Paper Doll’s 16 Ways To Organize Your Money In 2016 — Part 2

Your money has different personalities. Some just sit there like your college roommate’s freeloading boyfriend, drinking your milk and putting the empty carton back in the fridge. (Y’know, those investments you were talked into, but which have gone nowhere?) And some are delightful surprises, like friends who show up to drag you to the movies when you’ve had a bad day. (Think of that crisp $20 bill you find in your jeans pocket after doing laundry.) But your money won’t organize itself.

In Part 1 of 16 Ways To Organize Your Money In 2016, we looked at accessing and organizing the information others have about you in your credit report and credit score, and what you can do to improve your finances by tracking and making wise decisions about your expenses.

Today, we’ll look at more tips for keeping your money life in order.

6) Organize Your Financial Information

All the paper and digital information you have regarding your finances represents money going out (bills and statements for fixed necessities and variable luxuries) and money coming in (birthday checks from Grandma, your direct-deposit paycheck, investment interest and dividends). To keep control of your finances, to help you prepare your taxes, and to safeguard your financial future, it’s important for this information to be accurate and accessible.

The financial paperwork we receive or create usually breaks down into these sub-categories:

Outgoing Money

When you get a paper bill, you either tear off the stub to mail it back with your payment and keep the remainder, or you pay online and keep the whole statement/invoice. When I help my clients organize their financial information, we start by breaking the paper piles into categories:

- Monthly or periodic household bills (e.g., rent/mortgage, utilities, insurance, etc.)

- Credit cards statements

- Loans (e.g., home equity, auto, college, personal, etc.)

- Medical bills (which may be ad hoc or part of an ongoing payment plan)

- Anything else being paid on a regular or predictable basis (e.g., piano lessons, tuition, personal chef, professional organizer, fitness trainer) for which you wish to keep careful records

In this case, your basket is your financial information filing system. Usually, I advise this approach:

- Label (and alphabetize) tabbed interior folders within each sub-category. It doesn’t matter if you use generic terms (cable, power, water) or company-specific (Comcast, CityPower, Valley Water Authority) — just be sure to choose labels that reflect how you think. For credit cards, if you have more than one card from any one issuing company, you may want to put the last four digits of the card number on the label (Discover-1234, Amex-9876), just to help you file quickly. If your system is complicated, you’ll find excuses not to use it. Stay simple.

Group related sub-categories in hanging files in a filing cabinet, milk-style file crate, or desktop file box. - File the backlog in reverse-chronological order.

- File paper bills as you pay them.

Alternatives to file folders are three-ring binders and accordion folders. However, binders require three-hole punching of papers, and each additional step leads people to procrastinate. Accordion folders can work for college students and those with very few expenses, but a system you can expand as your financial complexity increases will be easier to maintain.

If you get all your bills and statements digitally, there’s no need to print them out; just set up a new behavioral system to acquire the information, label it, and store it.

You can manually download each statement, or use FileThis, an app/service which, once linked to your account, fetches your online statements and bills so you can pay them and store them as you see fit. Let everything live in the FileThis Cloud, on your computer, or in Evernote, Box, Dropbox or Google Drive. (FileThis ranges from free to $5/month, depending on your needs.)

You can manually download each statement, or use FileThis, an app/service which, once linked to your account, fetches your online statements and bills so you can pay them and store them as you see fit. Let everything live in the FileThis Cloud, on your computer, or in Evernote, Box, Dropbox or Google Drive. (FileThis ranges from free to $5/month, depending on your needs.)

To create a uniform digital system for labeling (for example, bill name and date, like Verizon-2016-1). Some people prefer to keep all of the digital invoices in one online folder and use search to find what they want; others (like Paper Doll) prefer a folder hierarchy system that matches the one described above for paper.

Finally, while some people refute the idea of maintaining bills once they’ve been paid, I suggest it for a couple of reasons. First, many companies only provide access to a limit period of billing, sometimes only a year or six months, making it difficult to source errors or track information. Second, for those who tend to be disorganized with their finances, a tangible (paper) system yields a greater sense of control.

Incoming Money

Incoming revenue information may involve pay stubs from employment, alimony or child support payments received, Social Security income, disability payments, IRA disbursements, personal loan repayments (to you), lottery winnings, and stock dividends (if not part of a dividend reinvestment plan). If you’re regularly getting money from any source, or have gotten a large lump sum for something other than employment, make a folder (or folders) to maintain records until tax time.

Transitional Money

The above categories talk about what you are doing to your money, but others show what your money is doing, with or without you. Bank statements for checking, savings, and trusts represent collections of funds in transition. They may accrue interest or have fees associated with them, so take time each month to make sure these accounts reflect what you think they should.

Brokerage statements contain investment information. Sort these by investment type: retirement, college savings, goal-related (like a vacation fund), first, and further sub-categorize (and alphabetize) by company or specific investment. So, in the Retirement hanging folder, you might have interior folders for your 401(k), an old 403(b) that remains in place, IRAs with Fidelity or Vanguard, and so on. Each account should have its own folder.

Simulated Money

Some of your records represent money that’s not real yet. These files might include quarterly or annual statements reflecting either regular or atypical benefit plans for your job, such as if you’re vested in an employee stock ownership plan. If you’re not particularly active in managing this information, maintaining it in digital form will keep you from getting overwhelmed.

You can also have a folder in this section for gift certificates, gift cards and store credits so you can keep track of the money value owed to you. If you prefer to keep them portable, a Card Cubby is a nice alternative to mixing them into your financial filing.

Keep stock certificates, bearer bonds, or other papers of significant value in your safe deposit box or fire-proof safe.

7) Create Tax Prep Folders (for the tax year just ended and for the one to come)

Depending on your financial situation, one folder per year might suffice; if your financial life is complex, you might want a handful of folders for each year’s incoming tax forms, charitable donation receipts, medical expense annual summaries from your insurance company, etc. Create a safe place for incoming papers to land and you’ll be ahead of the game.

Any day now, you’ll start receiving official-looking forms (1098s to indicate interest income you’ve paid on certain loans, 1099s to show interest, dividends, and other payments to you, W2s from employers, etc.) to help you prepare your taxes for last year. To get an idea of the forms to expect, these tax-related Paper Doll posts will walk you through it:

Taxing Conversations: Organizing the Essentials & a New Tax Tool

Taxing Conversations (Part 2): Organizing Fun With Forms

Taxing Conversations (Part 3): Form-Free Organizing

Securing these documents (plus any items that pop up when you’re following the steps in #6, above) will make tax time run much more smoothly, whether you file on your own or use a preparer.

8) Organize a (Socially) Secure Future

Cleaning up your credit history will organize your past; getting a handle on your expenses, financial paperwork, and taxes will take the wobble out of your financial present. But what about your future? Banking (if you’ll pardon the pun) on Powerball isn’t going to do it.

There are numerous ways for minimizing taxes and maximizing your odds for a financially secure future, and if you don’t have one or more of the alphabet soup of IRAs, 401(k)s or 403(b)s, you should be talking to a financial advisor about how to get started. But whatever your retirement plan, there’s one program in which you’re probably already participating (unless you work for the railroads): Social Security.

Start by signing up for your online Social Security account, as I’ve been pestering you about since Paper Doll Makes a Statement: The Social (Security) Network.

If you haven’t yet signed up yet, go to the my Social Security website and click on Create An Account. Once you create your account, you’ll be able to track your earnings and verify that they’ve been properly reported (by you and/or your employer), and get estimates of your future benefits. If you’re already receiving benefits, accessing your account enables you to obtain a letter with proof of benefits (often needed for legal and financial purposes), change your address and direct deposit payment information, and manage your benefits.

If you have already set up your account, change your password! The Social Security Administration actually makes you do what you’re already supposed to do — update your password every six months. If you haven’t, it’ll prompt you to do so when you log in.

Speaking of Social Security, take your card out of your wallet or purse — you shouldn’t be carrying it around with you.

As we talked about in What’s In Your Wallet (That Shouldn’t Be)?, in the wrong hands, your Social Security card is an invitation to identity theft and financial fraud. Memorize your number for when you have to unexpectedly fill in forms. (Really, it’s like a phone number, just nine digits.) Put the actual card in your VIP (very important paper) file system or in your fireproof safe, and only pull it out when you need it.

As we talked about in What’s In Your Wallet (That Shouldn’t Be)?, in the wrong hands, your Social Security card is an invitation to identity theft and financial fraud. Memorize your number for when you have to unexpectedly fill in forms. (Really, it’s like a phone number, just nine digits.) Put the actual card in your VIP (very important paper) file system or in your fireproof safe, and only pull it out when you need it.

Can’t find your Social Security Card? Report it, especially if you think you’ve been the victim of identity theft, and then replace it.

9) Save for More Than Retirement: Cheating the Obstacles to Willpower

I know, I know. Saving isn’t sexy. But a beach vacation is. And not having to go into credit card debt to pay for next year’s Christmas presents is an idea that gets the blood flowing. But saving is difficult. Usually, in order to save money, you have to use up all your reserves of willpower to keep from spending it in the first place.

What’s willpower, really? Psychologists have defined it as the ability to delay gratification, resisting short-term temptations in order to meet long-term goals. But the more you delay gratification, the more worn-down and put-upon you can feel.

So, why not do an end-run around willpower? Automate! No, you don’t need to be a robot; you just need to take the ongoing decision-making (to put money aside) out of the equation. Make the decision once and be done with it.

Remember last time, in step #5, you audited your expenses and figured out what bills you could lower? Let’s say you lowered your monthly entertainment expenses by $18 and your phone/communication bills by $11, and maybe eliminated a few other ongoing items by about $15 a month. On their own, that may seem a pittance, but that’s $44 every month. Set up an automatic transfer from your checking to your savings account for $11 per week.

Of course, even if you haven’t identified ways to pare down your spending, as long as you’re not at risk of falling into the red, having small amounts automatically transferred to savings on a regular basis is a way to improve your savings rate without feeling you’re being denied life’s pleasures.

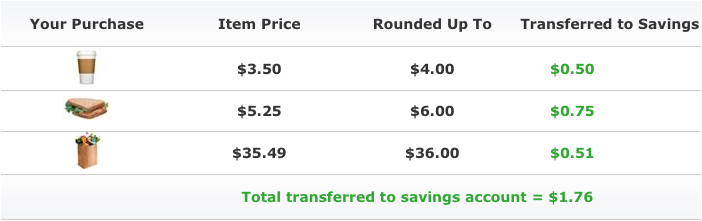

There are other automated savings options. Bank of America’s Keep the Change Program helps its customers save by rounding up each debit card purchase to the nearest dollar, and sequestering that extra money in savings but allowing you to track the movement of money via online banking. For example:

Prefer a little more tech support? The Digit web service works similarly. Once you link Digit to your checking account, it analyzes your spending patterns, predicts your cash flow, and transfers small but varying amounts of your money to your Digit account in an FDIC-insured bank.

You won’t earn interest, but whenever you want your money, just text Digit, and the money can be transferred back to you, so you could wait until you reach a benchmark amount, like $500, and then transfer that to savings.

Digit sends one text each day to let you know your new checking account balance; it can also text you how much your bank balance has changed over the prior two days, and can list all your debits from the prior day. The more you use it, Digit not only helps you save, but also gain more awareness of your spending habits. Isn’t that organized?!

Still to come in this series: organizing to get out of debt, streamline getting paid, using technology to achieve your financial goals, and more!

Paper Doll Post:

I have never thought about signing up on the Social Security website. Thanks for that information. I will be looking into that soon.