Archive for ‘Seniors’ Category

How to Organize Your Response to the 2024 National Public Data Breach

Hack! Breach! Data theft!

You see a news story about yet another company getting hacked, or you receive a letter from some service provider telling you that their servers were “breached.” Sometimes the letter offers advice, or perhaps a year of free credit monitoring.

Organizing your records, passwords, financial resources, and entire identity to protect against identity theft is exhausting. It would be understandable if you tend to tune out any news about such hacks and breaches.

Over the past week or so, however, you might have heard about a particularly nasty breach, leaving bad guys with access to millions of Social Security numbers. That probably made you sit up and take notice…and get queasy.

THE UNPRECEDENTED BREACH OF SOCIAL SECURITY NUMBERS AND MORE

At the outset, I should note that contrary to popular perception — the Social Security Administration was not hacked. The federal government wasn’t breached.

Who Got Hacked and When?

A Florida-based data brokerage company, National Public Data (NPD), got hacked. You may wonder how NPD got so much personal data in the first place. It, like many companies of its kind, scrapes data from wherever they can, including federal and state public records databases like voter registries, DMV records, professional license filings, birth/marriage/death records, criminal and civil course records, and non-public databases.

So, private information, by way of how the modern world works, gets stored somewhere over which we have no control, and then scraped, gobbled up by companies like NPD. They then turn around and sell our private data to anyone willing to pay — from employee background-check sites to private investigators (not cool, Sam Spade!) to data resellers.

According to NPD, the crime took place in December 2023; it just took a while to become known (and then a lot longer for NPD to own up to it). It’s not clear who actually stole the data.

What is clear is that the breach became known in on April 7, 2024, when a hacker group identified as USDoD posted on the dark web, offering an estimated 2.9 billion individual rows of data records for $3,5000,000. Jeez Louise!

At this point, various “bad actors” (by which I don’t mean David Hasselhoff or Pauly Shore) began posting on the dark web and leaking about the availability of the purloined data.

The breach was reported by the Daily Dark Web in a piece entitled NationalPublicData.com Hack Exposes a Nation’s Data:

The leaked data, which spans from the years 2019 to 2024, is of unprecedented magnitude, comprising 2.9 billion rows. The sheer volume of information involved is monumental, with the compressed data reaching 200GB to a staggering 4TB when uncompressed. The breached database includes comprehensive citizen information, firstname, lastname, middlename, name_suff, address,city, county name, phone 1,aka1 fullname, ssn and more. Such a massive breach raises serious concerns regarding data privacy, security, and the potential for widespread misuse or exploitation.

However, Daily Dark Web also noted that there was “a strong possibility that the assertion may be exaggerated and that the data could have been scraped from publicly available sources. Additional scrutiny and analysis are required to validate or refute these allegations.”

You’d expect that the mainstream media might attack this story like a dog with a bone, but few outlets took any notice. Instead, they focused on all the usual wars, natural disasters, sports, bird flu, Taylor Swift, and Congress trying to shut down TikTok.

Then, on July 21, 2024, someone leaked exactly what was stolen. Members of the cybercrime community Breachforums released in excess of 4 terabytes of data they claimed had been stolen (though not by them) from NPD.

Photo by Markus Spiske on Pexels.com

What Did the Hackers Get?

The breach contained massive database holdings at the nationalpublicdata.com domain, stealing Social Security records, phone numbers, physical address histories, and some email addresses of many millions of Americans. Information datasets from Canada and the United Kingdom were also included.

Per Troy Hunt, a regional director of Microsoft and founder of Have I Been Pwned (a site that helps people determine whether their email address has been included in data breaches), there were also 70 million rows from a database of U.S. criminal records.

Techcrunch referred to the data stolen as “partly legitimate — if imperfect.”

Brian Krebs of Krebs on Security further wrote that Atlas Data Privacy Corp. researchers found that there were 272 million unique Social Security Numbers in the entire records set, and that most of the records had a name, Social Security Number, and home address; approximately 26% of those records also included a phone number.

Apparently Atlas verified a subset of 5,000 addresses and phone numbers, and found that those records were, with “very few exceptions” for people born before January 1, 2002. So, maybe your college student is safe. But the rest of us? Oy.

Atlas also found that the average age of consumers in the records was 70 — with approximately two million records related to people who would be at least 120 years old at this point, so at least some of have already shuffled off this mortal coil, taking their credit lines with them.

This still leaves a lot of questions. Which data got out? Was it accurate or out of date? Which data was for deceased persons and which for real, live peeps? And what good data is paired with bad data?

If you’re feeling cyberwonky, read Troy Hunt’s Inside the “3 Billion People” National Public Data Breach. Hunt states that, “[t]here were no email addresses in the Social Security number files.” So, figuring out how bad it all is may take a while, because it’s hard to know what info is current and properly matched to your public identity.

Where Do Things Stand Now?

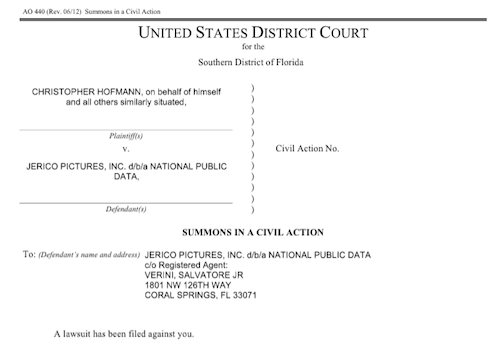

Mainstream media finally took notice on August 1, 2024, when California resident Christopher Hoffman filed a class action suit. Even then, NPD didn’t respond publicly until Friday, August 16, 2024, more than two weeks later, four months after the breach was originally reported, and more than eight months after the initial crime occurred!

And when NPD finally did post a milquetoast-y comment, it merely said that the breach involved a “third-party bad actor that was trying to hack into data in late December 2023, with potential leaks of certain data in April 2024 and summer 2024.” Well, duh.

That’s not even all! According to two Bleeping Computer pieces, National Public Data Confirms Breach Exposing Social Security Numbers, and Hackers Leak 2.7 Billion Data Records with Social Security Numbers, on August 6, 2024, “another threat actor known as Fenice shared for free the most comprehensive variant of the database with 2.7 billion records, with multiple records referring to a single person” and further, the “threat actor known as “Fenice” leaked the most complete version of the stolen National Public Data data for free on the Breached hacking forum.”

Meanwhile, in finger-pointing worthy of the Spider-Man memes, this Fenice claimed that the data breach was actually conducted by a different threat actor named “SXUL” rather than USDoD. (What, nobody’s named Mike anymore?)

(I created this from a meme generator. Apologies for offended artistic tastes.)

So, our data was stolen, priced for sale for $3.5 million, and then offered up for free to hackers, but nobody told us regular folk until the lawyers wanted attention for a class action suit?

If you feel like you need an aspirin, you’re not alone. Nothing about this feels particularly organized. Or fair.

This class action suit is a big deal, because, as the plaintiff’s law firm explained in a press release, Hoffman was not a customer of NPD. None of us were.

Thus, unlike when we get those letters from our doctor’s office or credit card companies, we never voluntarily gave our personal information to NPD in the first place, so most Americans (and Canadians, and citizens of the UK) won’t even know if they’ve been affected by the breach until or unless something along a continuum from hinky to financially catastrophic happens.

As a result, it’s essential to take action and organize your resources against potential fallout.

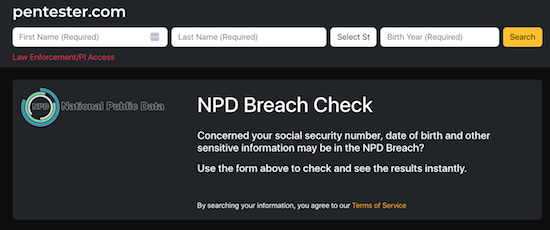

HOW TO KNOW IF YOUR INFORMATION WAS HACKED

The cybersecurity firm Pentester accessed the files included in the breach and created a free database/breach check of the stolen information — but with Social Security numbers redacted, birthdates partially redacted, and phone numbers and street addresses in the clear.

I know it doesn’t look very impressive, but experts and journalists, including at Time Magazine, have recommended using it.

Enter your first name, last name, state, and birth year. It will search billions of leaked records and note whether your information was included in the breach.

If your data isn’t found, you’ll get an error message instead of a list of records. Yay! Except that’s the starting point, not the finish line. Boo!

- Check every state you’ve lived in. Ever.

- Check your maiden name, or any other name by which you’ve been known, legally or otherwise.

- Check for your significant other, your parents, your kids, and pretty much everyone you care about. (I mean, you could also search for your horrible boss, the kid who stuffed you in a locker in seventh grade, and your ex-mother-in-law, just to enjoy a little schadenfreude. I won’t tell.)

However, will only tell you is whether your information is out there, somewhere, naked. Your next step is protect that data from molestation as best you can.

PROTECT YOURSELF AGAINST YOUR DATA BEING USED AGAINST YOU

Monitor your financial life

You should already be regularly checking your bank accounts and credit card statements for anomalies. Either log in to one at a time or use a financial dashboard like Empower, Rocket Money, or one of the other popular alternatives to the late, lamented Mint.

Next, monitor your credit reports.

Longtime Paper Doll readers know that I always advise using AnnualCreditReport.com, which, by law, guarantees a free credit report from each of the three credit reporting bureaus per year. Better yet, after the onset of the COVID pandemic and the related financial chaos that ensued, Equifax, Experian, and Trans-Union temporarily offered free weekly credit reports.

The bureaus extended those offers twice over the years, and as of last October, the Federal Trade Commission reported that AnnualCreditReport.com will now permanently make available weekly credit reports at no charge so that consumers can dispute errors, be watchful for any fraudulent account openings or changes, and report identity crimes at IdentityTheft.gov.

While you’re pulling your own credit report, pull them for your children, too. Even the existence of a credit report for a child who has never applied for credit is a big, honking sign that something fraudulent may have occurred.

Place a fraud alert on your credit file

This requires that any creditors contact you before making changes to any of the accounts you already have or before opening any new accounts in your name. You needn’t contact all three credit bureaus; rather, once you request a fraud alert with one bureau (say Equifax), the other two (Experian and Trans-Union) will be notified.

Per a law passed in 2018, fraud alerts stay in place for a full year (unless you rescind it earlier), and victims of identity theft and related crimes can secure an extended fraud alert for seven years. Previously, fraud alerts lasted only 90 days.

Also, the law requires that each of the credit reporting bureau must automatically send you a free credit report after you request a fraud alert. Scrutinize them carefully.

To request a fraud alert, contact one of the three credit bureaus’ fraud alert divisions:

- Equifax — or call 1-800-525-6285

- Experian — or call 1-888-397-3742

- TransUnion — or call 1-800-680-7289 (Note: an extended TransUnion fraud alert must be requested by mail.)

But before you choose this path, there’s a better option.

Freeze your credit file

A credit freeze is different from a fraud alert. While the fraud alert says that creditors have to contact you before changing or opening accounts, a freeze says, “Nope. Do not pass GO. Do not collect $200.” A freeze prevents any new loans or credit from being taken out in your name — even by you!

A credit freeze is different from a fraud alert. A fraud alert requires creditors contact you before changing/opening accounts; a freeze says, *Nope. Do not pass GO. Do not collect $200.* A freeze prevents any new loans/credit from… Share on XThe freeze stays in place until or unless you revoke it. So, if you need to buy a new car, seek a student loan or mortgage, or apply for a credit card, you can temporarily remove the freeze. After you secure funding, you can put the freeze back on.

Ice Photo by Enrique Zafra at Pexels.com

- Contact each of the three credit bureaus.

Unlike with the fraud alert, where you only have to contact one of the credit bureaus, you’ll need to contact all three at the following freeze division links or numbers:

-

- Equifax — or call 888-397-3742

- Experian — or call 866-478-0027

- TransUnion — or call 800-916-8800

You must create an account with login credentials before you can proceed to request a freeze.

- Keep your PINs in a safe place.

When you place a freeze on your credit, you’ll get PIN. You’ll need those PINs to defrost — I mean, unfreeze — your credit later. (Note: I helped a less tech-savvy client in her 80s accomplish this on Friday, and we learned that TransUnion no longer requires a PIN; your TransUnion login will suffice.)

Where you safeguard your PIN depends on the standard methods that you already use; you don’t want to be dependent upon your memory of an out-of-character decision.

- Write PINs down and put them in your fireproof safe or safety deposit box.

- Enter PINs in your digital password manager.

- Put PINs in your secure password book in code.

Do NOT put them on a sticky note affixed to the front of your computer. Do NOT write them in a little notebook that you take out of your home.

- Protect the credit files of your loved ones and those in your care

That 2018 law guarantees that you can freeze (and unfreeze) your own credit for free. (This is different from a credit lock, which requires a subscription to a credit bureaus’ services.) In addition to setting a freeze for yourself, you can obtain a credit freeze for your children under the age of 16. (Minors aged 16 or 17 may request their own freezes.)

Photo by Julia M Cameron on Pexels.com

Because minors can’t apply for loans, people rarely check children’s credit history. In theory, there shouldn’t even be a credit bureau file for a child, so when young adults start out trying to get student loans or credit cards, they may be in for a shock to learn that someone has already destroyed their credit!

For more on preventing children from being the victims of identity theft, check out:

https://consumer.ftc.gov/articles/how-protect-your-child-identity-theft

Additionally, if you serve as a conservator or guardian, or if you hold someone’s Power of Attorney, you may secure a free credit freeze for them, as well.

Why else should you get a credit freeze?

Any time you are at greater risk of identity theft, whether through a massive data breach, a run-in with a bad roommate, a breakup with a creep, or you’ve had your wallet stolen or your home burgled, a credit freeze can give you peace of mind that nobody will be able to access credit in your name.

Similarly, if elderly relatives develop dementia or anything that impairs their cognitive capacity, they can become prey to predatory lenders and charlatans selling everything from scammy auto repair warranties to non-existent services. A credit freeze prevents scams from moving past the spam stage.

Military Fraud Alerts

Members of all United States military branches have an additional resource that predates the 2018 law. They can set active duty alerts, allowing them to place a fraud alert for one year, renewable for the entirety of their deployment.

For Equifax, use the online form for an Active Duty Alert or call 800-525-6285. Meanwhile Experian has an online form but no phone number, and TransUnion has a phone number (800-680-7289) but no online form.

As a bonus, securing an active duty alert prompts the credit reporting agencies to remove a service member from the marketing lists for sneaky pre-screened credit card offers. (Service members can request to be added back, but who wants that junk mail?)

DON’T GET SCAMMED

Even partial information allows scammers to contact you, pretending they’re preventing scams. A caller might fake being from your bank or credit card, alerting you to a hacking risk. They may request you log into one of your accounts and change passwords (to something they provide) for “testing” purposes that might sound reasonable if you’ve been interrupted while chasing a toddler or running a meeting.

Photo by mohamed_hassan from PxHere

Be vigilant. If contacted by phone, text, or email, don’t respond, even (or especially) if the contact appears to already have some of your data. They’re using what they DO have to get you to reveal what they DON’T have — more of your private information. Call your financial institution directly.

The Social Security Administration won’t call you. They won’t email. They won’t text you. (Government sites may email or text two-factor authentication codes when you log into a federal site, like ssa.gov, but that’s initiated by you.)

My March post, Slam the Scam! Organize to Protect Against Scams, focused mainly on scams targeting seniors, but will help you protect yourself and loved ones from most common scams, and provides resources to help you learn more.

The Hill‘s August 15, 2024 piece, Was your data leaked in massive breach?: How to Know, and What to Do Now, has a good point about the likelihood of being at risk:

“If you’re a high-value individual that maybe has a high net worth or works at a company that they can extort you, you might actually be a real target,” Kyle Hanslovan, CEO of cybersecurity firm Huntress, previously told Nexstar. “For the masses though, the everyday common person, you’re more of a target of opportunity.”

Most people shouldn’t spend too much time worrying about what may happen if their information ends up in the wrong hands. Instead, Hanslovan recommends keeping an eye on your important accounts and making sure you’re prepared to act in case something does go wrong.

“It stinks for privacy, but it kind of normalizes just what’s happening,” Hanslovan said. “It doesn’t make it right, and it definitely doesn’t wave, you know, a company’s true fiduciary responsibilities to protect your data.”

Someone should tell NPD that.

Other Ways to Keep Bad Guys From Using Your Data to Hack You

- Make your passwords long and complex. Using at least 16 characters, with a mix of capitals, lowercase, numbers, and special symbols, will make it hard to hack you.

Image Source @2024 Hive Systems

- Use a password manager for all your longer, more complex passwords.

- Turn on two-factor or multifactor authentication for as many of your online accounts as allow it. (That’s like when you get a text or email with a code to enter before your login is authenticated.) Alternatively, you can use an authenticator app.

- Set up account alerts for your bank, investment, and credit card accounts, particularly to flag online or in-person purchases or ATM transactions outside of the US.

- Keep security software updated on your computer and phone.

- Don’t check financial accounts on insecure Wi-Fi networks; wait until you’re home, on secured WI-Fi network.

WHAT TO DO IF YOUR DATA IS USED FRAUDULENTLY

- File a police report.

- Report fraud to the Federal Trade Commission.

- If someone uses your Social Security number, report it at IdentityTheft.gov.

ONE LAST WEIRD THING

You may have noticed something odd about the class action suit. You’d expect National Public Data’s parent company to have a tech-leaning name, like InfoDynamics or Identidata.

Nope. The parent company is Jerico Pictures Inc., a Florida-based film studio owned by Salvatore (Sal) Verini, Jr., a retired deputy with the Broward County Sheriff’s office who fashions himself as an actor, producer, and writer.

Verini is also listed as the owner of companies called Trinity Entertainment Inc., National Criminal Data LLC, Shadowglade LLC (which sounds like a housing development in a horror movie produced by a company with a name like Jerico Pictures), and Twisted History LLC, which sounds like a joke.

Meanwhile, victims of data hacking won’t be doing a lot of laughing.

REFERENCES

As a Certified Professional Organizer®, I often help clients protect their identities and financial information. However, I am not a cybercrime specialist, nor do I play one on television. To research the specifics of this breach, in addition to the many government and tech-oriented links in the above post, I used a clarifying mainstream sources, including:

- 7 On Your Side steps to take to keep personal information safe amid latest data breach (WABC-TV)

- Hackers May Have Stolen Your Social Security Number in a Massive Breach. Here’s What to Know. (CBS News MoneyWatch)

- How to Check if Your Information Was Compromised in the Social Security Number Breach (Time Magazine)

- It’s Free to Freeze Your Credit: Here’s What You’ll Need to Do (HerMoney.com)

- The Weirdest ‘3 Billion People’ Data Breach Ever (The Verge)

- What to Know about Credit Card Freezes and Fraud Alerts (FTC.gov)

Keep your eyes open and your personal information close to the vest.

Organize to Help the Seniors in Your Life With Technology

This post was originally published on May 27, 2024, and has been updated as of September 8, 2025 to reflect additional information and resources, including revised links.

We love technology. However, it does not always love us.

Technology is not always (or even often) intuitive, which makes it hard to organize the technology and the content provided by the technology. This is especially true for our parents and grandparents (or ourselves, if we happen to be seniors).

Whether the seniors in your life embrace technology or eschew it, the digital realm has a lot to offer them.

Health and Safety Technology

- Wearable fitness trackers like Fitbit, Garmin, and Apple Watch (and associated apps) for tracking:

- nutrition and calories burned

- steps taken and stairs climbed

- health metrics like heart rate, blood pressure and glucose levels

- Reminder alerts and alarms for taking medicine and testing blood pressure and blood glucose.

- Phone-based magnifiers for helping read medicine bottle labels and prescription instructions.

- Phone-based cameras for supporting memory (noting parking locations, remembering hotel names and room numbers, etc.).

- Videoconferencing for telehealth allows seniors to stay connected with their physicians for regular visits and making inquiries without having to venture out to drive in inclement weather or seek rides when an in-person appointment isn’t necessary.

- Fall detection and emergency hotline hardware and software, or medical alert systems, allow seniors to get help if they suffer falls or medical emergencies in their homes, even if they are not positioned near their phones or are unconscious.

Paper Mommy and I call these the “I’ve fallen and I can’t get up” buttons after the famed grating commercials.

They range from wearables like bracelets and pendants to wall-based systems, and are connected through phone lines to base stations, so if someone suffers an emergency, they can “call” through that base station, like an intercom. If the user does not respond to the service’s inbound call, emergency services are dispatched. Common systems include Life Alert, Medical Guardian, and ADT Medical Alert.

Smart Home Technology

As with health technology, a variety of smart home technologies can make life easier and more convenient for all users, but especially seniors. These include:

- smart lighting and blinds

- smart plugs and timers that turn appliances off and on

- digital monitoring systems for temperature control, CO2 detection, humidity, and air quality

- smart thermostats

- robot vacuums

- GPS-based trackers to locate lost items

- digital doorbell cameras to help monitor who is at the front door (delivery workers, visitors, bad guys, ding-dong-ditchers, etc.)

Digital monitoring and home management can make it easier for seniors with low mobility or low vision to be able to care for their homes and personal comfort with minimal effort.

For more on smart home tech for seniors, the New York Times’ Wirecutter site has a great piece on the 14 Best Smart Home Devices to Help Aging in Place.

Entertainment and Social Connection Technology

There is no age limit on enjoying books, TV, movies, or music, but the same technology that brings a wider variety of options into our homes, but these technologies are not always intuitive. It’s not that Spotify or Netflix is easier to use when you’re 25 than when you’re 85, but those who have always lived with technology are quicker to note and understand user interface changes and make quicker guesses as to where missing options may be hiding.

Retirees who no longer interact with others in the workplace or at as many social gatherings as previously can benefit from all the modern offerings, including:

- Smart TVs with cable or satellite programming

- Streaming entertainment from mainstream services like Amazon Prime, Netflix, Apple+ TV, Hulu, as well as niche programming services like AcornTV or BroadwayHD

- Music streaming services like Spotify, Apple Music, Amazon Music, or Pandora

- Podcasting apps

- Book and audiobook services and apps like Audible, Libby, and others that allow you to purchase entertainment or borrow from your public library.

When Tech Go Wrong

We’ve all dealt with the frustration of tech going wonky. The difference is that the younger we are, the more likely we are to recognize a problem that we’ve seen before and recall how to solve it. We’re also more likely to visit the service’s FAQ pages or Google the problem. Seniors, however, may be both less likely to have experienced (or recall experiencing) similar problems and less adept at digital search and the right prompts to solve the problem easily.

When I got in the car to run errands this weekend, in place of the digital clock on my car’s navigation screen, it just said “–:–“ so I immediately went to the on-screen settings icon. However, on the resulting screen, the date/time icon was greyed out. I vaguely recalled this having happened once before, so I wasn’t immediately worried that my car was “broken” or that there was an expensive onboard computer problem.

First, I checked social media reports of widespread problems. That’s still my go-to for “is it happening right now” technology issues unless it’s an internet-based issue, in which case I follow the steps I described in Paper Doll Organizes the Internet: 5 Tools for When the Web Is Broken.

Then I Googled “Kia date/time setting greyed out and not working” on my phone. I got varying reports of it being a satellite issue that would self-correct; others suggested pulling one of two different fuses and/or resetting the onboard programming.

I can just shout, “Hey, Siri, what time is it?” so this wasn’t an emergency. Thus, so I didn’t get flustered, and figured if the problem continued I would check it out later in the weekend. An hour later, after a trip to Walmart (where the cashierless payment technology had everyone frustrated), I returned to my car to find the clock working again.

Now, take a moment to imagine your Great-Grandpa dealing with this clock kerfuffle, getting progressively more annoyed that the auto manual’s index and table of contents yielded no immediate solutions. Would he head to the search engines or YouTube? Would he become agitated?

We all love technology and we all hate when tech doesn’t work as it’s supposed to. The only difference is that the younger we are, and the more privileged (financially, socially, and educationally) we are, the more exposure we’ve likely had to potential solutions. The best thing we can do to make technology easier for our elders is to help them when we can, and connect them to others who can help them when we are not able to do so.

HOW TO HELP THE SENIORS IN YOUR LIFE WITH TECHNOLOGY

Let’s get the giggles out of the way, first.

Don’t laugh at them

When possible, do laugh with them.

This should be obvious. But it’s also hard. While serving as Paper Mommy‘s tech support over the phone, I kept trying to point out the lock icon so that she could recognize secure websites.

Because we couldn’t see one another’s screens, I was trying to give her landmarks, and I could tell she was looking in the right location in the URL bar at the top of the screen, but she kept not seeing the lock icon. Finally, Paper Mommy, frustrated, insisted “It’s not there! The only thing there is something that looks like a little purse.”

![]()

By Santeri Viinamäki, CC BY-SA 4.0

Um. OK. I had to laugh. While yes, to anyone thinking in terms of technology, that secure URL icon is a padlock. But if you’re in your 70s or 80s and haven’t been technology-focused for your entire adulthood, yep, it’s a purse. A green handbag.

Start with, and explain, the basics

Use proper lingo when you can, but if your person just can’t get a handle on remembering the term “scroll bar,” try saying, “Do you remember the vertical bar that makes the screen move up and down, like an elevator?” Use vivid, memorable language, and be prepared to backtrack. Often.

Let them make mistakes

Many seniors are afraid that they will “break” the computer or gadget by clicking on the wrong link. Assuming you’ve covered the basics of avoiding phishing and other scams (see below), assure them that changing settings isn’t going to void the warranty or damage the software or the hardware.

Do not condescend

If this senior is your senior (parent or grandparent), remember how many times they needed to help you learn how to use a spoon or spell your name.

Be patient

Go slowly and be as patient as you can be. (And if you can’t be patient with your mom even though you are known for being patient with clients or colleagues, recognize that you and your favorite senior will have different perspectives, and find them an alternate IT help desk, once that doesn’t look like you.)

Explain online dangers and prepare them for what they should NEVER do

Technology doesn’t need to be scary, but it often is, and especially so for seniors. Teach the seniors in your life about phishing scams, how to identify the true source of emails (by hovering over the sender name and looking at the actual domain name of the address), how to look for secure sites (and the “purse”), and how companies, banks, and the government will never call or email and ask for passwords or other information (or ask you to make urgent payments via purchases of gift cards!).

For more on this, refer to my post from March, Slam the Scam! Organize to Protect Against Scams.

Teach them where to look for resources and how to ask search engines for help

My mom once called me because every bit of text on her Facebook screen had turned German. I knew immediately that this was because Facebook had a word cloud of language names in the lower right-hand corner of the screen.

If you were holding an iPad (as she was) on the right side, it would be easy to press your thumb on one of the languages and change your settings. (Facebook has since moved this element off the main screen.)

I’d once accidentally turned my Facebook default language to French, and had to Google the solution, and my Google-fu is pretty strong. However, to the uninitiated senior, it can be tempting to ask a question as you might ask someone sitting next to you on the couch: “Why is my Facebook in German?”

However, to yield a more helpful answer (at least until our AI overloads take complete control), a better query might include, “revert Facebook default language from German to English.”

Search engine language is not intuitive, but we can all — including seniors — learn better queries to find help more quickly.

Customize accessibility settings

When the seniors in your life get new devices, sit down with them to customize the accessibility and assistive settings:

Sometimes, just making text larger, increasing display brightness, or addressing basic accessibility issues will make the entire navigation process easier for them. However, there’s a ever widening range of accessibility tools that can making digital devices easier — or even a joy — for any user, not just seniors.

For addressing visual or hearing impairments, magnification/zoom settings, larger text, screen readers, high contrast mode, live captioning, voice assistants, and LED flashing (for notifications for the hearing impaired) all support smoother use. For those with mobility or dexterity obstacles, you can customize accessibility shortcuts, create “sticky” keys (so key combinations aren’t required), and assistive touch on-screen menus.

You can also activate device settings for “simplified views” or “easy mode” to reduce visual clutter and make navigation more intuitive.

There are also user-friendly apps like Be My Eyes to connect individuals with vision impairment with volunteers who can read labels or identify street or in-home objects.

Google’s Lookout app offers a similar assisted vision option.

BUILD ON INITIAL GUIDANCE WITH MORE COMPLEX TECH SUPPORT

Use Screen-Sharing Technology Options

If you’re helping a senior long-distance, it can be maddening for both of you. They may feel rushed, and you might be knocking your head against the wall because they can’t “see” what you know or believe to be right there!

At minimum, seek solutions that grant you remote screen viewing so you can see what they’re doing at their end and provide tactical directions. Be aware that there’s often a delay between what they’ve done and what you see, so just as when you’re working on the phone, try to discourage them from jumping multiple steps ahead.

In addition, there are remote access software programs and apps that allow you to manipulate someone else’s device from wherever you are. This is how the help desks at Apple and other big software and hardware companies guide you through IT troubles. Unfortunately, it’s also how scammers get access to your loved one’s computers, so it’s important that they understand not to provide this access to anyone they don’t know unless they are seeking the help of an authorized, respected technology expert and NOT someone who randomly calls and claims that “There is a problem with your Microsoft computer.” (There isn’t.)

I used to help Paper Mommy and my virtual clients with LogMeIn (which is no longer consumer-oriented) However, there are still free and affordable options for providing remote tech support to your beloved seniors, including:

- Zoom will let you request or offer remote access (as part of your account). It works on computers as well as iOS and Android devices.

- Microsoft Teams has a similar function for sharing content, as well as giving and receiving control.

- TeamViewer used to be free, but (as with most remote access programs, has moved to a subscription model for all users). Still, $24.90/year for a single user remote license should give you piece of mind that you can help your senior for less than fifty cents a week.

- Chrome Remote Desktop — This option is free and low-cost. You may find that you need to help your senior set up Chrome Remote Access first to make the process work.

All of the above options will work whether you and your senior have the same platform (Apple or Windows) or are mismatched. Other options require you to be using the same platform.

- Apple Mac users have a few options. If you’re both using Apple computers, you can make use of the free Apple Remote Login, but as with the Chrome option above, you’ll need to set it up in advance.

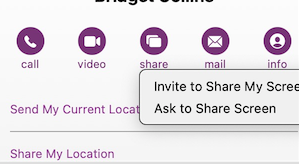

- Alternatively, without any advanced prep, (and again, if you’re both using Macs), you can use “Screen Share” from within the Messages app:

-

-

- Open the Messages app on your Mac.

- Select a conversation with your senior relative or friend. (If you haven’t ever texted with them, start a new conversation.)

- Click the “i” button in the upper right-hand corner of the window. A set of options will drop-down.

- Click “Share.”

- Ask your senior to share their screen. (Alternatively, they can also go to this same menu and invite you to view their screen.) They’ll get a pop-up requesting permission to share their screen with you. They need their “Control My Screen” option selected and should click “Accept.” From this point, you can control their Mac and show them what to do, step-step, or fix problems yourself.

-

Finally, I find it helpful to initiate a Facetime (Mac-to-Mac) call before starting the process, but you can also speak on the phone while troubleshooting.

- Windows users have similar built-in options, including Quick Assist and Windows Remote Desktop Connection.

Write Down Instructions, Step-By-Step

Don’t expect seniors to remember intricate processes they’ve only seen once or twice, or to intuit the workings after minimal practice.

When one of my clients (senior or otherwise) is learning new processes on the computer or another device, I teach the step and then write it down on a numbered list. Once we’re all done, I create a title with “if,” such as “If you want to listen to your new voicemails…” or “If you want to download an app from the App Store…”

Make a notebook of these lessons so your senior can flip through the pages, or even create an index in the front. (And yes, you can type these lessons and store them in Notes, Dropbox, or Evernote if that’s something your senior is comfortable navigating.) If you are at a distance, encourage them to take notes for themselves, if possible, and repeat back to you what they’ve written.

HOW TO OUTSOURCE TECH SUPPORT FOR SENIORS

Do you and your senior end up fighting when you try to help with tech? Sometimes, the best way to help is to arrange alternate help. (This is why, when adult children and their seniors spar over downsizing, bringing a professional organizer in is the best option.)

Outsource To Your Teenager(s)

Assign your teens to help their grandparents (or neighbors or friends who are grandparent-ish age).

Too few young people have the opportunity to learn from older generations, and this kind of bonding can be good for both. Seniors will feel younger when engaging with teen family members or neighbors, and the teens can connect with grown-ups with different perspectives on career, family, life, and history. (And shockingly, they’ll be more patient with Grandma than they are with you.)

AARP’s Senior Planet

Senior Planet is a free technology service sponsored by AARP, but you don’t have to be an AARP member to use it. (That said, at $16/year for anyone over 50, AARP’s discounts and educational resources definitely make it valuable.)

Senior Planet offers in-person virtual sessions, in-person classes in major cities, and online classes, like “How to Choose a New Computer.” There’s a hotline for those who need immediate assistance for simple questions. It’s available weekdays from 9 a.m. to 8 p.m. Eastern, during which Senior Planet’s “technology trainers” (employees and volunteers) can answer questions about email, texting, app notifications, video conferencing, and other tech conundrums.

Anyone needing personalized tech help can call the hotline at 888-713-3495 or fill out a form to schedule a help session.

Cyber Seniors

Cyber Seniors is a volunteer-based, non-profit organization and is available at no cost to users. Most volunteers are in their late teens and twenties and have training to serve as “digital mentors” to seniors. Think of it as digital natives guiding digital immigrants through the cyber world.

Cyber Seniors provides both one-on-one individualized support and as well as group education.

For individual needs, fill out a request form with general information(contact email, birthdate) and situation (device type, etc.), and then select an appointment date and time for a volunteer to contact you by phone. Once the mentor calls, you explain what you’re trying to do (e.g., attach a photo to an email, set up a Facetime call, change the settings in a program). Users can request a specific mentor by name or work with anyone on the CyberSeniors team, so if Grandma meshes well with a certain person, request a repeat session.

Cyber Seniors offers weekday group webinars over Zoom on tech and cybersecurity (and other) topics, and recorded prior webinars are also accessible.

GoGo Quincy

GoGoQuincy, promising “tech support for non-techies” started as a service to help seniors with but has expanded to assist anyone, no matter the age, with technology difficulties. For up to one call per month, the service is free; after that, there’s a $5/month fee plus $11 per call, so if there’s any chance you or your senior might be making more than two calls a month, the unlimited plan (for $19/month) is the way to go. (Reviewers note that experts didn’t try to upsell memberships or get callers to sign up for the paid service. Still, I’d encourage exhausting free options first.)

GoGo Quincy has a telephone hotline if you need immediate technology assistance; otherwise, schedule a session through the GoGo Quincy website.

[Editor’s note:

Hire a Technology Specialist

Your best bet for a loved one (or yourself) maybe to hire a professional technology consultant. I have senior clients who are active in their non-tech lives but for various reasons need support with their web sites, social media, or ever-more-complex devices, and having a paid consultant, either on retainer or paid per call, gives them confidence that they’re getting professional level services.

Online, you can find a variety of in-person and virtual technology coaches, like Tech Coaches or Candoo Tech.

Additionally, there are professional organizers, working both locally and virtually, who can assist with making technology more accessible. My technology-minded colleagues in the National Association of Productivity and Organizing Professionals (NAPO) can be found by going to NAPO’s website and conducting a search, as follows:

- Go to NAPO.net.

- Select “Professional Directory” from the FIND A PRO drop-down menu at the top of the screen.

- On the resulting search page (which defaults to a radius search, though you can switch to search by geographic location name), type in the requested information and select Digital Organizing from the residential organizing drop-down. The screen will refresh, giving you professionals guide you in organizing your technology.

Consider Artificial Intelligence

It’s not always ready for prime time, but there are AI options for getting tech support when humans aren’t available. One option is HelpMee.ai, which promises patient, voice-enabled conversations and screen sharing to guide seniors step-by-step through computer problems.

HelpMee.ai has multiple price points, from a free trial for 30 minutes of support, to two different levels of monthly support ($12/month for 4 hour, $20/month for 10 hours of support).

With all of these options, seniors can enjoy the benefits of technology while minimizing the frustrations. Don’t give up on helping your seniors with tech, and don’t let them give up, either!

If you have your own favorite tips and services for helping seniors with technology, please share in the comments.

Slam the Scam! Organize to Protect Against Scams

Being organized and productive depends on having systems in place. The problem is that sometimes things happen that throw all of our carefully curated systems out the window. Things like getting the flu, having your car break down (or get stolen), your computer crashing — or getting scammed.

It’s shockingly easy to fall for a scam, and frustratingly difficult to recover financially and legally after being a victim. It may require time, money, the services of specialists (like attorneys) and more. The best thing you can do is to organize yourself to protect against being victimized.

SCAMMERS PREY ON EVERYONE

You may have heard about a recent viral article in The Cut by Charlotte Cowles, the online magazine’s financial advice columnist. You wouldn’t have expected someone with that professional identity to write a column entitled, The Day I Put $50,000 in a Shoe Box and Handed It to a Stranger. But she fell for a scam, and she fell hard. And now, risking public and professional embarrassment, she has spoken out.

For weeks, there’s been debate online regarding what happened to Cowles. Many people can’t imagine that a grown woman with a professional background in financial writing could have been fooled by the ring of scammers who convinced Cowles that they were representatives of Amazon, of the Federal Trade Commission, and of the CIA.

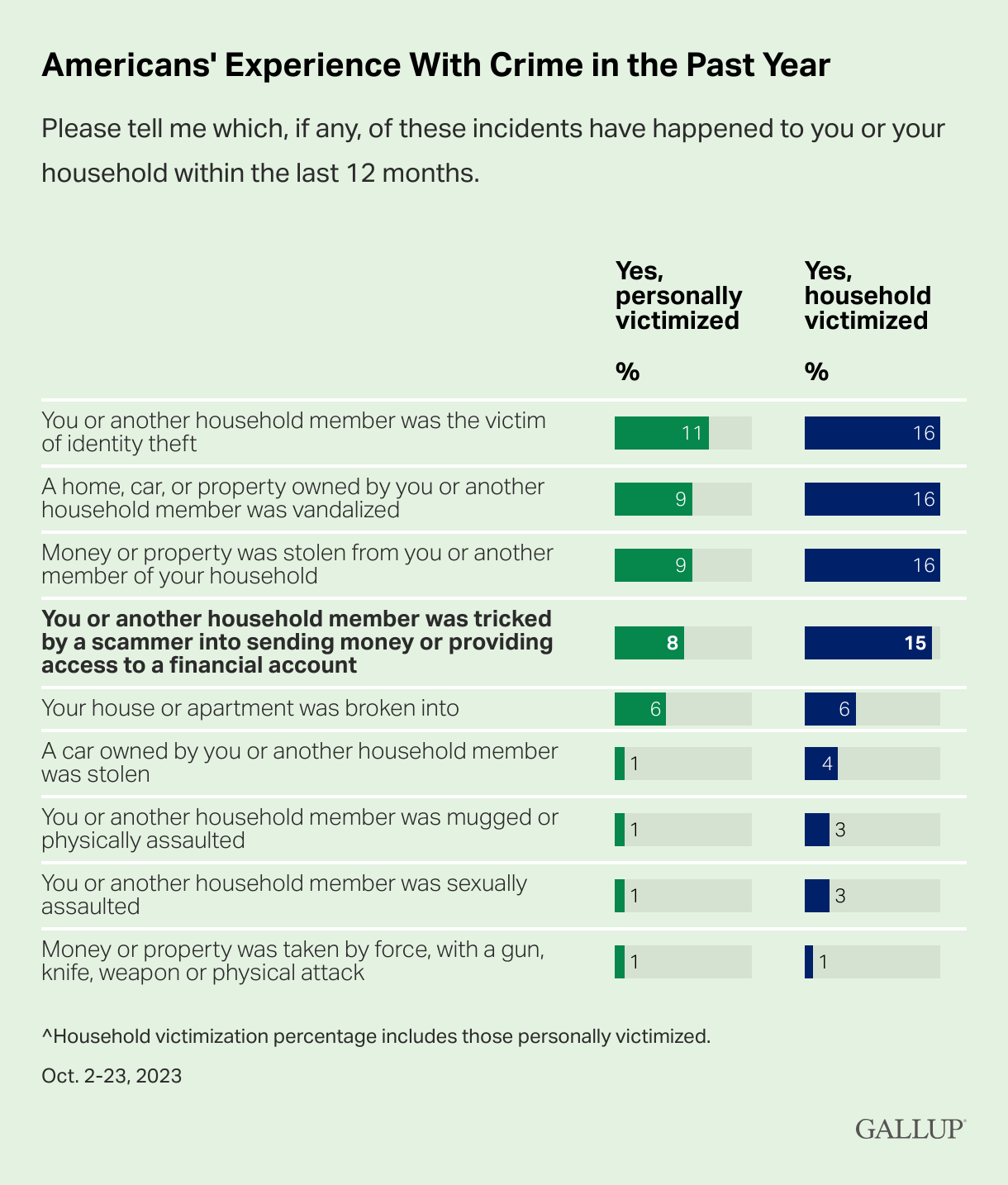

But scams are real, they are everywhere, and we need to organize ourselves (and warn our loved ones) to be vigilant. Gallup found that 15% of American households were victims of financial scams just last year.

Graph provided by Gallup

And, while we tend to think of victims as being older, every demographic group is at risk. In fact, younger adults (like Gen Z and the youngest Millennials) are overrepresented as victims of scamming (at 22%); meanwhile Gen Xers like Paper Doll and Baby Boomers are somewhat less likely to be scammed, at 9% and 14%, respectively.

The rate of victimization is lower among adults without a college education and with lower incomes than those who have college educations and who earn at least $50,000 per year. One might surmise that both of the latter groups have more opportunity to be warned and prepared to identify elements of scams.

But people with education, experience, savvy, and money can also be scammed. Last month, author Cory Doctorow wrote How I Got Scammed, explaining how a Christmas holiday travel week, a failed ATM transaction, and the post Alaska Air 737 Max door-plug disaster created a perfect storm for him being taken advantage by a phone-phishing fraudster pretending to be from his credit union.

Sometimes, a scam is obvious. Out of nowhere, you’ll be cooking or watching TV and the phone will ring. A mysterious and heavily accented speaker will say that there is “something seriously wrong with your Microsoft computer.” It doesn’t matter if you actually have a Mac, or if you don’t even have a computer. They’ll use that wearily patient voice so identifiable as IT customer support.

You immediately know it’s fake; but would your grandparents? Would your teenager?

Other scams are less obvious because they come wrapped in the kind of tech-related language we see every day. In just the 24 hours prior to writing this post, Paper Doll and Paper Mommy experience attempted scams.

I received an email claiming that I’d purchased $500+ in services, and if had not made those purchases, I should immediately click to be connected with the company’s fraud department. Of course, merely hovering my cursor over the return email address (displayed as the company’s name) showed it was actually sent by gibberishletters@Yahoo.com. Real companies don’t use Yahoo addresses; in theory, they shouldn’t even use Gmail addresses. Dependable companies have their own domains.

Meanwhile, Paper Mommy got the all-too-common email advising her to click because her iCloud was full. [Be assured, her iCloud was not full. It has a backup of her iPad and probably a few dozen photos and not much more.] Paper Mommy may be 87, but she is one smart cookie, and even if she hadn’t received one of these same phishing attempts previously, she knows enough to verify such things.

However, it’s common enough to get random notification texts, popups, and emails claiming that something is awry. One of the immediate clues is bad spelling, grammar, or punctuation, something that older generations are more likely to take seriously; a 50- or 70-year-old is more likely to immediately realize that a poor command of English (in an email sent, ostensibly, by an American company to an American customer) is a sign of a scam. Thus, given the propensity of younger people for text-speak and a lesser reliance on standard usage, younger adults might be more easily tripped up.

Still other scams prey on the inclination of individuals to be good natured. One popular scam comes in the guise of a text regarding a sick or injured dog. The sender addresses you by the wrong name and says that they’re at the vet; their dog won’t eat and is whimpering, and they’re waiting for assistance. I “fell” for such a scam a few months ago, in that I replied and said, “Sorry, you have the wrong person. I hope everything turns out OK for you and the dog.”

Sad Doggie Photo by Bruno Cervera at Pexels

I thought nothing more of it until the person kept texting and trying to inveigle me in conversation, asserting that I must be a dog lover, too. (Readers, while I’d hate for you to think I’m a Disney villainess, I’m not fond of animals in person, though I do love monkeys, puppies, kittens, and penguins, as long as they’re on my device screens and nowhere near me.)

I Googled, and immediately found that this is a long-running scam to convince text recipients to get emotionally enmeshed in the condition of the dog, and end up giving money. One can understand how Congressman George Santos managed to set up fake Go Fund Me accounts for animal care and steal the proceeds. People are softies and want to be kind.

We’re also inclined to be law-abiding. There have been a number of jury duty scams where recipients get calls or texts saying that there’s a bench warrant for them to be arrested because they have not shown up for jury duty. Sometimes, recipients are warned that deputies are on the way to arrest them unless they pay a fee over the phone, or buy gift cards and send them to the caller.

Government agencies don’t text you out of the blue. In most cases, none but teeny, hyper-local government offices will even email. They certainly don’t take payment in gift cards.

Scams are designed to prey on your lack of experience or information, your good nature, and your fear of getting in trouble (as with Cowles’ example). Do not let scammers waste your time, ruin your productivity, or take advantage of your goodwill.

SOCIAL SECURITY: SLAM THE SCAM DAY

The Social Security Administration has declared this Thursday, March 7, 2024 Slam the Scam Day!

On National Slam the Scam Day and throughout the year, the SSA provides tools to help seniors and others recognize scams related to Social Security and prevent scammers from stealing both funds and personal information.

Social Security and Paper Doll want you to protect yourself, your loved ones, and people in your community this Slam the Scam Day by educating everyone about government imposter scams. Discuss the issue and let people in your life know they shouldn’t be embarrassed to report if they shared personal information or suffered a financial loss. It’s important to report scams as quickly as possible, both to aid recovery and identify the culprits.

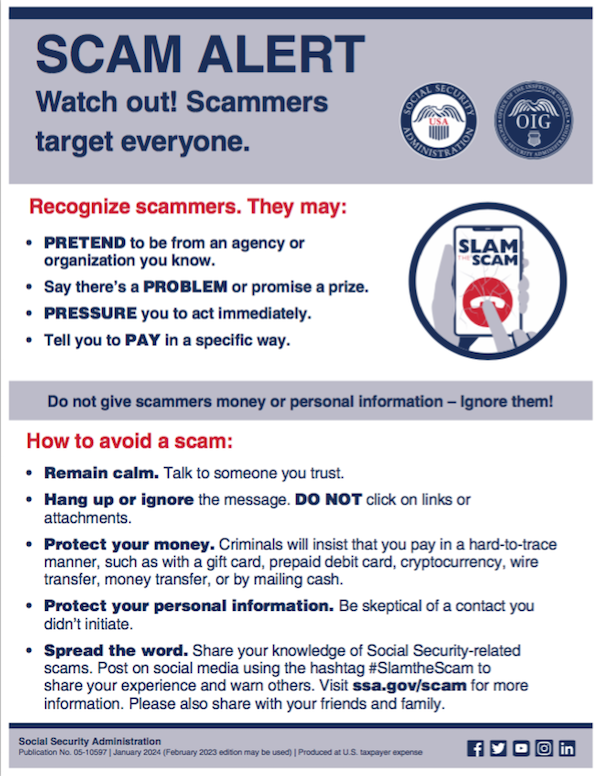

The Social Security Administration encourages us to share their Scam Alert fact sheet to help educate others about how to protect themselves. Report Social Security-related scams to the Social Security Office of the Inspector General (OIG).

If you do encounter scammers in any way related to Social Security, report the scam online with as much information as you have regarding the characteristics of their claims.

Social Security encourages you to visit www.ssa.gov/scam for more information and follow the SSA OIG accounts on Facebook, Twitter, and LinkedIn. Those accounts aren’t going to share the newest viral dances or memes, but will keep you informed of the latest nasty tactics. Please consider sharing this post with the #SlamtheScam hashtag on your social media platforms.

OTHER SCAMS TARGETING SENIORS

Scams targeting seniors aren’t limited to those involving Social Security.

The “Grandma, I’m in Jail!” scam has been prevalent for more than a decade. Your phone rings and you hear a young person’s distraught voice begging for help. The caller, ostensibly your grandchild, has somehow accidentally run afoul of the law and is in jail. “Please send bail money but don’t tell Mom and Dad,” the caller begs, providing a phone number and case number; you call as directed and the faux police officer verifies the case number and takes your money. These scams assume Grandma doesn’t hear your voice often enough to recognize it on the phone.

Help your grandparents not fall for such scams by 1) explaining how they work and 2) calling them more often so that they recognize your voice!

Photo by RepentAndSeekChristJesus on Unsplash

Elders are often the victims of medical scams designed to impersonate legitimate agencies related to Medicare, diabetes supplies, medical equipment, hospice, and more. Romance scams, which prey on lonely people of all ages, but especially tender-hearted seniors, are also on the rise.

The American Association of Retired Persons (AARP) is great resource for keeping on top of scams targeting the elderly. Bookmark AARP’s Scams and Fraud page to learn about new schemes as they become known.

KNOW THE SCAMMERS’ TRICKS

Similar to “Grandma, I’m in Jail” is “Dad, I’ve had a car accident!” There’s loud traffic noise (and perhaps sirens) in the background and the faux-distraught caller is saying that they’ve caused an accident and that the police say they need to pay a fine right away. Don’t fall for it.

Remember how I said that government agencies won’t ask for payment in gift cards? Neither will your boss. The Do Me a Favor scam shows up via email or text, when your boss (or maybe the CEO of your company) sends a message asking you to purchase gift cards for a work-related charity promotion, promising to pay you back after he receives them.

Yeah, no. The email or text may look like it’s coming from your work contact, your church leader, or your Facebook friend, but it’s almost certainly not.

Similarly, your friends aren’t going to be at the Paris Olympics and lose their wallets and ask you to send them money via Facebook.

The best way to organize yourself against scams is to stay informed of what scams are popular. When you know what to expect, it’s easier to identify scammers and avoid engaging.

- 5 Financial Scams To Avoid in 2024 as Expert Warns Fraud Has Reached ‘Crisis Level’ (NASDAQ)

- 6 Top Scams to Watch Out for in 2024 (AARP)

- 10 Scams You Should Know About in 2024 (Express VPN)

- 17 Facebook Marketplace scams to avoid in 2024 (Lifelock)

- Credit Card Scams to Know in 2024 (and How to Avoid Them) (Time Magazine)

- Five Biggest Frauds To Watch Out for in 2024 (Kiplinger)

- The Latest Scams You Need to Be Aware of in 2024 (Experian)

- No Love for Romance Scammers in 2024 (IRS)

DON’Ts AND DOs TO KEEP YOURSELF SAFE FROM SCAMMERS

DON’T CLICK — If you receive an email or text with links to your bank or other financial account, go instead to the official website and log in from there. If you don’t know the URL, look it up on the back of your bank or credit card or on your statements. And, as you’ve been told since the dawn of email, do not click on attachments from somebody you don’t know.

DON’T TRUST — The Caller ID may say that the inbound call is coming from your bank or the IRS, but it’s ridiculously easy to “spoof” (that is, fake) the identity of a caller. Consider not answering; scammers rarely leave voicemail.

Don’t assume that the caller having the last four digits of your Social Security number or even all of the digits of your account number is on the up-and-up; there’s just too much of our private information on the dark web. Instead, hang up and call the official number for your financial institution and request to be connected to the fraud department.

DON’T DIVULGE — If a stranger claiming to be from your bank or credit card’s fraud department contacts you, ask for a case number. Do not give out your personal information. Do not give out your PIN.

DON’T SAY YES — Do not answer questions in the affirmative. That is, if they ask, “Is this Jane Smith?” don’t say yes; if you must say something, reply, “What is this regarding?” Your voice could be recorded and cloned for AI-related scams. The less you say, the better.

DON’T RUSH (OR BE RUSHED) — It’s the nature of scammers, like the stereotypical used car salesman, to use the pressure of time to get you act against your best interest. Don’t be fooled into making a decision or taking action quickly. Check with advisors, whether more technologically savvy friends or relatives, your accountant or financial advisor, your attorney, or the police.

DO READ UP — The American Bankers Association has a nifty website called BankersNeverAskThat.com. The site explains what to watch out for in terms of email, text, phone, and payment app scams, and also has a great eight-question quiz where you can walk through the situations (on your own, or as part of coaching with a loved one) to identify whether something is a scam or legitimate.

For reference, I did pretty well, but I dithered on the question regarding payment app alerts; if you’ve only recently begun using apps like Zelle, Venmo, or other peer-to-peer payment services, you might find the example sneaky, too, so read (and share) AARP’s How to Avoid Scams on Zelle, Venmo and Other P2P Apps.

The site offers a goofy “retro” scam-themed video game and a series of lighthearted videos to drive the point home.

>

DO HAVE FAMILY PASSWORDS — Schools have security that was non-existent when I was a kid; there are lists of who is allowed to pick up little Johnny or Janey from school to ensure not only that there’s no Stranger Danger but that wackadoodle exes and pushy in-laws don’t insert themselves between you and your kids. Modern parenting includes having family passwords so that if someone says, “Hi, your mommy told me to come pick you up from soccer practice today,” even if the child recognizes Mommy’s best friend as Auntie Karen, the kids know to wait for the official password.

This concept should be applied to families at all ages. Have a communication password designed so that if Grandma or Dad or College Kid gets a call purporting to be from one of the others and is in in need of emergency funds, there’s a level of security involved. (But, y’know, if Grandma calls from jail too often, maybe let her think about the consequences of her actions for a little while.)

DO TELL THE AUTHORITIES — No matter how embarrassing it is to have been scammed, it’s important to report suspected and actual scams.

- Notify your bank, credit card company, brokerage, or other financial institution immediately. If scammers have actually taken your money via credit card, the company should be able to flag the transaction as fraud and reverse it immediately; other financial institutions may also be able to freeze the transaction and save your money. Take screenshots of texts or emails, and don’t delete the original messages in case law enforcement wants to dig more deeply into the source code.

- Contact the police, and file a police report. Do not be dissuaded if the police officer seems blasé about the crime.

My credit card company once notified me that someone had used my card number to buy an inordinate amount of mail order men’s underwear and stereo equipment. Algorithms had already flagged the purchases as fraud, but they asked me to file a police report. The police officer who took the report at my workplace could not have looked more bored if I’d asked him to watch paint dry. It doesn’t matter. Report!

- File reports with applicable state and federal agencies. Whether the case involves the Social Security Administration, Medicare, or other federal crimes, report scams to the applicable agencies. The Federal Bureau of Investigation (FBI) and the Federal Trade Commission (FTC), as well as your state’s bureau of investigation all have fraud departments. Learn more at the FTC’s Reportfraud.ftc.gov and the FBI’s Internet Crime Complaint Center at IC3.gov.

THE FUTURE OF SCAMS

Scams — and scammers — aren’t going away. There will always be scammers who take advantage of anyone more easily duped because they have less information, less experience, and fewer people watching out for them. But, as I alluded to earlier, there are higher tech scams on the horizon.

Artificial intelligence is scary. I bet you’ve heard about deepfakes, video imitations made to sound and look like a real person is saying something they never actually said.

Voiceprints and voice cloning constitute the audio version of deepfakes. A scammer can record you — or take your teenager’s Instagram or TikTok video — and create a completely new message using words and expressions that were never actually said, and then create an “emergency” where it’s believable that money or your Social Security number or other private information is requested. If your college-age kid still hasn’t memorized his Social Security number, you might be tempted to believe it if “he” calls from a spoofed number that looked like his and says he’s filling out a form at school and needed his (or your) digits.

Voice cloning is already being used. Scammy deepfake videos could just as easily be to sent via Facetime or text video. Be careful.

FUNNY THINGS (NOT) TO DO TO SCAMMERS

You shouldn’t engage with scammers, so don’t emulate Paper Mommy or her friend in the stories below. Still, it’s fun to imagine retribution against bad guys.

When I was a teen, my mother was visiting a friend, a suburban woman of (shall we say) means. A phone scammer interrupted their visit and was urgently pushing some sort of financial scheme. Mom’s friend told the caller that she was sorry, but he’d have to wait, that her husband busy shoveling the cow s***.

Later, my mother spoke of her friend’s response with a twinkle in her eye.

Paper Mommy, as longtime readers know, is a hoot. After a friend briefly fell prey to the “Grandma, I’m in jail!” scam (until she learned that her teen grandson was fast asleep in his own bed), Paper Mommy began plotting her revenge on scammers. A few years ago, she called me with delight to report that the day she’d been anticipating had finally arrived.

“Grandma, I need your help!” the voice implored. The scammer had already made a tactical error; much to Paper Mommy‘s chagrin, neither my sister nor I have made her a grandmother. My mom tut-tutted as the scammer wove his tale, offering periodic, “Oh, no, darling! … Oh, you poor thing? … You need me to send you money?”

She kept him on the line for eons, repeatedly leading the evil-doer to believe she was prepared to turn over her credit card number to secure grandson’s release. Oh, she just had to find her purse. Oh, fiddlesticks, where was her wallet? Just when his frustration led him to almost crack and he implored, “Grandma, aren’t you going to help me?” my mom uttered her Oscar-worthy line:

“No, Sweetheart. I never really liked you that much.” Click.

#SlamTheScam

A New VIP: A Form You Didn’t Know You Needed

Brown Plush Bear Patient Photo by Kristine Wook on Unsplash

As a professional organizer for 20 years, I am rarely stumped by organizing-related questions, especially those having to do with vital documents or what I call VIPs (very important papers). However, a client recently presented me with an article making a recommendation for a particular document, and it sent me down a rabbit hole of research.

THE USUAL SUSPECTS: VIPS AND HOW TO MAINTAIN THEM

Over the past years, we’ve discussed (at length) the essential documents everyone should have and how to organize and keep them safe. Posts covering these topics have included:

How to Create, Organize, and Safeguard 5 Essential Legal and Estate Documents

The Professor and Mary Ann: 8 Other Essential Documents You Need To Create

Ask Paper Doll: Do I Really Need A Safe Deposit Box?

Paper Doll’s Ultimate Guide to Getting a Document Notarized

Over the years, we’ve looked at documents granted by a government entity, like birth and marriage certificates, divorce decrees and custody documents, citizenship and military separation papers, passports, and Social Security cards.

We’ve also reviewed essential documents you must create for yourself (or with assistance), including home inventories, insurance policies, estate planning documents (like wills and trusts, pre- and post-nuptial agreements), and living wills (also known as advanced medical directives).

And, for ensuring that your loved ones can take care of you (and you can take care of them) in the event of incapacitation, we have always accented the importance of having both a Durable Power of Attorney for finances and Durable Power of Attorney for healthcare (known in some states as a healthcare proxy).

BEHOLD: THE POWER OF ATTORNEY

A Durable Power of Attorney for financial decisions is necessary if you are unable to make financial decisions or take financial actions on your own. This might occur if you are ill and lack the cognitive capacity to make your own decisions (such as if you’re comatose, heavily medicated, or experiencing some sort of dementia), but it might also come in handy in other circumstances.

Imagine that you are taking an around-the-world cruise or hiking in the Himalayas. In such cases, communication may be spotty or impossible. If the stock market were tanking or a financial opportunity of great importance occurred, or if your return were delayed and you needed to make sure your child’s college tuition was paid or some other financial arrangement was secured, knowing that someone with your Power of Attorney for financial concerns was handling everything would certainly put your mind at ease.

A Durable Power of Attorney for healthcare, or a healthcare proxy, is similarly important if you are unable to make your own healthcare decisions, pretty much for the same reasons initially outlined. If you are physically or cognitively incapacitated and need someone to make decisions on your care, it’s essential to have that paperwork in place.

And, as a periodic reminder to all parents who’ve recently sent their kids off to college, without a Power of Attorney for healthcare or healthcare proxy in place, if your away-at-school adult child were ill and had not granted you PoA for healthcare, the college’s health center or local hospital would not be allowed to provide you with any information about your child’s condition or care.

So, Power of Attorney documents are pretty darned important. You want them in place so that your spouse, partner, adult child, or trusted friend or advisor can be kept informed of your situation and can, if necessary, make decisions and take actions on your behalf.

This is the be-all and end-all of advice we paper specialists generally need to give. But guess what? We’ve been missing a pretty important document related to older adults!

BEYOND THE POA: THE DOCUMENT YOU DIDN’T KNOW YOU NEEDED

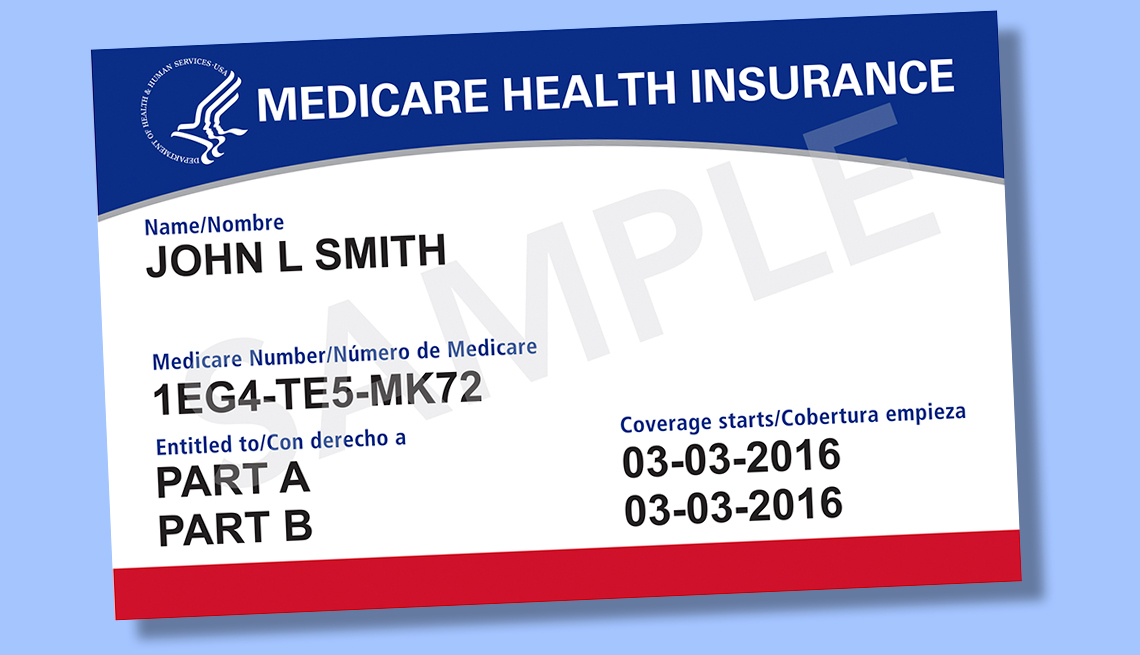

Let’s imagine your spouse is 65 or older. Or perhaps we’re talking about your parent, or another slightly older loved one. (I say slightly older, as now that Paper Doll has reached 55, the age of 65, when you can get Medicare coverage, doesn’t seem that far off.) Or perhaps you’re the one with Medicare.

You’d assume that as long as Powers of Attorney had been executed with regard to financial and medical decisions, then everything would be A-OK. Right?

Mostly. But not entirely.

It turns out that, by law, if you want someone (your spouse or significant other, your adult child, your caregiver, etc.) to speak to Medicare on your behalf, having a both a Durable Power of Attorney for financial issues and one for medical issues is not enough.

Perhaps because each state has a different variation on PoA forms, or perhaps because the government just likes to be wackadoodle, Medicare requires you grant prior authorization via a surprisingly under-mentioned form called the 1-800-MEDICARE Authorization to Disclose Personal Health Information Form or CMS-10106. (Doesn’t that just roll trippingly off the tongue?)

You must fill out the CMS-10106 well in advance if you want someone to potentially be able to discuss any of the following with Medicare:

- Medicare eligibility

- Medicare claims

- Plan enrollment (including part D or other drug plans)

- Payment of premiums

- Other information, including payments to beneficiaries

So, if you have Medicare, are you thinking “Whoops!” and wondering what happens if you have secured your financial and healthcare PoAs but haven’t ever filled out this authorization?

It turns out there’s a quirky loophole. If a person HAS done both of their PoA forms but hasn’t actually filled out this authorization form, it’s entirely not a catastrophe. That’s because the person who fills out the form has to be either one of the following:

- the beneficiary (that is, the person on Medicare)

OR

- the personal representative of the person on Medicare (that is, the person who has the Powers of Attorney, or otherwise has been granted authorization over your information).

So, yes, if you’re the person with the Power of Attorney for a Medicare beneficiary, you can authorize yourself to let Medicare talk to you about someone’s health and payment information. And if that seems a little weird to you, well, you’re not the only one.

The problem is that if someone hasn’t ever filled out the CMS-10106 in advance and their personal representative has to do it, it’ll take time to process because you have to MAIL it to Medicare.

That’s right — you can’t submit the authorization form online or even by fax. You have to mail it, like it’s 20th century, to a post office box in Lawrence, Kansas!

So, that’s why I’m writing this post, so that if you or someone you know is enrolled in Medicare, you (or they) can jump right on this.

WHAT TO KNOW ABOUT THE CMS-10106

The first thing to know about the long-windedly named 1-800-MEDICARE Authorization to Disclose Personal Health Information Form (CMS-10106) is that it’s a fillable PDF.

For those unfamiliar, that’s a digital form that allows you to type the information right into the blank fields on the screen so that when it’s printed, the information you typed is blended with the form provided, as if you were using a typewriter and typing right on the paper. One supposes that Medicare doesn’t want people to print and fill the blank documents by hand to prevent confusion caused by messy handwriting.

![]()

Open the CMS-10106 instructions and form on a computer. (While I have not tested all browser options, the fillable PDF function does not work on my iPhone or iPad.)

The form has only six questions (with a few sub-sections) and they are pretty self-explanatory.

Q1: First, fill in the name, Medicare number, and birthday of the person who is a Medicare beneficiary. That’s either you, or if you’re the person with Power of Attorney for a person with Medicare, you’ll put their information. (You’ll get to identify yourself as the Medicare beneficiary’s personal representative later on in the form.)

Q2: Next, you get to choose whether you’re allowing all information to be disclosed, or only a limited amount.

You can specify whether Medicare can disclose information related to any or all of the categories mentioned: eligibility, claims, plan enrollment, payment of premiums, and/or other information, including payments to beneficiaries.

(There is a special sub-question just for New York residents, allowing them to grant or withhold authorization to discuss alcohol and drug abuse, mental health treatment, and HIV status. If you are not a New York State resident, you will skip this question.)

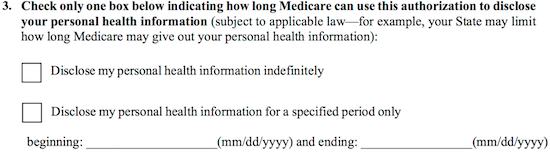

Q3: At this point, you get to decide whether you want authorize Medicare to disclose your personal information indefinitely, or only for a limited period of time (and you would provide a start and end date).

In most cases, you would grant authorization indefinitely to your spouse, adult child, or loved one. However, if you’re a singleton and asking a good friend (but perhaps not your BFF) to help you with these things, you might want to date-limit authorization. (Also, as you’ll see below, you may have reasons to grant authorization for a limited period to representatives of an agency or organization.)

Note: even if you grant indefinite authorization, your state may have separate regulations regarding how long authorization stands. Yes, that lack of uniformity between states and a federal agency is another example of how wackadoodle red tape can be.

Q4: The fourth question could prove a little confusing, so Medicare offers a twinge of help. The question reads, “Fill in the reason for the disclosure (you may write “at my request”):”

It’s good that they’ve added that parenthetical option, because most people would end up filling the two blank lines with some variation on, “Because I’m having this yucky surgery and my brain is going to be floopy for a while and I’ll be in the hospital and then in a rehab facility without good cell service, I want my cousin Bernice to be able to talk to Medicare for me.” And that won’t really help anyone. Just write, “at my request” and be done with it.

Q5: The fifth question gives you the opportunity to name two people (and provide their addresses) to whom Medicare can disclose your personal information. If you have named primary and secondary “agents” as your Powers of Attorney, these would be the people you’d most likely list here. (You can add more names on a separate sheet of paper.)

Note: Medicare allows you to list organizations instead of, or in addition to, individual persons; for example, if you’ve hired a professional financial organizer, daily money manager, geriatric care manager, or elder attorney, you might want to list the company/service so that assigned team members can provide assistance.

Another reason you might want to list a particular organization is if you’ve been injured in an accident. Let’s say you need to make a personal injury claim because your neighbor’s giant skeleton display for Halloween falls on you.

If you are making a claim, you have to prove that you sustained injuries, and your medical records (including Medicare records) may be required to support your claim and get your neighbor’s insurance to pay. Authorizing Medicare to talk to your neighbor’s insurance company may help speed things along.

Q6: The final question is formatted a little differently. First, there’s the official authorization statement:

“I authorize 1-800-MEDICARE to disclose my personal health information listed above to the person(s) or organization(s) I have named on this form. I understand that my personal health information may be re-disclosed by the person(s) or organization(s) and may no longer be protected by law.”

Underneath, there are fields for a signature (the only field you will leave blank until after you print the document), phone number, and date you’re filling out the form. Then there’s a box to list the complete address of the person with Medicare (that is, the beneficiary).

Note: if you’re not the beneficiary (rather, you’re the one helping the person with Medicare), you’ll check the box that says, “Check here if you are signing as a personal representative and complete below. Please attach the appropriate documentation (for example, Power of Attorney).”

Then you’ll provide your own address, telephone number, and your relationship to the beneficiary, and you’ll attach a copy of the Power of Attorney documents to prove you are authorized to be a personal representative. (Again, you’re authorizing yourself to authorize yourself to talk to Medicare. Yes, it’s weird.)

Remember, the person with Medicare is the beneficiary; the person helping the beneficiary is the personal representative!

Once you complete the entire form, there’s a grey PRINT FORM button at the bottom. Click it, and then sign on the signature line for question #6. Remember, I said the fillable PDF wouldn’t let you type anything there? That’s because, of course, you have to hand-sign the document. You can’t use Adobe or Apple Preview’s digital signature feature because the form won’t let you click there.

Make a copy of the CMS-10106 for your own records and mail the signed, blended form to:

Medicare CCO, Written Authorization Dept.

PO Box 1270

Lawrence, KS 66044

WHAT IF I CHANGE MY MIND?

At any time, even if you’ve granted indefinite authorization or the ending date of the limited authorization has not yet occurred, you can revoke your authorization.

This doesn’t have to seem like a mean thing. I mean, sure, you could be in a huge fight with your Cousin Bernice because she said the potato salad you brought to the last family reunion wasn’t as good as hers, and you’ve decided you don’t want her to be authorized to talk to Medicare on your behalf.