Paper Doll

Lost & Found: Recover Unclaimed Money, Property, and Savings Bonds

Treasure Chest by Immo Wegmann on Unsplash

Treasure Chest by Immo Wegmann on Unsplash

There are many reasons to keep your paperwork organized, but I think the most compelling one is that many VIPs (very important papers) are the equivalent of money.

Your Social Security card, for example, is key to proving who you are, and if someone gets his or her hands on your card (or even just the number) and a little bit of other information, you may suffer from years of financial strife due to identity theft.

A lost last will and testament means that a family could have to spend months or years lacking access to resources promised to them because of the difficulty of proving the deceased’s intentions for funds and possessions.

If you lose your birth certificate, you may not be able to replace other essential documents if they go missing or get destroyed in a fire or natural disaster.

Lose your passport without enough time before an international trip, and your vacation or work plans could be scuttled, leaving aside the potential for identity theft of a more-than-financial nature.

Paper Doll has covered a wide variety of topics over the years on accessing lost documents, creating essential ones you lack, and keeping them all safe so they are not lost in the future. These posts include:

Ask Paper Doll: Do I Really Need A Safe Deposit Box?

How to Replace and Organize 7 Essential Government Documents

The Professor and Mary Ann: 8 Other Essential Documents You Need To Create

Protect and Organize Your COVID Vaccination Card

A New VIP: A Form You Didn’t Know You Needed

Today, we’re going consider options for recovering lost property. Consider it a treasure hunt!

RECLAIM LOST “PROPERTY”

When I say “property,” what do you think of? Perhaps real estate?

Maybe that reality show Property Brothers with Canadian twins Drew and Jonathan Scott?

When you hear “lost property,” it’s possible you think of the boilerplate language on one of those claim tickets you get when you leave your coat at the fancy coat check room at a swanky venue.

So What Is Unclaimed Property?

The term unclaimed property is what you’ll hear most often when searching for lost money in various types of accounts. Unclaimed property usually refers to funds that a government (federal, state, or local) or business owes you because you’ve, quite literally, left it unclaimed.

It’s possible that you’re so organized with your paperwork that you feel affronted that I’ve implied you might have just haphazardly left money sitting around. But I’m not saying you’re absent-mindedly leaving piles of cash wrapped in newspapers like Uncle Billy in It’s a Wonderful Life. (By the way, that $8000 deposit that ended up in Mr. Potter’s hands would be work $121,762 in 2023! Maybe Uncle Billy should have tied the money to one of those strings around his fingers.)

Thomas Mitchell as Uncle Billy, searching the bank’s trash cans for the lost Savings & Loan deposit.

There are all sorts of reasons money may get separated from its rightful owner.

Perhaps you put a security deposit down on an apartment when you were in college, but after graduation you were heading across the country to start your first job. Your roommate returned the keys to the landlords, got the OK that you hadn’t left the place in a horrifying state, and similarly disappeared into the adult world, leaving no forwarding address for either of you.

In many cases, by law, your security deposit was placed in an account (perhaps interest-bearing, perhaps not) and should have been returned to you when your lease ended. If your landlords were playing by the rules, rather than deciding to take the money and run, they should have turned it over to the state.

Similarly, it’s common to have to pay a deposit when opening an account for certain utilities. While some utilities keep these deposits until you move and close your account, others have (little-advertised) rules stating you can request your deposit be returned after a set period of good payment history. Sometimes, however, if you don’t actually request your deposit back, it just sits there, eventually going unclaimed, and being sent to the state.

When I helped one of my clients, a gentleman in his 60s, search for unclaimed property in his name, we found a life insurance policy that his parents took out in his name when he was an infant. It had long since stopped increasing in value, so he claimed it and cashed out.

Or maybe your Great Uncle Horace left you oodles of money in his will, but his last valid address for you was three states and 22 years ago? (My condolences on Horace. We always heard good things about him.)

Unclaimed property can be in the form of cash, uncashed checks (including stock dividends), insurance policies, abandoned bank accounts, forgotten security deposits, or even tangible property in the case of safe deposit boxes.

Life gets busy. It’s OK. Don’t play the blame game. Instead, play finders keepers and locate your missing money!

Where Can You Find Your Unclaimed Funds?

Unfortunately, there’s no central repository for all unclaimed property. Instead, you can search in each applicable state’s unclaimed property office.

Start with Unclaimed.org, the website of the National Association of Unclaimed Property Administrators.

Once there, scroll down and select your state by clicking on the location on the map. If you are from a United States territory like Puerto Rico or the U.S. Virgin Islands, or from one of several Canadian provinces (Alberta, British Columbia, New Brunswick, or Quebec), click on the appropriate link below the map, or use the yellow “Select Your State or Province” button. This will take you to a specific unclaimed property office, like the Office of New York State Comptroller’s Search for Lost Money page or Tennessee’s unclaimed property search (with a snazzy alternative address of ClaimItTN.gov).

To begin your search at any of these state sites, provide whatever information you have available, but at least a first and last name (or, if you’re searching money owed to a company or non-profit, the entity’s legal name). Some state search sites will also ask for a city in order to narrow the parameters.

If you want to search for multiple states simultaneously (let’s say you have lived in many locations, or you’re searching for abandoned accounts for a relative who has passed away and are unsure where they might have had lived), visit MissingMoney.com.

MissingMoney.com allows you to just type a first and last name, and all possibilities for that name, across all state databases, will come up.

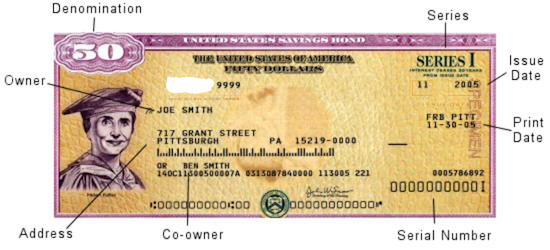

Whether you use a state search or a multi-state search, the resulting page should provide a series of options. If you find a listing for yourself (or a relative), you’ll likely see some combination of the following information:

- the name of the owner of the unclaimed property

- any co-owner’s name, if applicable

- the last known address of the owner (possibly including the street address, city, state, and/or zip code, though some states hide some of the information)

- the state in which the unclaimed property is held (if you’re doing a multi-state search)

- the amount or value of money being held (which may be listed as an exact dollar amount, a range (like $50-$100, or >$500), or “undisclosed); if the property is tangible rather than monetary, you may or may not get a clue to what it might be.

How Do You Claim Your Funds?

If you find a match for unclaimed property on your state’s page or through MissingMoney.com, you’ll need to file a claim to prove that you own the account or property. Similarly, if you are claiming it on behalf of a relative who cannot act on their own behalf or a person who has passed away, you must prove their connection to the property as well as show that you are the party authorized to file a claim.

Whatever search method you choose, as long as you go through a government web site, know that searching for the unclaimed property is free, as is filing your claim. (Please don’t get scammed by a site promising to funds that are due to you anyway. While some services are valid and may relieve you of labor searching for large 5- and 6-digit recoveries, I encourage you to exhaust all free options first.)

Each state or province will have its own rules regarding claim submission. While most prefer you to submit your claim online, some still let you submit by mail. Answer all of the questions to the best of your ability, and assuming you are able to substantiate that you have a right to the funds, the account will be processed in due time and sent to you.

For individuals, businesses, and non-profits, you will have to submit proof of identity, address, and ownership. For individuals, your identity can usually be proven by a scan/copy of your driver’s license, passport, or Social Security number; please be cautious about transmitting your Social Security number through the mail and be sure you are using secure web sites marked HTTPS.

Proof of ownership of property will vary. Options might include your Social Security number, employment pay stubs, W2s or 1099s, or utility bills.

If you’re making a claim on behalf of someone who is living, you will need to provide the appropriate documentation, which might included a copy of a child’s birth certificate or legal adoption order (if the money is due to someone under 18), proof of a claimant’s age, and a court document or other signed legal documents proving you have the authority to act on the actual owner’s behalf. These could include letters of guardianship or conservatorship, a trust agreement, or a Power of Attorney document.

If you are making a claim on behalf of someone who has passed away, you’ll have to submit a death certificate as well as a will or other court documents, like a Small Estate Affidavit and a Table of Heirs. (These are state-specific.)

What To Do Once You Get Your Now-Claimed Funds?

After you submit your claim, if you are able to sufficiently able to prove your right to the funds, you will eventually be sent a check. Verifying your identity and rights to the funds can take a while, though many states try to complete the processing within thirty days.

Once you receive your money, usually by check, deposit the funds as soon as possible. Do not run the risk of losing the check and starting the whole process over!

Depending on the source of the funds, you may have to pay state and/or federal tax on the claimed money.

For example, if this is a deposit returned to you, you would not owe tax on the amount of your deposit, but tax might be due on any interest the account earned. The same is true regarding funds from abandoned bank accounts; the principal would not be income, but interest would likely be taxable. Of course, if the money would initially have been taxable had you received it on time (such as with stock dividends), it will still be taxable, but as income in the tax year in which you are receiving it.

What About Unclaimed Money in Other Countries?

Are you a fancy-schmancy world traveler? Maybe someone in your family lived abroad?

Unfortunately, there’s no central repository for tracking money left behind in your Tunisian bank account or a security deposit your mom paid during her semester abroad in Paris. (You may find some solace in the links collected by the Global Payroll Management Institute.)

However, the US government’s Foreign Claims Settlement Commission does oversee unpaid foreign claims for covered losses. That’s government-speak for money you are owed for lost funds or real property in the following circumstances:

- a foreign government “nationalizes” your property (whether that’s the money in your account or the house you owned)

- damage to property you owned that was caused by military operations

- injury to civilian and military personnel

If any of these apply to you, review the Unpaid Foreign Claims page and fill out a certification form (linked on that page). There’s also a link for Standard Form 1055, if you’re filing on behalf of someone who has died.

LOST SAVINGS BONDS

Once upon a time, it was popular to give United States savings bonds as gifts when people got married, had babies, graduated from college, got confirmed or Bar or Bat Mitzvahed, or otherwise had a rite of passage.

In ye olden days, you’d go to your bank to buy a savings bond, and get a receipt for your purchase as well as a paper certificate to give to the recipient. With the old EE savings bonds, you could purchase a bond at half the face value, and then a few decades later, your investment would double to the face value. If you waited a little longer, the bond would keep earning interest, at least for a while. (If your bonds are more than 30 years old, they have likely stopped earning interest.)

Nowadays, savings bonds are registered electronically, which makes everything much easier. However, with the old bonds, without the certificates in hand, the process gets complicated.

The problem was that these called SAVINGS bonds — but people often treated them as if they were called “throwing-them-in-a-box-hidden-under-the-bed” bonds. That’s fine for a while, but once your bond stops earning interest, it would make sense to cash it in and find another wise investment option. That’s hard to do if you don’t have the bond.

What Should You Do If You Can’t Find Your Savings Bonds?

If you’re sure you have savings bonds, but can’t find your paperwork, you have a few alternatives:

- Check your safe deposit box or fireproof safe — Free, except for the value of your time.

- Search through those boxes of stuff your parents or guardians gave you when they retired to Boca or Shadytime Retirement Village. Again, free except for the value of your time.

- Ask your family members to check their safe deposit box(es) and/or fireproof safe(s) and send you (via secure shipping) your bond certificates — Depending on whether you live across the street or across the country from your loved ones, this will come at variable cost in terms of their time, delivery service fees, and you getting roped into providing IT support for your parents now that they’ve got you on the phone.

- Contact the Feds — If you can’t find your bonds, or know they were definitely lost, stolen, or damaged, this may be your only alternative.

If you’ve lost your original savings bond’s nifty tangible certificate, you have two options:

- replace your original bond with a digital* bond (held in your Treasury Direct account); or

- cash in your bond (possibly losing value if you decide to cash it in before it has reached maturity)

*Note: If your lost bond is a now-defunct HH bond, you can get a substitute paper bond. For EE or I-series, they must be digital

If you’re really lucky, even if you’ve lost the actual bond, someone in your family may have kept track of the serial number of the bond. If not, you’ll have to help the government perform a search. Go to the U.S. Treasury’s website at www.TreasuryDirect.com and fill out Form 1048 to locate savings bonds registered all the way back to 1935.

Random Treasury Trivia

EE savings bonds took the place of World War II-era E-series or “Liberty bonds,” which date back to WWI!

HH-series bonds, popular as gifts for GenXers and Millennials, only came in the paper format and existed from 1980 through 2004, and they stop earning interest in 2024. That’s next year. Yes, really. So it’s a good time to start looking for your HH bonds! I-series bonds were introduced in 1998.

Interested in buying bonds but not sure how they work? Treasury Direct has a whole page comparing EE and I-series bonds. Be sure to check out the rules and options for buying savings bonds.)

On Form 1048, you’ll be asked to provide as much information as possible, including the:

- Issue date (or a range of dates, if you are uncertain)

- Bond certificate serial numbers (if you have them)

- Inscription information on the bonds, including names, addresses as Social Security numbers.

- Whether the bonds were lost, stolen or destroyed. If the bonds were stolen and a police report was made, you will need to append that, as well. The government wants to know all the gory details, so if your Great-Aunt Gertrude started a food fight at Thanksgiving and your savings bonds were drowned in gravy, explain. Or, y’know, explain if your town had a flood. Whatever.

- If you are not the named party on the bond certificate, you will have to explain your right to access the bonds; for example, are you the parent or guardian of a minor, the conservator or legal representative of another adult, or the executor of the will of a now-deceased party? (Note: if the person named on the bond is deceased, you will also need to include a certified copy of the death certificate.)

- Then, you’ll have to state whether you want substitute (digitally-held) bonds or payment in return for cashing in your bond.

You will need the form to be certified by a Notary Public. Review Paper Doll’s Ultimate Guide to Getting a Document Notarized for your options.

Finally, mail the form to:

Treasury Retail Securities Services

P.O. Box 9150

Minneapolis, MN 55480-9150

What If You’re Not Even Sure If There Were Savings Bonds?

All of the above tells you what to do if you know you received the bonds, but they’ve since been lost, stolen, or destroyed (as in irretrievably folded, spindled, or mutilated…or drowned in gravy).

But maybe you’re not sure if your hazily-recalled bonds ever existed? Maybe you (or someone on your behalf) purchased bonds but they never arrived. Maybe you got hit on the head with a falling anvil and can’t remember if you ever had a bond, or maybe you think a deceased loved one owned savings bonds but you can’t find them?

If any of the above situations apply, visit the Department of the Treasury’s Treasury Hunt link. Enter your (or your loved one’s) Social Security number and state, and if there’s a match, the site will let you know what to do next to locate matured savings bonds, those that are uncashed but no longer earning interest.

This just scratches the surface of the unclaimed funds, property, and financial instruments that can be recovered with a little bit of effort. Invest a few moments to let your fingers do the walking and see if you can recover what’s been lost.

If you DO find money owed to you, please come back and share the story (but not confidential information) in the comments.

Paper Doll Helps You Find Your Ideal Analog Habit Tracker

![]()

If you cannot measure it, you cannot improve it.

~ Lord Kelvin (William Thomson, 1st Baron Kelvin)

If you cannot measure it, you cannot improve it. ~ Lord Kelvin (William Thomson, 1st Baron Kelvin) Share on XTHE BENEFITS OF HABIT TRACKING

Over the past two weeks, in Organize Your Annual Review and Mindset Blueprint for 2023 and Paper Doll’s 23 Ideas for a More Organized & Productive 2023, we touched on the importance of building good habits, either in and of themselves or to replace deleterious ones. We talked about the wisdom of James Clear, author of Atomic Habits: An Easy & Proven Way to Build Good Habits & Break Bad Ones.

Clear’s best-seller, which should be read in its entirety, talks about how successfully tiny habits (at the metaphorically microscopic, atomic, level) are based in four laws of habit creation:

- Make it obvious

- Make it attractive

- Make it easy

- Make it satisfying

In chapter 16 of the book, Clear references the essential nature of habit tracking, and ties habit tracking to the above four laws, but I’d like to speak directly to the last one. He states, “One of the most satisfying feelings is the feeling of making progress.” Well, duh!

And how can we verify our progress? Well, often, we can measure it by looking at the end result. If we’re trying to lose weight, we can measure our progress in having to tighten our belts or buy smaller clothes. If your kids are making progress toward doing better in school, improved grades will eventually make it obvious.

But it takes time to see that kind of progress, and if we’re going to keep motivated, to stick with our habits, we’re going to need to be satisfied daily. We need to see a sign of progress, no matter how minuscule, often. That’s where habit tracking comes in.

Habit tracking gives us an immediate sense of progress, even if the progress is only in our willingness to make an effort.

Persistence is the measurement of your belief in yourself. ~ Brian Tracy

Persistence is the measurement of your belief in yourself. ~ Brian Tracy Share on XTHE DRAWBACKS OF HABIT TRACKING

I should note that there are some inherent drawbacks to tracking our habits.

Our intention is to draw our attention to what we’re doing so that we can strengthen our resolve and recognize our struggles so that we may overcome them.

However, it’s easy to become so focused on our string of achievements that we become obsessed. When that happens, any time we do end the streak has the potential to demoralize us and weaken our resolve to get back on the horse.

If you tell yourself that you will run every day, but the weather is so stormy that “it’s not fit outside for man nor beast,” you may see your options as two-fold and rigid: risk life and limb and frostbite to hit your goal and mark that X or dot on your tracker, or leave it blank. That’s black and white thinking.

And if you leave it blank, you may feel like you’ve already lost. Somewhere, in the back of your head, despondency sets in, and failure to achieve your goal on one day can make you feel like a failure overeall, uninspired to get back to your habit the next day.

But this is an unnecessary dichotomy. Our habit goals are just that, goals. Doing something is always better than doing nothing.

If you can’t run three miles today, could you sprint up and down the stairs in your house, or work out along with a walking or dancing video?

If you miss your 10,000 steps and only manage 7500, could you do 500 extra steps for the next 5 days (or 250 for the next 10, or …)?

Maybe you promised yourself you’d practice the piano for 30 minutes a day, but your work and childcare schedule made that impossible; could you just play some scales to stay limber, or play one song to boost your spirits and remind yourself why this is a goal habit in the first place?

My colleague Karen Sprinkle created a wonderful 48-Week Achievement Guide, an e-book explaining how to use her patented chart for logging progress on goals. She recognized the inherent loss of momentum that comes from not getting to check off a day or week of a habit.

Thus, Karen’s chart creates space for four FREE weeks, weeks in which you have a “get out of jail free” card to not achieve your goals, while not exactly wrecking your streak, either.

Maria White interviewed Karen for episode #13 of her Enuff with the Stuff podcast, entitled Finally Accomplish Goals Using the 48-Week Achievement Guide. Take a listen.

DON’T BREAK THE CHAIN: THE BASIC CONCEPT

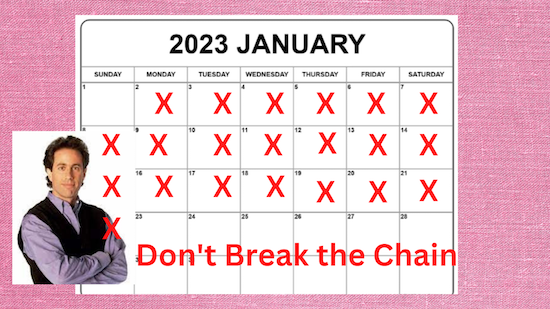

One of the best known tales of habit tracking comes from Jerry Seinfeld, master of his own (habit tracking) domain. Once asked how he wrote so many jokes, he explained that early in his career, he made a commitment to himself to write one joke a day.

Just one joke. But one joke every day.

He didn’t tell himself he had to have a Tonight Show monologue. He didn’t push himself to write a sitcom script. He just had to write one joke each day.

Seinfeld had a large wall calendar in his apartment, which showed all the dates in the year. Each time he wrote a joke, he marked the calendar with a red X, and as the story goes, he eventually had a long chain of red X’s to create a visual cue to show how he’d been consistently putting in the effort.

Did he need talent? Of course. Comedic timing? Without question. But Seinfeld’s advice to young comedians was simple: Don’t break the chain!

The chain of red X’s on the calendar is just the simplest form of habit tracking.

AUTOMATED HABIT TRACKERS

The easiest (though not necessarily the best) kind of habit tracker is one that is automatic, or done for you by something or someone else.

I recently bought a new scale, and realized that it had a Bluetooth function. I didn’t really need a scale with Bluetooth, but I was intrigued to find that once I connected it to the iPhone app (which itself connects to the Fitbit app), my scale tells the app not only my weight, but also my BMI, metabolic age, the percentage of my body made up by water and of skeletal muscles, my bone mass and muscle mass, and all the percentages of my fat that is body fat, subcutaneous fat, and visceral fat. And I hope that’s the last time I ever use the word “fat” in this blog!

My point is that all I have to do is to step on the scale (which I do only once per week so as not to obsess) and the app and the magic of Bluetooth does all the rest.

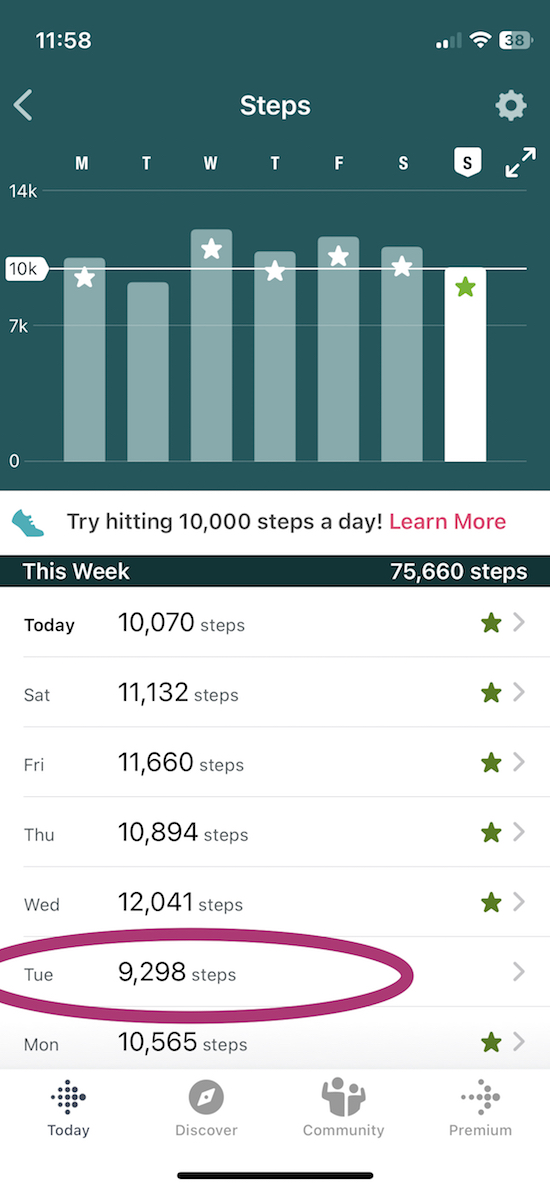

Similarly, while I can (and admittedly do) look at my Fitbit tracker on my wrist, the app takes care of tracking my efforts. Here’s how I did this past week.

Note: while I didn’t make my 10K goal steps on Tuesday last week, I made up for it the next day. I didn’t get down on myself for it, because I knew that progress, not perfection, is key to building habits.

There are even “smart” water bottles that measure and communicate (again, by Bluetooth) with an app to track how much you’ve hydrated!

There are a few main benefits of an automated habit tracker:

- You don’t have to do any math. (Yes, I can add daily numbers to get weekly ones, but why should I have to?)

- Automated trackers require little effort, so you can concentrate on your behaviors without focusing on the mechanism for measuring them.

- You don’t have to worry that you will forget to consistently measure and track your habits.

Parents and teachers commonly track and report the success of children at achieving habits, from potty training to turning in homework to practicing vocabulary words. If you work in a call center, there’s software to measure your metrics: how many calls you took, how many ended in resolved problems, etc.

The key problem with automated habit tracking is that by completely off-loading the labor of tracking, there can be a disconnect between effort and how much you pay attention to your habits. This is why, although there are many excellent habit tracking apps, I recommend that clients start their habit tracking journey with proactive analog methods.

CONCEPTS TO CONSIDER WHEN SELECTING A HABIT TRACKING METHOD

As you’ve heard me say before, with regard to calendaring and note-taking, the determination of whether you should go analog or digital, or which method within either category you choose, depends more on your self-knowledge than what’s popular.

If you love apps and prefer to gamify your habits, a habit tracking app may be your best bet, even if I would personally argue against it. If you have an artistic bent and find color motivating, selecting an analog habit tracker that lets you use colorful markers or crayons to track your progress might be the key to your inspiration.

Consider the following:

- Delight — How much do you enjoy a particular method of tracking your habits? Do you get joy or a sense of calm when you stop to log or mark your progress because the colors please you or the app makes a delightful sound?

- Convenience — How easily accessible is your method of tracking your habit? Does your tracking method need to be portable? If it’s just a card in your wallet or an app on your phone, it may not make a difference, but if you want to have a beautiful tracker, you’ll need to have drawing implements with you or wait until you’re wherever they are. Will that delay impact the likelihood that you’ll track what you do? Will you be less likely to perform the habit if your tracking method isn’t always visible?

- Flexibility — Do you want to customize your tracker or just follow whatever already exists? For the same reasons that I find bullet journals stressful (too many options, too many reminders that I’m not artistic), I’d prefer an analog system that has practically no customization, but wouldn’t mind getting to plunk around with digital settings to change colors and graphs or charts in an app.

- Measurement style — Do raw numbers have meaning to you, or do you need to see a bar chart? (And do you care whether your charts are vertical or horizontal?) Does a particular measurement style affect how much attention you’ll pay to your tracking? The attention you pay will surely have an impact on how much you improve.

- Commitment and accountability — The nature of the habit tracking method you choose can increase (or decrease) how committed you are to tracking, and thus to the habit you are building. Does this method make you feel more committed? Does it make you feel accountable to it?

We manage what we monitor. ~ Gretchen Rubin

The more you embrace your habit tracking method, the more closely (in a healthy way) you will monitor it. And we are more likely to tweak and improve and, in the words of Gretchen Rubin, manage what we monitor.

We manage what we monitor. ~ Gretchen Rubin Share on XANALOG HABIT TRACKERS

There are a variety of analog habit tracking methods, from — yes, as Seinfeld did — making X’s on a blank calendar to buying or making your own cute trackers. The following are just a few suggestions so you can consider what you might like to try.

Adhesive Habit Trackers

Tiny adhesive habit tracker sticky notes have the advantage of fitting anywhere. If you use a paper planner (and if you need ideas about that, see Paper Doll’s Guide to Picking the Right Paper Planner), sticking your tracker on your current weekly page or even on the front of your planner will keep it — and your goals — front and center.

I’m a huge fan of almost anything in the 3M Noted by Post-it® line. I found the following in my local Target last year; the periwinkle shade drew me to it.

![]()

I haven’t been able to find this 2.9″ x 4″ Noted by Post-it® Habit Tracker at Amazon, but they are available at Target online and in stores. Online, 3M only mentions the pink version, for which they only have this tiny photo; the difference seems to be the “Make it a habit” label instead of the “Take (self) care” title.

![]()

The very-cool mäkēslife goal-setting/stationery store has a minimalist, $5 habit tracker sticky notepad. Because it only indicates the days of the week and has six lines for habits on each note, you can either track multiple habits each week, or one habit for six weeks (or two habits for three… you get the idea). The 60-sheet pad measures 3.25″ x 2.125″.

![]()

Adhesive habit trackers are quick and easy to grab, so they’re low-effort. Setting one up takes seconds, and checking a box or circle is no more effort than an X on the calendar. But only you know whether effort on the low end of the continuum will keep you motivated. Do you need more involvement to embrace the habit of tracking a habit?

Habit Tracker Printables

On various sites, you’ll find both free and for-purchase habit trackers. On Etsy, for example, a search of “Habit Tracker Printable” yields hundreds of choices, from the simple to complex.

This streamlined, downloadable Monthly Habit Tracker from MyLifePlans on Etsy comes in two styles, one with boxes and one with circles, and is just $1.74:

![]()

My colleague Katherine Macy of Organized to Excel references her own (free) downloadable, printable habit tracker in the post Practical Tips for Living Your Best Life: The Smallest Achievable Step.

![]()

©2022 Organized to Excel

Another fun option is from Cristina at Saturday Gift. Cristina has created free downloadable, printable spiral habit trackers in 28-, 30- and 31-day styles, as well as a variety of mini-trackers, trackers designed to be used in bullet journals, and more.

![]()

Printables are ideal for someone who prefers something that takes up a little more real estate and is less likely to get lost. You’re limited by the designer’s creation, though, so if you’re the type of person who needs a lot of customization, printables don’t offer much wiggle room for your muse.

Printables can also seem like homework. For an Obliger or Upholder (in Gretchen Rubin’s Four Tendencies parlance), this is a plus. If you’re a Rebel or Questioner, however, printables may work less for accountability and feel more like an (unwanted) obligation. Know thyself!

Habit Tracker Cards

Not everyone wants a sticky note or a full-size printable. Some people just want a tiny note they can tuck in their wallet or use as a bookmark, but keep handy.

Baron Fig has a series of 3″ x 5″ Strategist Index Cards in three styles: Dot Grid and To-Do, each $10/pack of 100 and Habit Tracker cards for $15/pack of 20. All have rounded corners. (The Dot Grid and To-Do cards are blank on the back; the Habit Tracker cards have motivating quotes on the reverse.)

![]()

Fancy Plans takes the popular spiral style of habit tracking to the card form in their 3″ x 3″ Linen Textured Habit Tracker Journal Cards. ($7.99 for a six-card set.)

![]()

These square, spiral habit trackers are tiny and designed to be clipped into your journal/planner pages. Each tracks up to eight habits for an entire month.

Unlike more traditional index-style cards, these are smaller, and if you weren’t great at coloring inside the lines in kindergarten, the teeny-tiny boxes might outweigh the visually appealing nature of the spiral. Fear not; we’ll be looking at a similar but more expansive option a few sections down.

At Home With Quita’s YouTube channel has a great video on how to use these. Scroll to about nine minutes in when the coloring begins.

Of course, you could make your own DIY habit tracker card if you had the patience (and a straight edge, pencil, and stack of dollar-store index cards).

I liked the minimalist combination of “Don’t Break the Chain,” DIY, and cards (if not actual card stock) illustrated in this video from the Robert’s Theory YouTube channel. I also thought the white/silver ink on the black background had a nifty visual appeal.

Habit Tracker Journals

As with printables, you will have an embarrassment of riches from which to choose when you search for habit trackers journals.

Baron Fig has created a Clear Habit Journal in collaboration with James Clear. The clothbound, hardcover, rounded-cornered, open-flat notebook features habit trackers, one-line-per-day journaling space, and lots of Clear-specific content. It comes in two sizes: Flagship (medium size at 5.4″ X 7.7″ and 224 pages) or Plus (large size, 7″ X 10″ and 208 pages). It’s $26.

![]() However, if you want a journal that you could place on display to clock your habit tracking as the day goes by, there are a variety of styles, from gridded notebooks to artistic visions.

However, if you want a journal that you could place on display to clock your habit tracking as the day goes by, there are a variety of styles, from gridded notebooks to artistic visions.

This Lamar Habit Tracker Calendar in the spiral style is undated, spiral-bound, and stands-up on its own, or you can hang it or lay it flat. It’s $16.95. You can track weekly and monthly habits.

![]()

If you’d like something a little more subdued, Weanos has a Habit Tracker Journal in a similar format, but with Kraft coloring, for $14.99.

![]()

And you can explore the internet (or even just Amazon) for a wide variety of other habit tracker journals.

DIY Your Bullet Journals for Habit Tracking

All of the prior options give you pre-ordained structure for tracking your habits. Personally, I don’t want to fiddle with lots of customization; it takes away from the time I would prefer to spend on my habits rather than on creating a system for tracking my habits. I’m willing to trade the beautiful and creative (admittedly, because my artistic leanings are neither beautiful nor creative) for having all the boxes be the same size and not having to worry about my chicken-scratch handwriting.

However, if you like the idea of having a notebook with you in which to track your habits, and if you want to embrace customization in terms of style and color, a bullet journal or other blank journal might be ideal for you.

The internet is full of options for formatting. You may want to start with this short list, all with mind-blowing graphics for tracking your habits:

50 Habit Tracker Ideas for Bullet Journals (Bullet Journal Addict)

25 Bullet Journal Habit Tracker Layout Ideas to Help You Build Better Habits (Habits Buzz)

121 Habit Tracker Ideas for Your Bullet Journal (Planning Mindfully)

45+ Bullet Journal Habit Tracker Ideas & Examples for 2023 (Develop Good Habits)

10 Habit Tracker Spreads (Bullet Journal Habit video)

Intentional Habit Tracking (Bullet Journal)

In addition to design ideas, and especially helpful for those of us who aren’t so artistic but might like to explore habit tracking with a bullet journal, there are two tools that I find delightful.

Stickers

Sometimes, flashing back to third grade is just what you need to get a boost of motivation. (Though sadly, I suspect it’ll be hard to find any scratch & sniff habit tracking stickers.)

Stickers are fun, colorful, and add pep to paper. When I visited Italy and the UK, I bought a variety of stickers for use in my paper planners. Stickers for tracking habits would be equally motivating.

Just Google “habit tracker stickers” and you’ll find a nifty bounty of colorful options.

The Grey Palette‘s Habit Tracker sticker sheets in cool or warm hues offer up 4.5″ x 6.5″ stickers (32/pack for $5.25) for tracking Sunday to Saturday habits and habit-specific stickers.

![]()

Mochi Things has a huge variety of color-dot stickers, calendar stickers, and grownup activity stickers made from PVC material and generally priced under $5 for a set. If you’d rather use dots than markers, the Circle Pigment See-Through Stickers might fit the bill (and prevent marker bleed-through in journals).

Rubber Stamp Blocks

If your fear of creating wiggly lines and lopsided grids in a bullet journal or DIY habit tracker is keeping you from embracing the format, rubber stamp blocks may be the secret shortcut.

I found a large number of calendar/planner/habit tracker rubber stamp blocks on Amazon, Etsy, and around the internet, but they all seem to follow the same patterns, so I encourage you to find a price and style that appeals to your aesthetic.

This Tosnail 18-Piece Bullet Journal Stamp Kit creates all the stencil/formats you need for bullet journaling, including dated and undated tracking grids, as well as formats for just listing the days of the week, as well as stamps for calendaring, list-making, meal-planning, and more.

Although I’m a Paper Doll, I know there are a variety of digital habit tracking solutions, from simple spreadsheet-based grids to cool Evernote habit tracker templates to apps galore. We’ll explore digital habit tracking in the near future.

Until then, how do you track your habits? Please share in the comments.

Paper Doll’s 23 Ideas for a More Organized & Productive 2023

Happy New Year! And welcome to GO (Get Organized) Month 2023, where we celebrate efforts to make our spaces more organized and make ourselves more productive.

We in the National Association of Productivity and Organizing Professionals (NAPO) love this opportunity to help you make this year your best. To that end, today’s post offers up 23 ideas for achieving what you want this year in your space, schedule, and life.

CREATE A FRESH MINDSET

1) Learn last year’s lessons to build next year’s success.

You were probably super-busy last week, but I encourage you to read the final Paper Doll post of 2022. (Trust me, it was a good one!)

Organize Your Annual Review & Mindset Blueprint for 2023 is full of questions and resources for figuring yourself (and your last year) out.

I often joke to clients that while I’m not a mental health professional, I am like a marriage counselor between you and your stuff. Well, last week’s post is like a cross between a therapy session and a deep dive with your BFF. It rejects the demoralizing proposition of resolutions in favor of creating a fresh, motivating mindset for the coming year, whether with a word, quote, or motto of the year, and uses signage, a vision board, or a music playlist to keep your eyes on the prize that is your new and improved life.

2) Don’t take my word for it. Listen to James Clear.

If you’ve been paying attention to the news in the “habit” realm at all in the last few years, you know that James Clear wrote Atomic Habits: An Easy & Proven Way to Build Good Habits & Break Bad Ones, a book that takes the research of habit researchers (like Charles Duhigg in his The Power of Habit) and makes it all actionable.

Theory is good, but what most of us want is someone to tell us how to do it, and preferably in a way that doesn’t make us hungry, cranky, poor, or frustrated. Clear delivers.

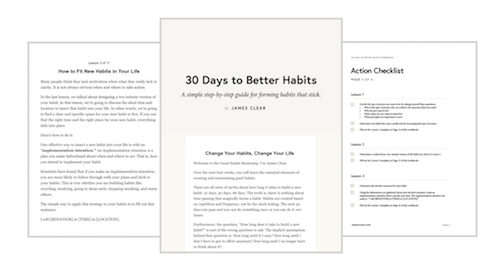

But this year, he’s doing something special. Clear is offering a free email course called 30 Days to Better Habits: A simple step-by-step guide for forming habits that stick.

It’s not a bootcamp. Rather, as Clear explains, “Habits are not a finish line to be crossed, they’re a lifestyle to be lived.” Over eleven emails (after an introduction), one sent every three days, he’s going to gently teach principles to help cultivate a new lifestyle (and not merely a set of “tasks you can sprint through during a 30-day challenge.”)

There’s also an 18-page PDF workbook and a Google spreadsheet with more than 140 examples (!) of how to implement the strategies in the course and apply them to different habits.

The course is based on Atomic Habits, but he notes that you don’t need the book to successfully complete the course. However, because I originally read a library copy, I decided to buy my own, because he’s also got a nifty set of bonus packages for those who do buy the book. Basically, you email a copy of your receipt or other proof of purchase, and you get:

- Bonus Guide: How to Apply Atomic Habits to Business

- Bonus Guide: How to Apply Atomic Habits to Parenting

- The Habits Cheat Sheet

- Companion Reading Guide email series

- Habit Tracker

For what it’s worth, I bought my copy New Year’s morning, and had received the bonuses by the time I had lunch!

3) Make strides towards delight, too!

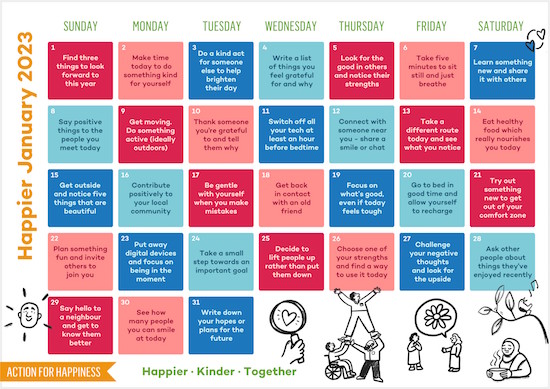

One of my favorite sites is the UK-based Action for Happiness. Each month, they put out a stellar calendar of tiny (Clear might even call them atomic) actions you can take toward a better life. Each month is themed, and you can find daily reminders on their Instagram, Twitter, and Facebook accounts.

January 2023’s theme is Happiness, and on New Year’s Day, the assignment was to “Find three things to look forward to this year.”

If you’re wondering what happiness has to do with organizing and productivity — hi, you must be new here!

But seriously. Clutter — all the excess stuff in our spaces, in our schedules, and in our brains — wears us down. It’s not at all uncommon for clients to be dealing with clinical depression or anxiety disorders, and disorganization and lack of productivity (and the stress of toxic productivity), only contribute to greater unhappiness. Think of these daily themes less as homework (“I have to”) and more as opportunities (“I get to”) on the path to organizing your mental health.

4) Collect good days — literally!

Each day, make a habit of writing down something great that happened. You can consider this part of (or instead of) a gratitude practice.

Our lives fill up with what we give our attention, so let’s pay attention to the good stuff. Next year, when you’re doing your annual review, you’ll have a tangible resource for looking back on the year and see the highlights, what you considered valuable at the time, and what might have been forgotten had you not made a notation.

Our lives fill up with what we give our attention, so let's pay attention to the good stuff. Share on XCreate a spreadsheet, an Evernote note, a pretty notebook, or — and this is my favorite idea — a Jar of Joy! (Someone else came up with the concept, but I came up with the name. Write a few words or a sentence about whatever great thing happened on a slip of paper. Fold or roll it up, and toss it in a jar or glass canister. Consider using colored slips of paper to make the contents look prettier, and keep your Jar of Joy visible, so you can be reminded each day that good things are happening!

5) Remember that tiny tasks count toward a more productive life.

There’s a reason why James Clear (and, ahem, Paper Doll) believes that those teeny, tiny steps lead to success. Whatever you want to achieve, whatever goals you have, I’d like to encourage you to figure out the teeniest, tiniest, itsy-bitsyist thing you can do to get yourself microscopically closer to the finish line…heck, to the starting line.

Adam Bulger at Fatherly.com came up with 27 Life-Changing Micro Habits That Require Only A Few Minutes. Many of the habits on this list take less than a full minute to accomplish. I liked item #23 on his list:

Always put one thing away before you leave whatever room you’re in. If you’re overwhelmed by clutter, you feel like you don’t have time to clean but habitually chipping away at the mess, one piece at a time, can make it more manageable.

— Liz Fosslien (@fosslien) June 28, 2022

START PLANNING YOUR YEAR

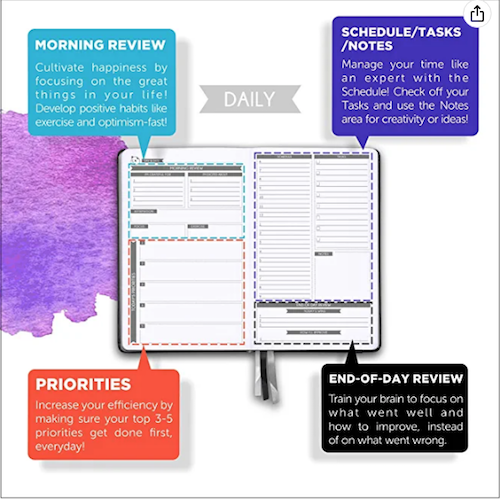

6) Select your planning system.

If you’re a digital person, your calendar is a continuous scroll of everything you’ve got planned. But if you’re a paper planner person (try saying THAT three times quickly!), you may have delayed getting a planner out of fear of buying the wrong one, or perhaps you’ve just not written in what you did buy, because you “don’t want to mess it up.”

It’s your planner. You can fill it in with crayons and use scratch-&-sniff stickers, and it’ll be OK. Whatever inspires you to log your meetings and appointments, block your time, and work toward your deadlines is fine with me. (And if anyone gives you guff, send them to Paper Doll. I’ll set them straight!)

If you’re still struggling with how you’ll plan your 2023, go visit Paper Doll’s Guide to Picking the Right Paper Planner. It covers the features you need to consider in a planner (including whether you’re better off with digital or paper), as well as pointing out some of the best options.

The key to organizing your life is being able to visualize your time. So get everything out of your head and in front of your beautiful eyeballs.

7) Move into your new planner now.

Make a cup of cocoa, grab last year’s planner or pull up your digital calendar (using two screens, like your computer and your phone simultaneously) — compare apples-to-apples.

Go page-by-page through last year’s schedule and copy over everything that recurs on the same dates, like birthdays and anniversaries. Digital users can skip this step.

Next, add events that happened last year and are already scheduled to happen again, but not on the same dates (like conferences, work retreats, mammograms, dental appointments, etc.).

Use last year’s calendar to help prompt you to make a list of everything you need to schedule or add to your long-range tasks, like setting an appointment with your CPA to discuss tax issues.

8) Don’t forget to plan time for your activities.

Appointments aren’t everything. Make time in your schedule for thinking, doing your creative work, attending to self-care, and so much more. Whenever clients complain to me that they don’t have time to accomplish something that they swear is important to them, I ask them to show me where they’ve put it on their schedules. [Insert cricket noises here.]

The truth is that if you don’t prioritize something by making time for it, it’s not really a priority to you. Treat yourself with the same respect you’d treat your boss or your best client or your Grandma, and make time for what matters:

Struggling To Get Things Done? Paper Doll’s Advice & The Task Management & Time Blocking Virtual Summit 2022 (I’ll have news about the 2023 summit coming soon!)

Playing With Blocks: Success Strategies for Time Blocking Productivity

Organize Your Writing Time for NaNoWriMo 2022 (Even though the post is ostensibly about making time to write, it’s applicable to make time for anything you value.)

9) Nurture your commitment to your planning system…every day.

If there’s so much going on in your life that you forget to check your planner or digital calendar and task system until it’s too late, upgrade your accountability support:

- Set an alarm on your phone to ring at around 5 p.m. daily to remind you to check your calendar and tickler file for the next day and the coming week.

![]()

- If you have an assistant (especially if you both work remotely) schedule time each day to review newly-added appointments and obligations.

- Have a family meeting on the weekend to make sure every appointment and school pick-up is covered.

- Schedule your next appointments before leaving anyplace you visit intermittently (doctor, dentist, massage therapist, hair or nail salon, etc.) — but only if you have your calendar with you. Otherwise, ask them to call you. Never agree to any date without your planner nearby. In fact, if you tend to agree to too much, say that your professional organizer told you that you’ll have to wait to check your schedule before taking on any new obligations. (Blame me; I won’t tattle.)

10) Know where your time is going — before it gets away from you!

It really doesn’t help you schedule all of the things you’re supposed to be doing if you don’t have a handle on what you’re actually doing. To that end, Laura Vanderkam is doing something nifty.

You may know Laura from her podcasts, her blog, or her several books, including 168 Hours: You Have More Time Than You Think, Off the Clock: Feel Less Busy While Getting More Done, and the recently published Tranquility By Tuesday: 9 Ways to Calm the Chaos and Make Time for What Matters.

Laura is running the 168 Hours Time Tracking Challenge — and yes, I signed up for this one, too. I’ve always enjoyed Laura’s writing, but when we both participated in the 2022 Task Management and Time Blocking Summit, I really got to peek behind the curtain to see how she thinks about time and our use of it. She’s talking about time concepts and strategies that are too rarely discussed.

The 168 Hours Time Tracking Challenges doesn’t start until the middle of next week, January 9, 2023, so there’s still time to sign up. After signing up, you’ll get links to resources and suggestions for tracking your time on paper (via Laura’s time sheets) or digitally, as well as links to her other writings on the subject.

Like tracking what you eat (which can be emotionally distressing), tracking what you do with your time can be uncomfortable. When you realize you’re spending 3 hours a day on social media — and your job is not as a social media influencer — you may be upset. But if you recognize that you’re spending 90 minutes (or more) of every day “making do” with software that keeps freezing or helping a co-worker who takes advantage of your kindness, you’ll become more aware of challenges you can then overcome!

BECOME YOUR OWN MONEY HONEY

11) Make a TAX PREP folder. Actually, make two.

Tax season has started. Within a matter of weeks, your mailbox will start filling up with W-2s and 1099s, and you’ll need to keep them safe. At the very least (if you haven’t done it already), create a folder with a simple name like 2022 Tax Prep.

Look around for all of your tax-deductible receipts and charitable donation paperwork, and pop those in; when forms start arriving in the mail, put those in, too. Some of your important tax forms may come by mail; others, like your investment accounts or health insurance annual summary, might live in your online accounts, requiring you to log in.

This one two-minute task will save you so much time down the road. And time is money, so whether you do your own taxes or hand things off to a CPA, you’ll be saving the Benjamins as well as the clock-hours.

You don’t have to get fancy. A manila folder set in the front of your financial files is fine; or get a dedicated accordion folder like the Smead All-in-One Income Tax Organizer.

12) Stop hiding from your financial truths.

You have to answer mail call! Not looking at your bills when they come in the mail (or email) is like ignoring a pain that gets worse and refusing to go to the doctor because you’re afraid of bad news. Financial ills don’t go away on their own.

Not looking at your bills when they come in the mail (or email) is like ignoring a pain that gets worse and refusing to go to the doctor because you're afraid of bad news. Financial ills don't go away on their own. Share on XWhy not start bossing your money around instead of letting it bully you?

Over the course of the next few weeks, get in the habit of putting your bills and statements all in one place, like a folder next to your computer. If you normally just get a reminder to log in and pay a bill, make a point of downloading and/or printing out your monthly statement.

Make a list of all of your credit cards, loans, and other debts, as well as their balances and interest rates. Seeing it in black and white is the first step toward taking control of your financial future.

13) Get a financial accountability partner!

Last year, I said, “If you don’t know the difference between an NFT and BBQ…” It turns out a lot of people were investing in NFTs and cryptocurrency when they would have been better off having a backyard barbecue and inviting their friendly neighborhood fee-only Certified Financial Planner.

I’m no expert in cryto-currency. (And your brother-in-law’s cousin almost assuredly isn’t!) But whether you want to know whether you invest more in your 401K or your IRA, a fee-only CFP can help you out when your eyes start to glaze over. You pay for their expertise, and they give you unbiased advice because fee-only CFPs don’t get any commissions on investments you make.

Does thinking about investment vehicles feel like choosing between between becoming a rock star or an NBA star (because of their equal improbabilities)? If you need support and strategies for getting your bills paid on time, every time, there are NAPO members who are financial organizers; you can also find a Daily Money Manager through the American Association of Daily Money Managers (AADMM).

BECOME A VIP WITH YOUR VIPs

14) Get your vital documents in order.

It’s a sad fact of life that people get sick or incapacitated, and sometimes shuffle off this mortal coil far too soon. Whether it’s illness or natural disasters or some other kind of calamity we don’t want to think about, we need to get our affairs in order. And that means getting paperwork straight.

Check in with these posts for step-by-step guidance to making sure you’re covered with up-to-date vital documents and a way to keep them organized.

- A New VIP: A Form You Didn’t Know You Needed — If you or anyone in your life is in Medicare, please make sure you read and act on this post! This is not one that you should put off.

- Ask Paper Doll: Do I Really Need A Safe Deposit Box?

- How to Replace and Organize 7 Essential Government Documents

- How to Create, Organize, and Safeguard 5 Essential Legal and Estate Documents

- The Professor and Mary Ann: 8 Other Essential Documents You Need To Create

- Protect and Organize Your COVID Vaccination Card

15) Put your foot on the brake before automatically renewing your car insurance.

If you haven’t shopped insurance to compare prices and coverage in recent years — or ever — this is really the time to do it.

This year, I updated an older post that explained all of the elements of auto insurance, as well as how and where to organize your paperwork.

Organize for an Accident: Don’t Crash Your Car Insurance Paperwork [UPDATED]

But the post also talks about the wisdom of comparison shopping. While you’re at it, shop around for homeowners’ or renters’ insurance, as well. Why not organize some discounts while you’re organizing your paperwork?

16) Clean out your wallet and make an inventory.

You’ve probably got too much in your wallet. If you keep it in your purse, it’s giving you shoulder pains; if it’s in your back pocket, you’re likely misaligning your spine. Why not take a lunch hour and declutter your wallet, and then put it all back so it makes sense to you?

While you’re at it, this is the perfect time to take an inventory of the licenses, insurance cards, and debit/credit cards you have in there and all the information contained on them.

Pull everything out of your wallet, make two columns of cards on the table, and take a photo with your smartphone. Then flip each card over in the same position, and photograph the back. Easy-peasy. (If you’ve got a home scanner/copier, it’s fine to use that, but I’ll discourage you from using a public copier; it’s too easy for someone to surreptitiously snap photos of your information over your shoulder.)

Remember to password-protect the document on your phone or in your cloud back-up.

EMBRACE PAPER DOLL‘S CLASSIC PRINCIPLES ABOUT ORGANIZING

17) Follow the Ice Cream Rule.

I tell my clients, “Don’t put things down, put them away.” The word “away” assumes you’ve already got a location in mind. But good organizing systems have two parts: the where & the how.

When you bring groceries home, you put the ice cream away in the freezer immediately to keep from having a melted, sticky mess. It’s pretty rare for someone to put away the toilet paper or breakfast cereal before the frozen foods. The freezer is the “where” but putting the ice cream away first is the “how.” It’s so innate, you don’t even think about. But for most of your stuff, including papers, you do have to think about it.

Whatever comes into your space, when you go shopping, or even when things are free, decide on a home before you bring it in.

Once it’s in your space, build fixed time into your schedule for how/when you’ll deal with maintaining it or getting it back to where it lives. When will you do laundry? When will you file financial papers? What will be your trigger — when the laundry basket or in-box is full, or will you put it on your calendar?

Remember: “Someday” is not a day on the calendar.

18) Everything should have a home, but not everything has to live with you.

Clients are often so focused on organizing what they already have that they ignore a key truth: not everything you own needs to stay with you forever.

If it’s broken and you’re not willing to spend the time or money to repair it, let it go. If you’re sentimentally attached to something that’s outdated or takes too much space or effort to keep, take a photo of you holding it or wearing it. Then set it free!

If you have piles and files full of clippings and articles you haven’t looked at in years, you’re not alone. 80% of what gets filed is never accessed again. Trust that the internet is a vast storehouse of everything you’d want to look up, and if the paper you’re holding has nothing to do with you, personally, or reflects information you’ve long since learned by heart, recycle it and give yourself space.

19) Don’t fight clutter with more clutter.

I love The Container Store and all the office supply stores as much as every other professional organizer. (Really!)

But buying oodles of storage containers — bins, boxes, tubs, and shelves — can only help you organize if you pare down to what you need and want.

Photo by Lia Trevarthen on Unsplash

When you see a great outfit at the store but it’s not in your size, you shouldn’t say, “Hey, I’ll buy this now and then lose (or gain) 30 pounds to fit into it.” Even if you do declutter the personal poundage, you never know from where, exactly, that weight will disappear. It almost certainly won’t be a perfect fit.

I’m not saying never to acquire storage containers (adorable or otherwise), but do it last. Once you pare down, pick colorful, fun containers that suit your needs, space, and tastes.

20) Take baby steps. Declare small victories. Don’t feel like you have to do it all.

When it comes to clutter, it’s not the space it takes up in your house, it’s the dent it puts in your life! If you’re late every day because you can’t find your keys and your kids can’t find their homework, it’s a much bigger deal than a cluttered guest room closet or drawers of old birthday party pictures that haven’t been scrapbooked.

Focus on your biggest daily stressors, break them down into small, actionable steps, and solve those first. You don’t need to do it all at once, but if you develop a habit of doing a little bit at a time, once your space is straightened up, maintenance will feel natural.

What you don’t do is just as important as what you do. pic.twitter.com/sE6BrMyUAm

— Sarah Arnold-Hall (@saraharnoldhall) November 6, 2022

21) Declare bankruptcy on clutter debt.

Give yourself permission to declare bankruptcy on the “debt” of unread magazines, charitable contribution requests that aren’t really your cause, unworn clothes three sizes too small, or email from last July. In the words of Elsa, LET IT GO!

Keeping something just because you spent money on it or because it was a gift doesn’t make it any more valuable or useful; it just ends of costing you time (dusting or caring for it), space (that you could use for more important things), or money (spent on dry-cleaning or storage rental).

Keeping something just because you spent money on it or because it was a gift doesn't make it any more valuable or useful; it just ends of costing you time, space, & money. Free up the mental energy! Share on X22) Hire a professional organizer.

As a Certified Professional Organizer®, I see how much my clients get out from support to make difficult decisions and develop systems to surmount those challenges. Find a professional organizer near you (or a virtual organizer) by using NAPO’s search function. You may also want to consult with our colleagues in the Institute for Challenging Disorganization.

Whether you need to reinvigorate a closet, learn how to use Evernote to get your productivity zipping along, or downsize Grandma’s house so she can move to Boca, professional organizers can show you the way. We’re not just experts in organizing stuff, but experts in helping you figure out how best to organize your ways of thinking and living.

23) Be gentle with yourself.

Getting organized and being productive is a constant battle between your goals and other people’s expectations of you. Focus on what you need and want.

In the words of Mary Oliver poem The Summer Day, “What is it you plan to do with your one wild and precious life?”

The purpose of organizing and being more productive is to make your life easier — so that you can spend it doing the things you like with the people you love.

Happy New Year! Happy GO Month!

Organize Your Annual Review & Mindset Blueprint for 2023

The holiday week is the perfect time of year to plan for next year, to set goals and intentions, and get a fresh start. Of course, you don’t need a new year for that. Check out Organizing A Fresh Start: Catalysts for Success from this past September to see all the ways you can find inspiration for fresh starts quarterly, monthly, weekly, and each day.

But before we can design the coming year, it’s essential to review the past, and to get a handle on what worked (and didn’t) so that we can use that knowledge to set us up for future successes.

LOOK IN THE REAR-VIEW MIRROR

On the very businesslike side of the productivity realm, this is called an annual review. People in the corporate world often experience this in terms of a sometimes-feared, often-maligned annual performance review.

That’s where you tell your boss how you think you did during the course of the year (in hopes of a raise, promotion, and an atta-boy/atta-girl), and your boss tells you how the company thinks you did (in hopes that you’ll be so thankful to have a job, you won’t notice that any extra money is going to the CEO’s newest yacht).

But a personal annual review, which can cover both lifestyle and professional topics, is solely for your own benefit. It’s to help you figure out the who, what, where, why, and how of your past year so that you can find the common threads (or snags) in your successes (or challenges).

Gather Supplies

The process is as formal or informal as you’d like, but I encourage you to start with some of the tools you use to create the structure of your year:

- planner or calendar

- journal

- correspondence — email or text threads — with your best friend, accountability partner, or mastermind group

- a sense of your values

With a pen and paper (or fresh Evernote note or blank document), sift through what you’ve written and logged about your life over the past year. Where did you go, with whom did you meet, and what did you do? As if you were reading a mystery, you’ll find yourself noticing clues to patterns in your year. (Feel free to wear your Sherlock Holmes deerstalker hat.)

There are a few kinds of clues, and depending upon your life and work, as well as what you value, different clues will yield evidence for making different kinds of decisions.

Know Your Values

Speaking of values, these are not uniform across nations, regions, communities, families, or even periods of our lives. In the United States Army’s Basic Combat Training, they focus on seven values: loyalty, duty, respect, selfless service, honor, integrity, and personal courage. Conversely, the immigration portal for the Durham Region of Ontario, Canada lists Canadian values as “equality, respect, safety, peace, nature – and we love our hockey!”

If you’re not quite sure how to identify the values that help you plan your life, here are some great resources:

Nir Eyal’s 20 Common Values [and Why People Can’t Agree On More] (Eyal is the author of Indistractible: How to Control Your Attention and Choose Your Life.)

James Clear’s 50 Core Values list (Clear is the author of Atomic Habits.)

Brené Brown’s 118 Dare To Lead List of Values (Brown is the author of Dare to Lead, as well as Daring Greatly, Rising Strong, and The Gifts of Imperfection.)

The Happiness Planner’s List of 230 Core Personal Values

Some people highly value achievement and contribution; for others it’s balance and inner harmony. For me, it’s knowledge, usefulness, and humor.

We’ll get to how to use your values in a bit. For now, it’s just helpful to go through one (or more) of these lists and identify from three-to-five overarching values that resonate with you and how you aspire to live your life.

Ask Qualitative Questions

The Good

- What challenges made me feel smart, empowered, or proud of myself this year?

- What did I create?

- What positive relationships did I begin or nurture?

- Who brought delight to my life?

- Who stepped up or stepped forward for me?

- What was my biggest personal highlight or moment I’d like to relive?

- What was my biggest professional moment I’d want to appear in my bio?

- What’s a good habit I developed this year?

The Neutral

- What did I learn about myself and/or my work this year?

- What did I learn how to do this year?

- What did neglect or avoid doing out of fear or self-doubt?

- What did I take on that didn’t suit my goals or my abilities?

- What was I wrong about? (Note: Being wrong isn’t a negative. Not one of us knows everything. In the words of Dr. Maya Angelou, “Do the best you can until you know better. When you know better, do better.”

The Ugly

- What challenges made me feel weaker or less-than?

- Whom did I dread having to see or speak with this year?

- Who let me down?

- Whom did I let down?

- What did I do this year that embarrassed me (professionally or personally) or made me cringe?

- When did I hide my light under a bushel?

- What am I faking knowing how how do? — Instead of pretending you know how to do something but are choosing a different path, ask for help. Make decision about what to do from a position of strength rather than weakness.

- What’s a bad habit I regret taking up or continuing?

- Where did I spend my time wastefully or unproductively? (It’s social media. For all of us.)

- Where did I spend my money wastefully or unwisely? (Target? Let’s take a poll. Was it Target?)

Although most of these are questions I’ve developed over the years, the inspiration for including this list came from the Rev Up for the Week weekly newsletter put out by Graham Allcott, author of How to Be a Productivity Ninja, among other titles.

2022 Year In Review: 50 Powerful Questions To Help You Reflect, which includes questions for looking back as well as looking ahead.

Ask Quantitative Questions

The quantitative questions, the ones that can be measured in “how much?” or “how many?” or “how often?” will depend on the metrics by which you’ve measured yourself in the past (or expect to in the future).

I’m not a quantitative person because I find that raw numbers rarely reflect context. If you asked “how many pounds did I lose in 2022” but you were pregnant or recovering from an illness or in mourning, the answers would be useless. It reminds me of the quote variously (but likely inaccurately) attributed to Albert Einstein:

Everybody is a genius. But if you judge a fish by its ability to climb a tree, it will live its whole life believing that it is stupid.”

If you’re a fish, don’t pick metrics for monkeys.

*Everybody is a genius. But if you judge a fish by its ability to climb a tree, it will live its whole life believing that it is stupid.* If you're a fish, don't pick metrics for monkeys. Share on XThat said, if you have metrics that matter to you, by all means, measure. But again, make sure those metrics measure what you actually value. Some ways to measure:

Professional Efforts:

- How often and when was I asked to contribute (to a team effort, a podcast, a conference)?

- How much revenue did my efforts bring in?

- How many clients did I serve?

- How many new clients (or projects) did I bring in?

Physical Health:

- How many reps can I do of X? (Or, by how many reps did I increase my stamina for X?)

- How many steps or miles did I walk (or run or swim or pedal)?

- How often did I “complete the rings” on my Apple Watch or hit the goals set in my app?

Financial Strength:

- By how much did I decrease (or increase) my debt?

- How much did I invest? (Note: Measuring the performance of your investments is important for driving your future investment decisions, but actual investment performance isn’t a measure of your abilities — I mean, unless you’re a stockbroker. You don’t control global markets; you don’t control the products or services or marketing strategies of the companies in which you invest. Please don’t judge yourself by your stock performance.)

Ask How Your Year Measured Up To Your Goals and Values

Goals and values are different. In both qualitative and quantitative ways, we can flip through our calendars and our LinkedIn achievements to see where we’ve hit the benchmarks we’ve set for ourselves. We all know about SMART goals and the importance of them being measurable.

But values? You can’t check off a box to say you’ve “done” a value. But that doesn’t mean you shouldn’t consider whether your accomplishments are in line with your actual values.

We all have things at which we’re stellar, things that we may consider (or others may consider) to be our superpowers. I have a mug that reads, “I WRITE. What’s your superpower?” Writing (and talking — so much talking) is intrinsic to who I am. Because knowledge, usefulness, and humor are my values, when I’m writing this blog, I’m in alignment.

But for most values, it can be hard to tell and certainly hard to measure. One method to measure if you’re living in alignment with your values (and the goals toward those values) comes from the Acceptance and Commitment Therapy (ACT) modality.

ACT is a type of psychotherapy that focuses on emphasizing actions that increase well-being, and the ACT Values Bulls-Eye helps people not only identify their values but envision how well they’re doing in trying to live in alignment. This short video offers some guidance for using a simplified version of the Bull’s-Eye; online, you’ll find a variety of modifications for circles, stars, and graphs.

Get Creative in Describing Your Year

Not everyone wants to feel like they’re putting themselves through a performance interview. But there are creative ways to look at the year you’ve just survived.

Morgana Rae, a wealth and life coach who transforms people’s relationships with money, had an interesting idea in her newsletter last Friday. She said that she had a “one-step super trick for empowerment” in the new year — to end the prior year with a headline!

Don’t worry, you don’t have to pretend to work for the New York Times or a clickbait web site. Morgana’s was “2022 was the year that nothing worked out as planned, but everything worked out.” In 2009 (the year I was hospitalized 6 times and mostly couldn’t work with clients), my headline could have been, “2009 was the year that gave me lots of entertaining-in-retrospect cocktail party anecdotes.”

In 2009 (when I was hospitalized 6 times and couldn't work), my headline could have been, *2009 was the year that gave me lots of entertaining-in-retrospect cocktail party anecdotes.* Share on X(Note: In January, Morgana is releasing a 10th Anniversary Edition of her best-seller, Financial Alchemy.)

If you’re pithy enough for headlines, could you end 2022 by describing it as a novel or a movie? You were the protagonist, but who (or what) were the heroes and villains of the story? What was the plot? Try to accurately — and/or entertainingly — describe your year in a paragraph.

Don’t Reinvent the Wheel

You don’t have to figure this out on your own. The free, downloadable YearCompass is a popular resource for a reason. Download this fillable, printable PDF — print the booklet version and fill it out by hand, or type your answers in the digital version — and explore the creative questions to get a deep, abiding sense of what your year really meant, and how to approach the coming year.

DESIGN A BLUEPRINT FOR NEXT YEAR’S MINDSET

Once you have a strong handle on the year that was, you can begin to set your goals and benchmarks for the year that will be. But writing down goals and creating a task list isn’t always motivating. That’s because we’re not all motivated the same way. In Gretchen Rubin‘s Four Tendencies Quiz, I’m definitely an Obliger.

If you’re not familiar with the basics of the Four Tendencies, the categories reflect how we respond to expectations. As an Obliger, I respond best to outer expectations — and so accountability (through working with my accountability partner, the magnificent Dr. Melissa Gratias, and with my Mastermind Group) is the key to meeting my goals. Inner expectations? Yeah, I blow right past those.

You might be an Obliger, Upholder, Questioner, or Rebel. Upholders do well with discipline; Questioners need to know the “why” behind the what; and Rebels? Well, I suspect everyone’s still trying to figure out how to get Rebels to do what they believe they want to (and should) do.

Resolutions

Beyond figuring out what kind of support works best for you, it helps to borrow from marketing. For a long time, resolutions had a good long run. But the truth is most people break their resolutions. (Read James Clear’s Atomic Habits for a handle on why that is.)

So, with that in mind, let’s go back to Graham Allcott and his video, How to Not Suck At Your New Year’s Resolutions.

And if you still want to make resolutions, take a peek at Vox’s In Search of an Attainable New Year’s Resolution, science-based piece (including advice on a values-based approach).

But again, I’m less a fan of making resolutions, and more inclined to cheer on a big, bold way to set an attitude for the coming year. There are a few we’ve discussed at Paper Doll HQ over the course of the years.

Word of the Year

Pick a Word of the Year to help you focus your attentions on your intentions.

Another way to think of it is, what is your theme for 2023?

Whether or not you define what you will do with goals or resolutions, choosing this word helps clarify the approach you will take. To quote myself from four years, ago, the idea is that you pick a word that “encapsulates the emotional heft of what you want your year to look and feel like.” Each time you agree to take something on, you can ask whether that event or project resonates with the word you’ve picked.

Decide for yourself what the rules are. Do you want to pick a word based on what your life was missing this year? Or go for a bold new direction in which you want to take your life?

As a colleague embraced retirement this year, she picked the word “humor” for 2022 and used her newfound time to post something funny every day on social media, bringing levity to her friends.

I consider my word as carefully as picking the three wishes I’d request from a genie. I think I’ve seen too many episodes of the Twilight Zone; I know that if something isn’t worded well, I can feel cursed. The year I picked “resilience,” I ended up with too many unfortunate things from which to bounce back.