medical personnel may be able to use your thumb print access or facial recognition to get your emergency contact info.

But there’s something else you can quickly do to make sure your emergency contacts can, um, get contacted. Add your emergency contacts to your cell phone’s lock screen.

On an iPhone:

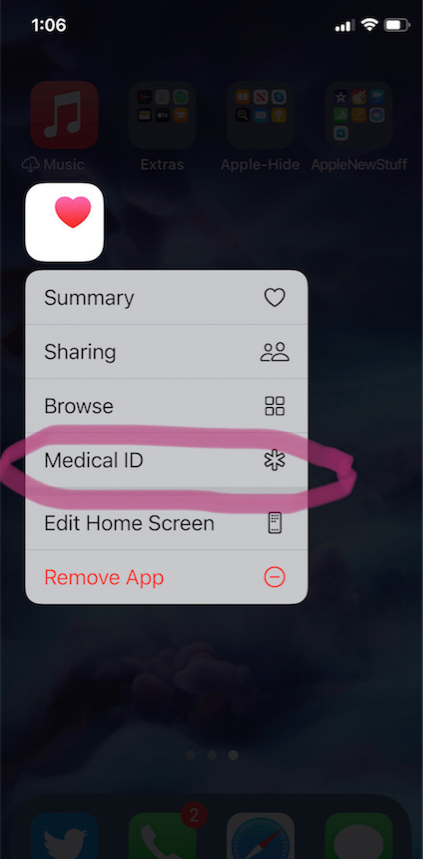

1) Go to the Medical ID screen. You can get there one of three ways:

- Long-press on the Health app icon. That will bring up a screen that looks like this:

- You can also manually open the Health App by tapping on it, then on your profile image, and then selecting Medical ID.

- Or go to Settings, then Health, then Medical ID.

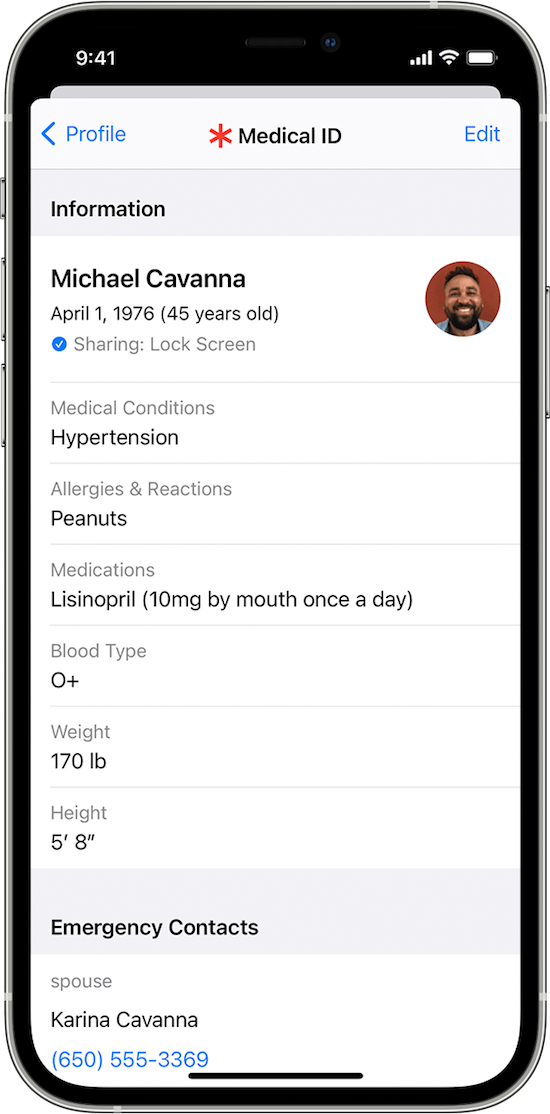

2) Tap Edit.

3) Fill in all the fields that you want, but if there’s nothing significant, it’s better to type “none” than to leave it blank (so that you’re not leaving anything open to interpretation). There are fields for medical conditions, allergies, medications, blood type, weight, height, and emergency contacts. (Bingo!)

At the top, there’s an option to put in your photo. Do that; it ensures that an emergency responder can verify this is your phone.

4) Choose a name and phone number (or two names and numbers) for your Emergency Contact(s). Be sure you select names/numbers that already exist in your contacts list.

5) Scroll down to the section for Emergency Access.

6) Enable “Show When Locked” and “Share During Emergency Call.”

7) Tap “Done” at the top right corner to save your info.

Now, go look at your lock screen. You should see the word “Emergency” in the lower left corner of your iPhone. If your phone is locked and someone taps that, they can see your emergency information but nothing else.

If you don’t see the word “Emergency” there, hold down your power button (or power and volume-down buttons) as if you were going to turn off your phone and you’ll see the Medical ID access. (I guess it all depends on which version of iOS you’re using.)

For more information about the iOS Medical ID, Apple has a detailed page of instructions and explanations.

Assuming you have a photo somewhere on your phone to add in the photo field, this can usually be completed in well under 10 minutes. (The only sticking point is if someone has many medications or allergies they have to list.)

On an Android Phone

Although Android phones do not have one default health-related app, you can easily show your emergency contacts on your lock screen in one of two ways.

Method #1

- Open your Settings app.

- Tap “User & Accounts” and then select “Emergency Information.”

- Tap “Info” and then “Edit information” to enter any medical information you want to store.

- Tap “Add Contact” to add a person from your contacts list. Note, you might have to click on “Contacts” first to be presented with the list

Method #2

Android phones will let owners put any message directly on the lock screen.

- Open your Settings app.

- Tap “Security & Location.”

- Tap “Settings” next to “Screen lock.”

- Tap “Lock screen message.”

- Type your primary emergency contact (and, if applicable, any medical conditions). You could type, “In Emergency, call Lin-Manuel Miranda” and his number. What? Can you think of someone more comforting to have around in an emergency? OK, maybe Stanley Tucci. Or Paper Mommy.

- Tap “Save.”

After you’ve set this up, your ICE information can be found by swiping upward on the lock screen and tapping EMERGENCY and then “Emergency information.”

Do An Inventory of Your Essential Documents

An emergency is the worst time to realize you have no idea where your important documents are. Do you know which of these documents you have and where you can find them?

- Birth Certificate

- Social Security card

- Marriage License and Certificate

- Divorce Degree

- Military Separation Papers

- Death Certificate

- Passport

- Durable Power of Attorney for Finances

- Healthcare Proxy or Durable Power of Attorney for Healthcare

- Living Will or Advanced Medical Directive

- Last Will and Testament

- Digital Will

- Driver’s License

- Voter Registration card

- Vaccination Record

- COVID Vaccinate Card

- Professional license(s)

- Other licenses

As with the beneficiaries section above, a great way to save time is to make a list (think of it as a treasure map) of where each of these documents are located. Use Excel or a Google spreadsheet and take note of what the document is and where it’s located (e.g., your family filing system, fireproof safe, safe deposit box, wallet, etc.).

EXTRA CREDIT: For good measure, for your passport, driver’s license, and any other licenses, take note of the expiration date.

And then for really good measure, put a reminder task in your phone to alert you one month before your any of these items expire to make sure you address renewals. (Give yourself a longer lead-time to renew your passport; also, as you’ve probably not been traveling out of the country in the last two years, you should check to make sure your passport hasn’t already expired.)

If you have a lot of documents, just do a few every day and you’ll be amazed at what a few ten-minute tasks can do to put your mind at ease.

EXTRA, EXTRA CREDIT: The Paper Doll archive has extensive information about what documents you should have and what to do if they’re missing. These posts are a great place to start.

How to Replace and Organize 7 Essential Government Documents

How to Create, Organize, and Safeguard 5 Essential Legal and Estate Documents

The Professor and Mary Ann: 8 Other Essential Documents You Need To Create

Protect and Organize Your COVID Vaccination Card

Paper Doll acknowledges that I write longer-than-typical blog posts. Feel free to consider reading each one to be a 10-minute task. But the knowledge you gain will contribute to your ability to use your time more efficiently. Because, the more you know, the better prepared you are for any eventuality.

Snap Some Photos to Take Key Information With You

Unlike the vital documents listed in the prior section, there are some pieces of information you are more likely to lack at the most inconvenient times.

Toy car accident image by Andrea Closier on Pixabay

For example, if you have an auto accident and the police or first responders won’t let you get back into your car for safety reasons, you wouldn’t be able to get your auto registration and car insurance paperwork out of your car. Yes, you’d have it at home, but that would slow everything down.

Or perhaps you need to fill a prescription at a different pharmacy from usual, perhaps when you’re on vacation, and they don’t already have your pharmaceutical company discount card on record.

Or maybe you’re unexpectedly with your spouse or child or senior parent in the emergency room, and the physicians want to know what medications, at what dosages, prescribed by what healthcare providers, the patient is taking. If that information is pinned to the fridge at home, but you came directly to the ER from somewhere else, that’s frustrating.

This is where the magic of modern cell phones (which we usually bemoan for the time they steal from us) comes in handy. Consider any of the following:

- auto registration form

- auto insurance card

- health insurance card

- homeowner’s insurance card

- pharmaceutical company discount cards

- handwritten instructions of how to get to a room or office you visit infrequently

- a list of the size/type of batteries and light bulbs you use for which items in your home so that you never again have to unscrew a light bulb just to know what voltage and whether you want a skinny-base or a fat-base bulb)

- etc., for whatever is important in your life.

You could snap all of these as photographs and store them in a photo album in your phone’s photo section. Name it “Remember” or “Vital” or whatever will catch your eye.

If you want to go to the effort of scanning the document and sending it to your phone, that’s fine, but iOS has created an easy option using the Notes app.

- Open a new or existing note.

- Tap the cute little camera icon.

- Tap “Scan Documents.”

- Focus your document, card, medicine label or whatever within your camera’s viewing area.

- Then you have two options:

- Let the auto-capture work its magic as the item comes into the viewfinder and auto-focuses, or

- Click the shutter button (or one of the volume buttons) to capture the scan

- Drag the corners of the scan to do any necessary adjustments.

- Tap “Keep Scan.”

- Scan more fiddly stuff to keep it handy or tape Save if you’re done.

From here, you can save the scan in your Notes or Files app in your phone itself, or upload it to a synced app, like Dropbox or Evernote:

As an all-Apple user, I don’t have an Android-specific scanning suggestion; if you do, please add your voice in the comments.

The next time a new insurance card or other piece of important information comes your way, take a snapshot or scan to ensure you’ll have whatever you might need when you are out and about.

As I often say, organizing can’t prevent all catastrophes, but it can make many of them less catastrophic. I hope these various ten(ish)-minute tasks will help ease many of the ickier moments in life for you.

Paper Doll Wraps Up, Declutters, and Updates 2020

It’s been quite the year. “Unprecedented,” you might say. (Or, better yet, let’s not say. How about we purge that word from our vocabulary?) Before we turn the calendar page to 2021, there are a few additions and updates for the posts you read (or might have missed) over the past year.

PANDEMIC PRODUCTIVITY

The Now Normal: When the New Normal Changes Quickly

Back in March, none of us knew what the next nine months would bring. I’d acknowledged the difficulty of being at home, whether that meant working from home, home-schooling, or dealing with family and their foibles 24/7, and noted that at least, to some extent, we’d get used to it, or at least we’d have to get used to the “Now Normal” of things constantly changing and us not getting used to things. Little did we know how long (how very, very long) we’d be getting used to things constantly changing. I gave you all permission (as much as anyone needs permission from random internet bloggers) to be OK with not being OK.

Now, on the cusp of 2021, there’s light (in the form of a vaccine) at the end of this tunnel. But I suspect things will never go back to exactly where they were. Remote work had already been increasing (by 173% between 2005 and 2018); 2020 gave companies the impetus to make this a more permanent option. Companies that had believed workers could never be as productive when working remotely found that the opposite was true. According to research collated by Apollo Technical:

- Performance can improve up to 13% when working remotely (in a quieter, more convenient workspaces)

- Remote work yielded greater worker satisfaction

- Remote workers spend 15% less time avoiding work tasks

- Anecdotally, once supervisors trust the work-from-home approach and stop micromanaging, productivity increases.

This doesn’t mean we can extrapolate only good things to come out of more people working from home. Even once children and life partners are no longer in the home/work space, the distractions of household tasks (especially for women) will likely adversely impact productivity, and research indicates that productivity may take a hit due to prolonged lack of social interaction (especially for extroverts, like moi).

Some workplaces will stay 100% remote; others will return to traditional venues; and I suspect many employees will demand greater flexibility, and companies will want to consider the reduced overhead associated with smaller (or no) dedicated offices. The only thing we know for sure is that things will continue to change, and we’ll have to be nimble, accepting that the sand will keep shifting under our feet. As L.P. Hartley once wrote, “The past is a foreign country; they do things differently there.”

The only thing we know for sure is that things will continue to change...As L.P. Hartley wrote, 'The past is a foreign country; they do things differently there.' Share on XPaper Doll’s Ultimate Guide to Organizing a Virtual Field Trip

This post proved to be one of the most popular during the early pandemic. Organizing our days to include breaks, including virtual day trips to escape monotony, became a necessity this year, and rarely a week went by when a reader did not email or tweet or post to tell me about other cool virtual field trips.

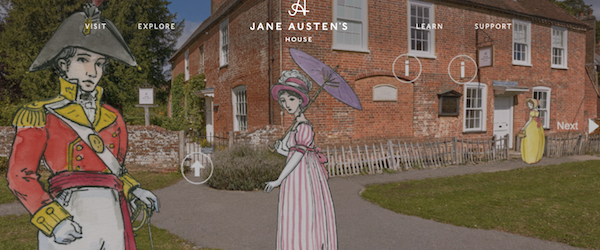

Friend of the blog Janet Barclay knows that Paper Doll is a consummate Jane Austen fan, and forwarded Celebrate Jane Austen’s Birthday With a 360-Degree, Interactive Tour of Her House, and from there it was a quick hop, skip, and virtual jump to the Emma Thompson-narrated Twelve Days of Christmas special. There are also paid live virtual tours of Jane Austen’s House from Home, trails, and exhibitions. (Two live tours in January each go for £5, or about $6.78).

Discovery Education has developed a variety of live and on-demand, family-friendly interactive field trips. Each is free and includes a companion guide with hands-on learning activities! Take your kids to “visit” the Johnson Space Museum in Houston, see the cars of the future, hobnob with polar bears in the Tundra, and so much more. Whether you need a virtual field trip to break up winter vacation, quell home-schooling doldrums, or reverse just too little play time, Discover Education is a delightful addition to the options in my post.

Perhaps you binged too much of The Crown and need a reality check? Take a virtual tour of Buckingham Palace. Prefer a different venue? How about the Taj Mahal, the White House, or the Vatican?

Virtual Museums started an interactive map of the world’s museums available to virtual visitors. (Create an account to track and rate your visits.) From the Canadian Museum of Human Rights to South Korea’s National Museum of Modern and Contemporary Art to the mysterious fossils of the Graz Natural History Museum in Austria, new field trips for grownups are appearing all the time.

And if you need the the kind of field trip that takes you away from the hubbub, Escapista may be to your liking. Escapista has developed a manifesto to explain its approach to selecting opportunities for immersive meditative experiences, from pausing by a snowy river to Norway’s “Slow TV” experience of ten hours on a train. (Click the speaker icon to turn on the audio.)

Be sure to organize time in your life to relax and to learn for fun.

Does Anybody Really Know What Time It Is? 5 Strategies to Cope With Pandemic Time Dilation

There’s an irony of mentioning time dilation between two long weekends marked by Christmas and the new year. I’ve lost count of how many people have told me they checked for the mail on Friday or took the trash to the curb on the wrong day.

In the original post, I explained why our body clocks became so borked during our quarantine and recommended five strategies, with LOTS of tactical suggestions, for keeping everyone from becoming unstuck in time:

- Put structure in your life.

- Enhance novelty.

- Create vivid sensory clues for the passing of time!

- Get what you know you need! (Daylight, sleep, exercise, and for those of you who’ve had the same pair of sweats in rotation since St. Patrick’s Day, get dressed!)

- Take a technology break.

As a professional organizer and productivity coach, my job is to help people get more out of their time. But efficiency isn’t everything. In a year like we’ve had, and going forward, some daydreaming and navel-gazing preserves sanity. If you find yourself losing track of time too often, add in a bit of structure to your day and use technology to get a quick “beep-boop.” But do give yourself permission to enjoy the one small benefit of this year, living by your natural body clock.

Organize Your Health: Parental Wisdom, Innovation, and the New Time Timer® Wash

Don’t touch your face. Wear a mask. Wash your hands. It’s good advice, so listen to your mom. Listen to mine.

READING RENEWAL

12 Ways to Organize Your Life to Read More — Part 1 (When, Where, What, With Whom)

I’m not the only embracing tips for reading more. Oprah, the ultimate book club leader, may have ended her print magazine, but the December issue offered up 20 Simple Ways to Read More and Enjoy More Books in 2021. (Personally, though, I preferred my take on developing a reading nook. What do you think, readers?)

12 Ways to Organize Your Life to Read More — Part 2 (Reading Lists, Challenges & Ice Cream Samples)

Want to read more in 2021? You’ve got a bounty of options for finding recommended reading lists. One of my favorites is the NPR Book Concierge. (Find annual suggestions going back to 2013.)

If, instead of looking for a specific title, you want to find a 2021 reading challenge that, well, challenges you, opportunities abound, including:

The Uncorked Librarian (Most intriguing suggestion: read a book set on a train.)

Modern Mrs. Darcy (This year, it’s not just reading prompts, but an entire interactive kit for creating your personalized reading life!)

GirlXOXO Master List of Reading Challenges (While I’ll skip the challenge to read mysteries with cats as main characters, there are certainly lists galore for every taste!)

Meanwhile, who would be up for a Paper Doll reading challenge to embrace books on organizing and productivity?

How To Make Your Reading Time More Productive With Book Summaries

My coverage of book summaries focused on non-fiction. Unless you’re in 11th grade English class (sorry, kids), you probably don’t want summaries of novels. However, you can get ice cream tastes of fiction, to see if you like an author’s style.

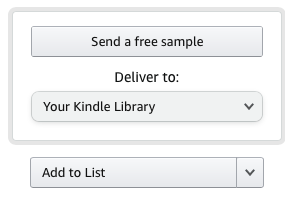

- Most people are familiar with Amazon’s “Look Inside” feature, which allows you to click a link above the book cover and read a handful of pages. But did you know that many Kindle books have “Send a free sample” link so you can preview chapters? Check in the browser version, not the app, below the “purchase with one click” section and above the “add to list” button.

- You can also get a free audio sample. Check for a link under the book cover.

- Literary Hub has daily offerings of novel excerpts. Click on the book cover you want to try, and the resulting page provides short author bio and a selection from the novel. Titles range from new releases, like Mrs. Murakami’s Garden, to reprints of classics, like Betty Smith’s Tomorrow Will Be Better. (Literary Hub also has short stories excerpted from short story collections.)

PAPERWORK DECLUTTERED

Organize for an Accident: Don’t Crash Your Car Insurance Paperwork

In April and May, due to much of the country quarantining and people driving far fewer miles, many insurance companies offered 15%-25% premium rebates to customers.

While rebates largely disappeared by June, that doesn’t mean you should be paying full price if you’re still staying close to home. For example, if your workplace has decided to go “permanently remote,” and you no longer have a commute, it’s worth contacting your insurance agent about potentially lowing your premiums now that you are regularly driving less each week. One option insurance companies are exploring is vehicle telematics, little “black boxes” that keep track of your speed, mileage, and precision at accelerating and decelerating, and report back to the insurance company. Safer drivers get better rates.

Similarly, if your college-age student is not currently on campus and is attending school remotely (from your home), that means your car is in the driveway most of the time, not states or time zones away. Review your situation with your agent for the greatest number of discounts.

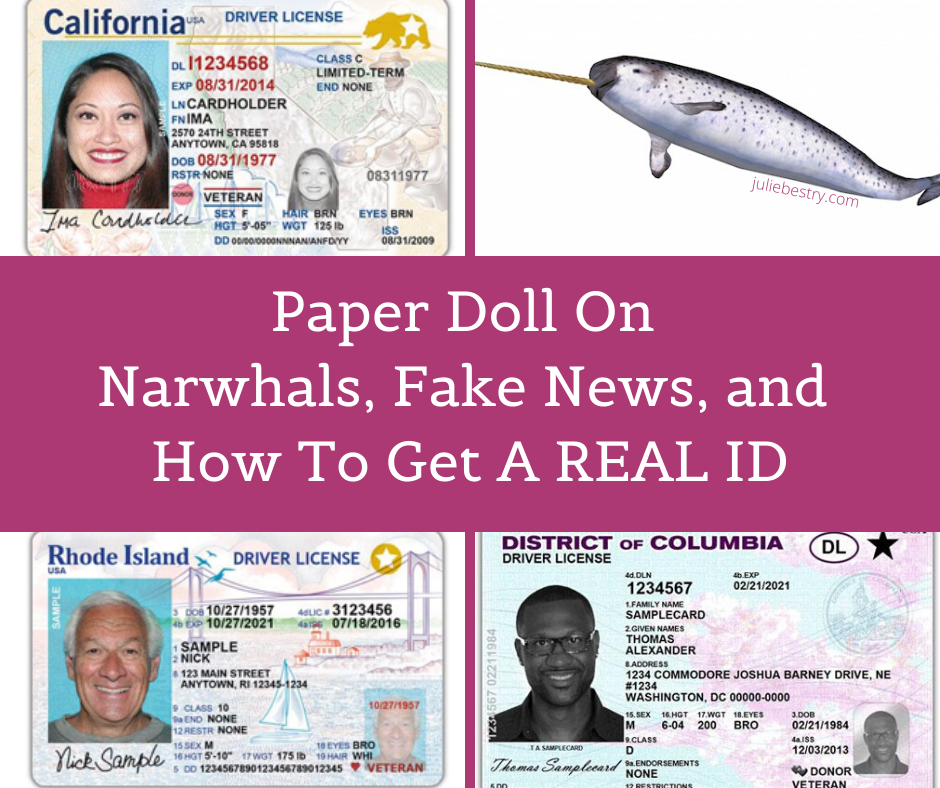

Paper Doll On Narwhals, Fake News, and How To Get A REAL ID

Everything in the post is still accurate except for the enforcement deadline. Due to COVID, the federal government delayed enforcing REAL ID by one year, to October 1, 2021. Remember, as of next October, if you don’t have Real ID-compliant identfication, you won’t be able to board a domestic flight or enter federal courthouses or restricted federal facilities, like military bases, nuclear power plants, or the White House.

Paper Doll Says The Tax Man Cometh: Organize Your Tax Forms

The forms are the same, but a few the rules have changed. Kiplinger’s Magazine covers a few dozen of the Tax Changes and Key Amounts for the 2020 Tax Year.

ORGANIZING ADVICE, PLAIN AND SIMPLE

The Truth About Celebrity Organizers, Magic Wands, and the Reality of Professional Organizing

As you head into 2021 armed with resolutions to get more organized, please review my counsel in this post. I stand by my word that there are no magic wands!

And in a future post, I’ll have more to say about advice from celebrity organizers with regard to organizing by color. Here’s a preview:

(Readers, if you like curry in your pumpkin pie, feel free to tell Jacki directly!)

Organize Away Frustration: Practice The Only Good Kind of “Intolerance”

This is the perfect week for you to take note of whatever frustrated you during the holiday season: a light system with too many broken bulbs, an artificial tree that has seen better days, a sense of obligation to send holiday cards to people who haven’t so much as liked one of your Facebook posts in a decade. Stop tolerating what doesn’t work for you, and if you don’t know the solution, seek help to find one.

Paper Doll Peeks Behind the Curtain with Superstar Coach, Author & Speaker Leslie Josel

Our talk about 1980s sweaters may have been dated, but discussion of student procrastination is not. This fall was the first semester that was 100% in COVID times; even stellar students struggled, and “taking an incomplete” has become a common refrain. If you have (or are) a student, Leslie’s How To Do It Now, Because It’s Not Going Away should be on your bookshelf.

Organizing in Retrospect: A Confessional Look Back at 2020

Writing this post, I realized I accomplished more than I realized. (Which would have been easy; when people asked what I’d been doing this year, I was often at a loss for words. “Missing my mom, my friends, and my travel plans, eating too much cheese, and craving Chinese food” seemed like an ineffective response.

This quiet lull before the new year is the perfect time to pull out your calendar and scan your To Do lists. Take notice of your achievements; in a year like this, it’s easy to forget small (and even not-so-small) victories. Ask your friends and loved ones to report back on the successes they recall from your year. Tally them up. Whether you use this in your next performance evaluation at work or just to buck up your self-esteem, remember that surviving this year intact is an accomplishment!

CLUTTER-FREE HOLIDAY GIFTS

In a Downton Abbey-themed post a few years ago, I told you about Give Back Box, a program whereby you could gather up the items your new holiday presents made redundant and easily ship them off to charity. This year, especially, when a touch-free donation option is especially useful, I encourage you to explore Give Back Box.

Clutter-Free Holiday Gifts for the Weird Year of 2020 (Part 1): New Twists on Old Favorites

For those of you looking for gifts of cooking classes, two highly praised options came in after deadline: King Arthur Baking‘s impressive calendar of interactive, online cooking and baking classes, and Milk Street‘s live-streamed and recorded, self-paced virtual classes. (If you give a cooking class gift to someone with whom you live, you get to eat the homework!)

Clutter-Free Holiday Gifts for the Weird Year of 2020 (Part 2): Giving Well, Giving Back

In addition to tangible gifts that give back to others, I wrote about charitable giving in your recipient’s name. Due to COVID, new tax laws let most taxpayers deduct cash donations of up to $300 made by December 31, 2020 when filing taxes in 2021 – even if you don’t itemize. (Note, this is a “per return” deduction, meaning married couples get the same $300 deduction as singletons. Consult your tax advisor.)

Clutter-Free Holiday Gifts for the Weird Year of 2020 (Part 3): Organizing Yourself & Others

Finally, I hope one of the gifts you give yourself is the time and opportunity to keep reading organizing and productivity advice here at Paper Doll.

Thank you, my dear readers, and have a happy, healthy 2021!

Follow Me