Ten 10-Minute Financial Tasks to Organize Your Finances

[Editor’s note 4/27/2020: As we all cope with another month sheltering in place, financial issues are causing anxiety. Even if you’re not feeling highly motivated (or motivated at all), this classic Paper Doll post is filled with quick tasks to help you get a handle on your financial situation and feel more empowered.]

Readers, at three weeks into the new year, most people have petered out in their attempts to achieve their resolutions, or they’ve not even started, waiting until after they’ve taken down the tree or gotten the kids back to school. But the clock is ticking, and time is money. And while love of money may be the root of all evil, money itself is what keeps us from living in a van down by the river.

So today, Paper Doll is offering up a fast-forward kick-in-the-tush for organizing those little green pieces of paper we all like so much.

To that end: take ten minutes a day, for the last ten days of January, to take ten tiny steps toward getting your finances in order.

1) Sign up for your online Social Security account.

IRA. 401(k). 403(b). No matter how you’re saving for your retirement, there’s one program in which you’re pretty much guaranteed to be participating (unless you work for the railroads): Social Security. If your senior years are dependent upon your retirement savings, investments and benefits, wouldn’t it make sense to ensure the information is organized?

A few years ago, in Social Security Goes Paperless & Gets Lean, Green & A Little Mean, I told you about how the paper Social Security statements we’d been receiving annually were being discontinued.

A year later, I announced the new SocialSecurity.gov online account program in Paper Doll Makes a Statement: The Social (Security) Network.

But did you sign up?

If you haven’t yet signed up yet, now’s the time to do it. Go to the my Social Security website (let’s just ignore their e.e. cummings-esque decision not to capitalize “my”), and click on Create An Account to get started. Once you create your account, you’ll be able to track your earnings and verify that they’ve been properly reported (by you and/or your employer), and get estimates of your future benefits. If you’re already receiving benefits, accessing your account enables you to obtain a letter with proof of benefits (often needed for legal and financial purposes), change your address and direct deposit payment information, and manage your benefits.

If you have already set up your account, change your password. Now! The Social Security Administration actually makes you do what you’re already supposed to do — update your password every six months. If you haven’t, it’ll prompt you to do so when you log in. (Speaking of passwords, just this week, SplashData released a list of the worst passwords of 2014. Don’t use those. C’mon.)

2) Take your Social Security card out of your wallet.

Seriously, dude. We’ve talked about this (in What’s In Your Wallet (That Shouldn’t Be)?). Your Social Security Card, in the wrong hands, is an invitation to identity theft and financial fraud. Memorize your number for when you have to unexpectedly fill in forms. (Really, it’s like a phone number, just nine digits.) Put the actual card in your VIP (very important paper) file system or in your fireproof safe, and only pull it out when you need it.

Seriously, dude. We’ve talked about this (in What’s In Your Wallet (That Shouldn’t Be)?). Your Social Security Card, in the wrong hands, is an invitation to identity theft and financial fraud. Memorize your number for when you have to unexpectedly fill in forms. (Really, it’s like a phone number, just nine digits.) Put the actual card in your VIP (very important paper) file system or in your fireproof safe, and only pull it out when you need it.

Can’t find your Social Security Card? Report it, especially if you think you’ve been the victim of identity theft, and then replace it.

3) Pull your credit report annually.

Yup, we’ve talked about this, too. Over and over and over. The only way to make sure that creditors have properly reported your financial activities, and to ensure that you’re protected against bad guys securing credit in your name, is to check your credit history.

To that end, the federal government mandated the creation of a free joint program among the credit reporting agencies (Experian, Equifax and TransUnion) at AnnualCreditReport.com. Click, answer enough identifying questions about past addresses and financial history to convincingly prove that you are who you say you are, and print (or make a PDF of) your credit report.

And then here’s the thing: read it. Downloading your credit report and not looking at it is like buying exercise videos and not taking the shrink-wrap off the DVDs. It creates clutter in your space, maintains clutter in your life (messy finances, like lumpy physiques), and keeps your future (financial) health insecure. Downloading your credit report and not looking at it is like buying exercise videos and not taking the shrink-wrap off the DVDs.

Remember, your credit report doesn’t automatically include your credit score. You generally have to pay each of the three credit reporting agencies extra for that. But that doesn’t mean you have to pay — DiscoverCard and other credit card companies have started to provide FICO scores (for more on that, check our classic Paper For Your Plastic: Organizing a Better FICO Score) and CreditKarma, a company enabling you to track your credit score over time, is a non-icky consumer option.

4) Look back at 2014.

Did you get married? Divorced? Have a baby? Adopt? Did your own little company shoot through the roof? You’ll be doing lots of paperwork soon to work on your taxes for last year, but don’t forget about setting things up for the coming year.

If you’re employed by someone else, you may be subject to more or fewer withholding exemptions. Sit down with your HR department to figure out how to change your withholdings on your W-4.

If you pay self-employment taxes, be sure to adjust your quarterly estimated taxes accordingly.

5) Balance your portfolio (and not on the top of your head).

The best way to organize your future finances is to be an active participant and know what you’re invested in, in what proportions, and keep tabs as the economy changes the balance of your holdings. Paper Doll isn’t a financial consultant. I read Money and Kiplinger’s and watch the quarterly statements on my investments, and I don’t have a clue about the math on my own.

Sit down with your financial advisor, if you have one, or find a fee-only financial planner through the National Association of Personal Financial Advisors (NAPFA), and find out where your money is: in what companies or mutual funds, in what types of accounts (growth, income, real estate, magic beans, etc.), in what proportions, and create a plan for getting your financial future organized.

6) Create, or add to, your emergency fund.

Experts used to say to keep three-to-six months’ worth of expenses in a liquid emergency fund. (And no, as much as Paper Doll believes diet Coke should be legal tender, this means your money is immediately accessible.) During the recent volatile economic years, that’s been upgraded to eight months.

Not even close? Keep reading for baby steps to help you get there.

7) Create a spending plan.

The word “budget” is about as appealing as the word “diet” — and about as effective. Instead, take a few minutes as your mail comes in each day to jot down what you pay each month, or use a financial dashboard like Mint to track all of your spending and income. Review expenses, including:

- Rent or Mortgage

- Insurance (health, homeowners/renters, auto, etc.)

- Utilities (electricity, gas, cable, internet, land line, cell phone, data plans)

- Child-related (baby sitters, tutors, music lessons, activity fees)

- Home-related (homeowners’ association dues, cleaners, lawn care, exterminators)

- Credit card bills

- Student loan payments

- Other debts (car loans, personal loans, etc.)

- Controllable expenses (groceries, dining out, clothing, personal purchases)

Show up for mail call. Avoiding the truth about your financial situation is like not going to the doctor because you’re afraid of the diagnosis. The sooner you know what’s going on, the quicker things can start improving.

Know your income and your monthly expenses. If the latter seems to outstrip the former, prioritize what can be cut (even temporarily). Knowledge is power.

8) Automate savings. Don’t play games.

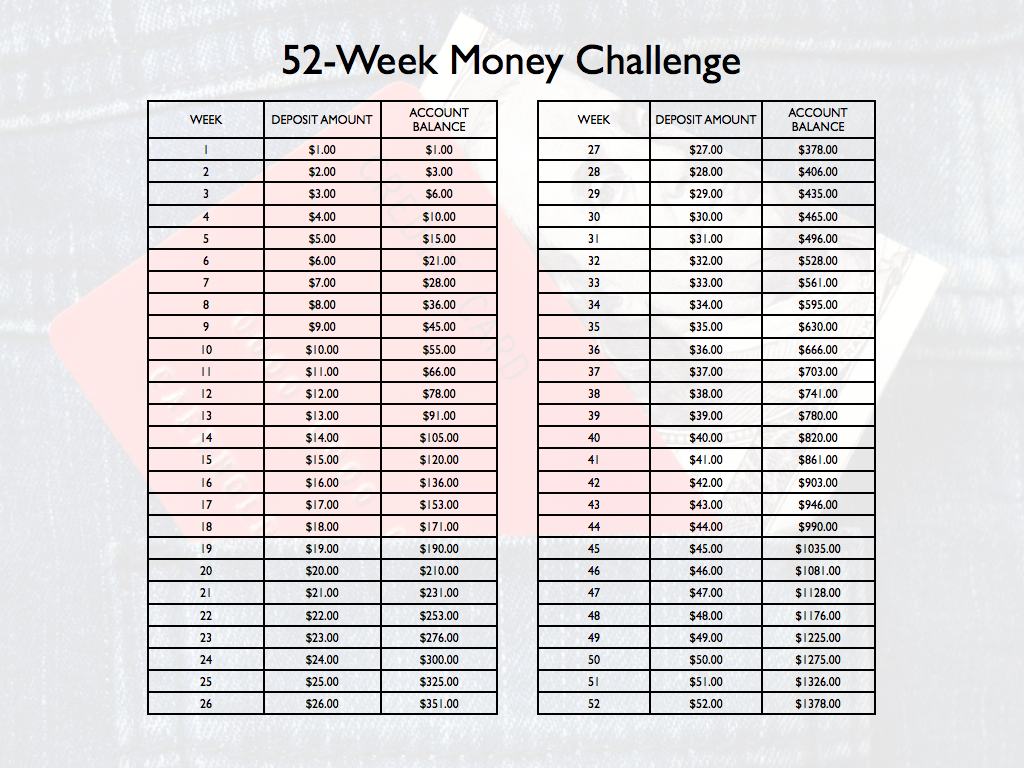

Have you heard about the 52 Week Savings Challenge? This got big exposure in 2014 and has been making the rounds again. I’d love to credit the graphic below, but it’s simply been EVERYWHERE for the past year-plus, and nobody’s taken credit.

The theory was that each week of the year, you bank one dollar more than the week prior. What’s a dollar? What’s a couple bucks? Keep it up and after 52 weeks, you’ll amass close $1400 (plus interest), almost painlessly. Conceptually, it’s appealing, but I’ve got worries.

The theory was that each week of the year, you bank one dollar more than the week prior. What’s a dollar? What’s a couple bucks? Keep it up and after 52 weeks, you’ll amass close $1400 (plus interest), almost painlessly. Conceptually, it’s appealing, but I’ve got worries.

Let’s start with the plan as written. Sure, $3 is no biggie for most of us. But as you go along and head toward the end of the year, it might be hard to find a loose $47 or $50 every week. From Thanksgiving to the end of the year, alone, that’s $296, and for people who are struggling, that’s a toughie. (For those who increase each week’s savings by $10 instead of $1, the end of the year would be similarly problematic.)

One solution might be to move backward or mix it up. Start at $52 at the start of January, decreasing the amounts each month. Or number scraps of paper 1-52, put them in a jar and pick one out each week to transfer to savings.

A larger problem with the system is that it’s hard to automate transfers with an incremental increase. You probably can’t tell your bank to take $X+1 and transfer that each week. But you know that it’s easier to do something when you don’t need to find motivation to accomplish it.

I think it makes more sense to automate your savings. How much do you want to save this year? Divide by 52, and whether you’re putting away $5 or $500 (lucky you!), set up an automatic transfer through your bank, or consider seeing if your employer will split your direct deposit between two accounts.

9) Identify to what’s expiring when, and what it’ll cost you.

If you’ve completed task #7, you’ve got a handle on regular expenses, but what payments do you make annually, or upon expiration? Don’t be surprised — review last year’s credit card and bank statements and think about past financial annoyances. For example:

- Amazon Prime — Did you get in on the low rate last year before it bumped up?

- Annually renewed gift subscriptions — Do you regularly bestow largesse?

- Discounted services — Did you get a discounted 12-month package from your cable company? Is your low-rate cell contract up?

- Professional expenses — Do you need to renew dues or pay for certifications or licenses?

- Travel costs — Do you need to renew your passport, Global Entry or Trusted Traveler programs, or airport lounge memberships?

10) Don’t guess. Know.

Being organized doesn’t just mean sorting the paperwork or the emails that come every month. It means knowing what you have and where you have it, keeping what works and getting rid of what doesn’t suit your goals.

- Write down everything you spend. (If you never use cash, a financial dashboard may suffice, but you’ll pay more attention to those little drips and drops of funds if you put pen to paper.)

- Balance your checkbook register, even if you haven’t written actual checks in eons.

- Check receipts against your online bank and credit card statements.

- Scan your credit card statements as soon as they arrive, and call to verify anything that looks hinky.

It’s your money, honey. Your finances are like children. Keep them safe, help them grow, and they’ll make sure you have a happy old age.

Great post Julie! I love that these ten minute tasks get us more in touch with our money and the important documents needed. Thanks!

Lots of valuable info here! Even though some of your resources are strictly for Americans, the principles apply everywhere. Now we know what we need to know!

I think creating a spending plan is the most important task. Having a plan goes a long way in focusing on how to move forward, not just reacting to what happens.

I have found that cash is when I lose track of what I’m spending on. I avoid using it as much as possible, because I track everything I charge in Quicken. It is good to be honest about where you are spending your money. In my case, it is mostly on taxes – argh.

I avoid cash except when I’m traveling; I find it’s hard to track, even if you keep the receipts for everything, and you end up getting weighed down by loose change!

Facing financial issues can be similar to facing health ones. We tend to ignore them for fear of discovering something unpleasant. But of course, postponing is not good to do. I love how you share doable (relatively painless) ways of getting more control over your finances.

One of the best steps my husband and I took was to automate weekly deposits into our 401K and SEP-IRA accounts. Each year we evaluate the amount being set aside and decide if we can increase it. Even a little bit more makes a difference. It was my husband that started doing this first, and he inspired me to do the same.

I love this, Linda. And once you set it up, you don’t have to think about it — which means you aren’t inclined, on a month-by-month basis, to wonder if you should spend the money elsewhere. Very smart!