How to Organize Yourself for a Stress-Free Tax Season

Nobody likes paying taxes, but if you’re organized, the discomfort can be limited to the money leaving your bank account and not all the work leading up to it. Preparing your tax returns (or getting the information to your tax preparer) doesn’t have to be annoying. To that end, every few years, I try to provide a Paper Doll primer on what you need to know and understand to make tax time bearable. This year, it has bonus pop culture to keep you entertained!

SET THE STAGE FOR PAYING THE TAX MAN

Photo by The New York Public Library on Unsplash

Tax prep is the homework of the adult world, but that doesn’t mean it can’t be easier (or more fun) than finding the area under a curve or remembering what cosin and tangent are.

Start by creating a comfortable work environment. Clear your desk of clutter and distractions. If that’s not possible (in the amount of time you have), consider moving to a new workspace just for doing your taxes. That might be the dining room table, the guest bedroom, or the conference room at work on a Saturday afternoon.

The key elements are ample workspace, a place to put (and if necessary, plug in) your computer, functional Wi-Fi, a pad of paper for taking notes, access to good lighting and a comfortable chair, and your tax prep documents (of which, more later).

More importantly, do what you can to eliminate interruptions, whether that means working when others are out of the house (or getting out of the house to do your work).

Create the right ambiance for your style. Some people need a window facing sunlight, while I prefer to have my chair face a blank wall to eliminate distractions. Some people need silence, while others prefer white noise. If you used to do your 9th grade math homework with your stereo blasting, try making a tax prep playlist using Hubpages’s 50 Best Songs for Tax Day.

Don’t feel like you have to get your taxes done all in one sitting. If your return is simple (one W-2 and few 1099s) and you’re filing online, you might wrap it all up in an hour. But if there’s a lot of complexity in your finances, plan multiple shorter stints. Find chunks of time to:

- gather (and if necessary, download and print) official documents

- isolate and review all types of income

- isolate and review deductible expenses reflected on forms

- locate deductible expenses reflected on receipts (tangible and digital)

- fill in online tax preparation software like TurboTax or TaxCut, but then walk away and come back later to check your work; or

- make an appointment to sit with a professional tax preparer

Take frequent breaks to keep your mind fresh. Stay hydrated and have light, healthy snacks. When you finally finish, celebrate with a small ritual to reward yourself for all that adulting.

While I’m not always happy with the way my tax dollars are spent, I often find that the filing (if not the paying) of them goes down better with a listen to Irving Berlin’s WWII-era I Paid My Income Taxes Today. (The only version I found with Berlin singing it himself was a bit too jingoistic, so I present singing cowboy Gene Autry.)

GATHER YOUR RESOURCES

One of the most common frustrations my clients have is that they don’t know where to start. The fear of mysterious forms and documents starts the buzz of anxiety. I encourage a few simple steps for making the experience easier to bear.

Time Travel to Last Year

The easiest way to estimate what forms you’ll need this year is to start by looking at what you dealt with to prepare your taxes last year. You should have a folder with everything you (or your tax preparer) used to support last year’s tax returns. Scanning through last year’s taxes and supporting documents will help you create a checklist of what you’ll need for your treasure hunt.

Photo courtesy of Chris Potter/CCPix at www.ccPixs.com under CC 2.0

First, there’s the income side of things. Did you have a job? You’ll be looking for a W-2. Were you freelancing? Find those 1099s! Did you get paid interest or dividends? There will be 1099s for those, too.

Then, on the flip side, there are your expenses. You’ll have some fancy forms, like 1098s for interest paid on mortgages or tuition costs, but you’ll also need to gather receipts.

But that’s generally it, just what did you earn and what did you spend? (Obviously, not everything you spend is tax-deductible. The cheeseburger and fries you eat on your way home from the gym? That receipt can go. The one from when you took your best client to lunch to propose extending a contract? Hold on to that receipt!)

Answer Mail Call

In general, employers and financial institutions are supposed to mail tax documents like most 1099s and 1098s by January 31st, so you should have them in hand already. (Got a pile of unopened mail on top of the fridge? Now’s the time to open it!) Other forms, like 1099-B, 1099-S, and 1099-MISC don’t have to go out until February, so watch your mail. And, annoyingly, Schedule K-1 forms (related to partnerships, LLCs, and S-corps) generally don’t get mailed until early-to-mid March!

Don’t just think in terms of U.S. postal mail. Be sure to check your email, too!

I have quite a few clients, particularly those over 80, who don’t dependably check their email, and don’t necessarily realize that institutions have stopped sending paper copies of essential forms. Instead, they send emails alerting you to the existence of your forms in online portals.

If your inbox is full of hundreds or thousands of unread emails, try using the search bar for terms like “tax forms,” “1099,” or the word “tax” and the name of some of the institutions that should be sending you tax documents.

Let Your Fingers Do the Walking

Waiting for the official mail can be frustrating, especially if you are hoping to get a tax refund and want to get your taxes prepared and your return filed as soon as possible. In many cases, you don’t have to wait — just head to your keyboard, log in, download, and print.

For example, a client was recently frustrated with herself because she suspected that, in a fit of tidying the paperwork from last fall for enrolling in a 2026 health insurance plan, she’d accidentally shredded her 1095-A, her Health Insurance Marketplace Statement. Frustration turned to delight, however, when we logged into her Healthcare.gov account and quickly downloaded another copy.

Starting with your list of all of the institutions that have sent you tax documents in the past, and then adding any that know about your income/outgo, log in and search for a menu title like “tax forms” or “documents.” For example, log in to your:

- Bank accounts for 1099s

- Brokerage/investment accounts for 1099s

- Lender sites for 1098s

- Social Security for SSA-1099

- Health Insurance Company for annual summaries of medical and pharmaceutical expenses

- Paypal, CashApp, Venmo, Square, and similar platforms (for 1099-K and other records of income and expenses)

Remember that you may also have receipts that came to you by email. (If you haven’t gotten into the habit creating a “receipt” folder in your email or printing receipts for potentially deductible expenses, this is this is the time to start.)

Further, if you need to access information that’s on your prior tax returns and you don’t have them accessible — for example, if you’ve been the victim of a natural disaster, or you and an ex haven’t been able to amicably share data — you can get tax records and transcripts directly from the IRS.

Once you file your taxes, make a list of all the forms you received this year (and how/where you acquired them), and tuck that list into your tickler file for next January. Check off each form as it arrives, and you’ll have a better sense of when you’ll be ready to start working on your 2026 taxes in 2027.

KNOW YOUR FORMS

Much of the fear associated with tax time comes from the fact that the language referring to the different types of forms seems like gibberish.

Here’s a reminder of what each of the most common forms related to income and deductible expenses represent.

Let’s start with income.

W-2 (Wage and Tax Statement)

Were you an employee in 2025? If so, your employer should have provided one W-2 to you and one to the IRS, reporting how much you were paid (in wages, salaries, and/or tips). If applicable, the W-2 should should also indicate how much money was withheld (from you) and paid to another entity.

Federal, state, and local taxes, FICA (Social Security and Medicare), unemployment insurance, and a few other withholdings are considered statutory payroll tax deductions, because they are governed by statues (AKA: laws).

Sometimes, courts rule that an employee’s wages can be garnished (which sadly has nothing to do with caviar or sprigs of parsley). In these cases, individuals who owe money from lawsuits or are behind on child support may have money removed directly from their earnings, before it ever gets to their paychecks, to ensure it goes directly to whomever is owed. A W-2 will reflect this.

A W-2 may also report voluntary payroll deductions, amounts withheld from paychecks with your permission. Examples include your portion of health and life insurance premiums, contributions to a 401(k) or other retirement fund, employee stock purchasing plans, one-time or ongoing donations to the United Way, union dues, etc.

In theory, a W-2 should be mailed to the address listed on your W-4. (The W-4, is the form that tells your boss how much to withhold based on your number of dependents you have.)

Smaller companies may just hand you your W-2 instead of mailing or emailing it, but if your W2 is missing, consider:

- Did you change employers last year? You should have received W-2s from each employer. (If you changed jobs at the same company, you’ll receive one W-2 from each employer, not one per position. If you changed companies within a larger corporation, though, you may get one for each.)

- Did you change addresses since you filled out your W-4? There’s only so much a former employer will do to track you down to give you your W-2. Keep the Madge in HR updated!

Don’t assume that if you don’t have your W-2, then nobody knows what you made. Remember, your employer sends the IRS a copy of your W-2. Since the IRS knows what you made, be sure you do, too! (If your former company went out of business or is otherwise not returning your calls, the IRS has a procedure to help you file your taxes in the absence of a W-2.)

Examine your W-2 it carefully. Do the numbers seem right? Compare them to the final pay stub you got for last year. Calendar years may end mid-week (or even mid-pay period), so the numbers won’t correspond perfectly, but they’ll be close enough for you to spot if something is seriously wrong. The sooner you call your employer’s attention to an error, the sooner you can prepare your return.

W-2G (Certain Gambling Winnings)

Gambling Photo by Pavel Danilyuk on Pexels

The W-2G is the wild-and-wooly cousin of the W-2. While a W-2 is for money you make while working, the W-2G is what you get while playing. If you win more than $600 in any gambling session at a casino, the “house” should request your Tax ID (generally your Social Security number) and either prepare a W-2G on the spot or send it to you in January.

Casinos aren’t interested in keeping up with your losses, just your winnings, so they only tell the IRS about what they paid you. If you want to deduct losses to offset winnings, the IRS requires receipts, tickets, statements, or other records to support both your winnings and losses.

1099s

A 1099 is a form that basically says, “Hey, you weren’t an employee but we paid you money this year.” You get a copy; the IRS gets a copy. (Cue Oprah: “You get a copy! You get a copy! Everybody gets a copy!”)

There’s not just one type of 1099; actually, there are 22 different kinds of 1099s as of 2026! Don’t worry, you won’t be tested on this. But it helps to be familiar with some of the more common versions, like:

You may not have interest in 1099s, but 1099-INT reports the interest you receive — from interest-bearing savings and checking accounts, money market bank accounts, certificates of deposit, and other interest-paying. It also reports whether (U.S. or foreign) taxes were withheld and if there were any penalties assigned for early withdrawal from an interest-bearing account.

If you received less than $10 in interest, your bank may not send a 1099-INT.

Whether you’re TikTok’s viral man in finance, 6’5″, with blue eyes, and a trust fund or your grandma bought you one share of stock in Disney for your 10th birthday, you’ll get a 1099-DIV to indicate the dividends or capital gains you received as an investor. (Note: if you have a DRIP — a dividend re-investment plan — you many never see these dividends as checks sent to you. They’re literally re-invested in your portfolio.)

Again, if you didn’t earn at least $10 in dividends, you are unlikely to receive a 1099-DIV.

1099-G (Certain Government Payments)

This random-sounding form can cover everything from state unemployment compensation to tax refunds, credits, and offsets at the state and local level. It can also be used to report payment of taxable grants, agricultural payments, and other nifty things where a state or local government gives you money.

The 1099-K reflects payments to you from third-party settlement organizations (TPSO) like PayPal, Apple Pay, Venmo, or Zelle and platforms like Etsy or TikTok. This form was supposed to go into effect several years ago, but due to the pandemic, its use was delayed, and for several years, the threshold was $600, but has now been raised to $20,000 (and 200 transactions).

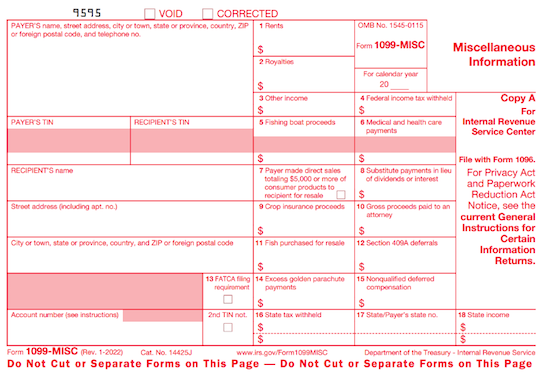

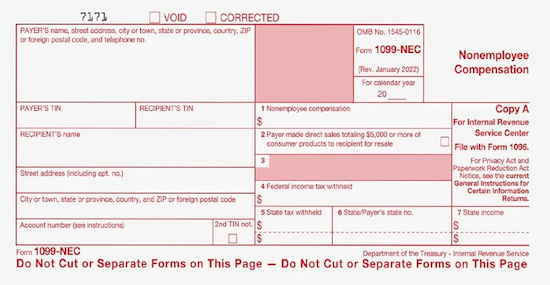

If you’re self-employed (a freelancer, an independent contractor, etc.), clients should send a 1099-NEC. However, although 1099-NEC came into use in 2021, some offices still send 1099-MISC by mistake. Just remember, whatever form you get, the IRS knows about it, so don’t try to hide that money.

Also remember that even if someone paid you for doing work as an independent contractor, they may not know they should be sending you a 1099-NEC or any form at all.

So, if you are self-employed or irregularly employed, it’s essential to keep track of your own incoming revenue. (Otherwise, if the person who paid you ever gets audited, it could trigger some messy situations for you, too.)

Now that the 1099-NEC covers income for freelances and independent contractors, this one is much more “miscellaneous.” As I’ve said before, it’s the junk drawer of tax forms!

1099-MISC is used to report payment of royalties, broker payments, certain rents, prizes and awards, fishing boat proceeds (yes, really!), crop insurance proceeds, and some payments to attorneys that wouldn’t be reported on a 1099-NEC, like if you received a settlement that required an attorney to get paid a portion contingent upon your winning.

If you get Social Security benefits, you should receive an SSA-1099. (Non-citizens living outside the US, like widows/widowers receiving spousal Social Security benefits, may get a SSA-1042.) The 1099-SSA tends to come on a weirdly long form, folded and sealed such that it makes its own envelope. Unfortunately, it looks like junk mail, so watch out for it and replace it, if necessary!

You Never Give Me Your Money, or Why Income Isn’t Always “Real” Money

A 1099 doesn’t always indicate that you were literally paid money. For example, remember how I said that you may get a 1099-DIV, even if you never actually got the dividend payment because it was re-invested?

Similarly, a 1099-C indicates that someone forgave a debt, like a student loan or a credit card balance. That forgiveness is a relief, but you may owe tax on forgiven debts, and the 1099-C alerts the IRS that since you didn’t pay money owed (and got to keep it), it’s as if you received money.

1099s May Be Hidden in Plain Sight

Sometimes, instead of sending a 1099 in a separate envelope, a bank or brokerage house may include a 1099 form in the same envelope — sometimes perforated at the bottom of a quarterly or end-of-year financial statement, or on the reverse side of a related form. Brokerage houses often send multiple forms as a “combined 1099,” scrolling across multiple pages.

Check all that boring-looking official mail!

Of course, income is only half of the equation. On the other side, you get to use forms and receipts to determine how much you can deduct or write off.

So, let’s look at expense documentation.

1098 (Mortgage Interest)

A 1098 is not a 1099 that’s been taking Ozempic. A vanilla, no-frills 1098 reflects the interest paid on a mortgage, which is generally deductible on federal taxes. Renters don’t pay interest, so they don’t get 1098s; neither do homeowners with paid-off mortgages.

Sub-types of 1098s reflect money you’ve paid for things other than interest on property loans:

- 1098-T shows tuition you paid; you’ll get this from a college or training school.

- 1098-E reflects you’ve paid interest on a student loan; it will come from your lender.

- 1098-C indicates the value of a donated car, boat or airplane. So, if you’re a fancy-pants, monocle-wearing Thurston Howell III or his wife, Lovey, you’ll get this from the agency or organization receiving the donation.

1095-A (Health Insurance Marketplace Statement), 1095-B, and 1095-C

You’ll get a 1095-A if you enrolled in health insurance coverage through a state or federal exchange.

1095-B (supplied by companies with fewer than 50 employees), details the the type of coverage you had through work, the period of coverage, and your number of dependents, so you can prove you had the Minimum Essential Coverage (MEC) required by law.

A 1095-C is similar, but for employers with more than 50 employees.

Schedule 1-A (Additional Deductions)

The Schedule 1-A, to be used with the 1040 return, the 1040-SR return (for seniors) and the 1040-NR (for non-resident aliens) is a new form for calculating some of the new deductions related tips, overtime, new purchases of cars manufactured in America and the enhanced deductions for seniors (see below).

Got all that?

IMPORTANT NEWS FOR THE 2026 TAX SEASON

Know Your 2026 Tax Deadlines

The federal tax deadline is Wednesday, April 15, 2026.

If you file a (valid) extension request, you have until October 15, 2026 to file your tax return. However, you still have to PAY what you (estimate that you) owe by April 15th to avoid a fine.

It’s true that if you won’t owe anything, there’s no penalty for filing late (without an extension), but then you’ll be delaying receiving a refund.

Age Has Its Advantages

Did you know that adults aged 65 and older may qualify for a new $6,000 deduction this year, in addition to existing standard deductions?

The deduction starts phasing out for single filers with incomes above $75,000 and for joint filers above $150,000. Once you hit the threshold, the deduction gets reduced by six cents on each dollar above the applicable threshold. Once your adjusted gross income hits $175,000 (for single filers) or $250,000 (for joint filers), the deduction is effectively reduced to zero.

This $6,000 deduction applies regardless of whether you take the standard deduction or choose to itemize. Also, it’s not permanent, applying only from this year through the 2028 tax year.)

Direct File Is No Longer An Option

A few years ago, I shared information about a government program that allowed people with simple returns (income solely from from employment, unemployment compensation, or Social Security, and only taking a standard deduction) to file directly with the government at no cost. The current administration has cancelled this program.

If you’re seeking a no-cost or low-cost way to file your taxes without working with a professional or filing through paid commercial software or online platforms, consider the following options for filing your 2025 returns:

- file out a paper form (often available in public libraries) or use IRS Free Fillable Forms

- see if you are eligible (depending on your adjusted gross income) to use IRS Free File and file through one of the eight online programs

- seek volunteer tax preparation programs like the Volunteer Income Tax Assistance VITA and Tax Counseling for the Elderly (TCE)

Don’t Procrastinate If You Plan to Mail Your Return

Filing tax returns at the last minute is a time-honored tradition. I’ve seen postal workers outside in the late hours, clad in reflective gear, taking possession of people’s returns.

Unfortunately, if you prefer to mail your tax return, filing on the last possible day may not be workable anymore.

At the end of last year, the US Postal Service announced that it was changing the methods for postmarking mail. They will still stamp the current day’s date on your tax return envelope, birthday card to your grandma, or care package to summer camp when they get to a USPS processing facility. The problem? It might take longer for your mail to get from where you give it to them to an actual facility.

Apparently the USPS is looking at ways to save money. One of those strategies includes reducing the frequency with which it picks up mail from local post offices. This means fewer trips from your drop-off point to a processing center, and THAT means it’s less likely that you’ll get a same-day postmark.

So, if you put your mail in your outside mailbox with the flag up, it could take a few days to get where it’s going. If you drop it in a blue maiilbox in front of a post office that isn’t a processing facility, it could take at least another day. Grandma may not care when an envelope is postmarked, but the IRS does. (And if you’ve got a deadline for mailing something for legal purposes, it definitely does.)

So, your mail may not get postmarked the same day you send it, even if you send it from a post office. That means that finishing your taxes at 11:30 p.m. and jumping in your car to head to the post office on the corner just isn’t going to cut it anymore.

Your best option is to file and pay your taxes online. But if you must mail your return, you may want to ask at your local post office if they are able to manually stamp and postmark your tax return.

While it will be more expensive, another option is to use a private shipper for your tax paperwork, like FedEx or UPS.

FINAL THOUGHTS

Paper Doll is a Certified Professional Organizer, not CPA or enrolled tax preparer. Always verify your questions with a tax specialist. If you receive a funky form and don’t know what to do with it, the IRS has a surprisingly easy Forms, Instructions and Publications Search.

Most importantly, remember that the sooner you get organized for tax time, the less likely you are to end up like Homer Simpson.

Call me crazy, but I actually enjoy tax prep. I’ve done it for many clients and for us.

At this point, the system I use to prepare our packet for the accountant is simple. Expenses and income get logged regularly into Quicken. I can pull year-end summary reports that add up receipts and categorize them for me. From there, I compile the pertinent info into a summary doc, gather the various forms and documents, and give it to our accountant.

Throughout the year, all tax-related documents (such as donation receipts and 1099s) go into a folder. When it’s time to gather papers, there is no hunting for anything.

It’s been years, maybe decades, that I’ve used Quicken. That was the game changer. No more adding up each receipt with a calculator. Although, honestly, I liked doing that. But it’s now it’s a more efficient and less time-consuming process.

I enjoy tax prep, too, but especially for clients because it’s an adventure figuring out what we need and where it might be (because I already know these things for my own taxes). It’s a treasure hunt!

I do my own taxes and my mother’s, as well, and then it’s not just a matter of what to search for, but how to answer the questions when they aren’t always clear. (Like, if you own stock in a company that’s financially managed in America, but you have to pay foreign tax, how do you answer the question as to whether you control a foreign financial asset?)

I’m glad Quicken is such a boon for you financial operations. Having the right tools and software makes such a difference! Thanks for reading!

My taxes are complicated. For one thing I get a widow’s pension from the UK that goes directly into my checking account and has no form. It varies each month as well since it is not paid in dollars.

This year will be the first year that Rob is not included.

Fortunately, my accountant puts together a worksheet form me.

Every year it seems like I am missing -not lost just missing- at least one form that I have to search online for and print off.

Sigh! I hate the process, but I can do it.

I do keep a red tax folder that everything goes into all year.

How strange that your pension has no document associated with it on an annual basis. That is frustrating! Even more frustrating is the variable amount. Does your bank have an app that lets you search by entity? This is the kind of thing where having a financial dashboard like the old Mint, or Empower or Monarch Money could make things easier, but if it’s only the one a month, I can see why doing it manually might be easier.

And yes, there’s always one random thing that doesn’t show up and needs to be chased down. It’s a shame that all entities don’t have to follow the same rules and deadlines.

Thanks for reading!

This whole topic makes me want to vomit. I think it is CRAZY that the process of paying taxes is so complicated. We truly incentivize people not to comply.

We use Quicken for our family finances, which makes the process easier. I’m lucky that my husband is on top of this stuff, and our accountant helps us do the best we can. Which isn’t very good, I’m afraid, when it comes to how much tax we pay. I feel like all we do is pay taxes.

Anyway… my main complaint is how some of our Schedule Ks arrive late every year, necessitating an extension every year. I feel like they should be required to get their forms out on time. I honestly have no idea what is involved on their end, so just speaking from my end.

I’m gonna pin this post for future reference to remember what everything is. Of course, since the landscape changes every year, you will just have to update this post every year LOL!

I get it; in other countries, they just send you a letter saying, “This is what we think you owe.” And then you either pay it or explain why not. You may see people in other nations (like on TV or social media) complaining about paying taxes, but never about filing them!

I completely agree about Schedule Ks; it’s very common for them to be delayed until September, so recipients have to get extensions. Why are they delayed? Because the partnerships aren’t organized to complete their own taxes, and the entity has to file its taxes before the Schedule Ks can be sent. Ugh!

And I do update this every few years, at least. The forms stay the same, but there are always new ones added. 22 different 1099s! (A quick trick? 1099s are for money you got paid; 1098s and 1095s are for money you paid. 1099 is the biggest number, so (hopefully) you make more than you spend!)

Thanks for reading and sharing your thoughts.

I’m with Seana. I get a stomachache just thinking about taxes. Luckily my husband does our taxes and I have a system that works well for organizing all financial data for my business and handing it over to my accountant.

I love that you included a list of all the forms and their uses.

Well, at least the most common forms. As I said, there are 22 different kinds of 1099s, and numerous other forms, not to mention worksheets.

It’s lovely that your husband does your taxes and that you have an accountant for the business, though I always recommend that people (especially women) make sure to review each of the line items to make sure they understand their purpose. (After all, when you sign a return, it’s a legal document.) I have no doubt your system for gathering the documents and data works well; we organizers always have a system! 😉

Thanks so much for reading!

Of course, this was posted right when I scheduled time to begin completing the CPA organizer. That makes it easier for me to ensure I don’t miss anything. However, your post was a helpful reminder. I find that using Quicken to create individual expense Category reports is a real time-saver. Thanks again, Julie!!!

I’m delighted to know that this was helpful, Michele.

Quicken and similar programs, as well as financial dashboard software, can make the tax prep experience go much smoother.

Thank you for reading!