Paper Doll’s 16 Ways To Organize Your Money In 2016 — Part 3

Whether it’s that shiny nickel that burns a hole in your Garanimals pocket at age 5 or the wallet overflowing with wrinkled receipts or a hot mess of old abandoned 401(k)s that have never been rebalanced or rolled over, money can be a source of pleasure or pain. This series on organizing your finances is designed to give you some actionable ideas for gaining more control over your money in 2016. Review the first nine strategies in Part 1 and Part 2, and continue with today’s money-organizing tips.

10) Organize yourself out of debt.

“Annual income twenty pounds, annual expenditure nineteen [pounds] nineteen [shillings] and six [pence], result happiness. Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery.” ~ Charles Dickens, David Copperfield

It might seem as though getting out of debt would have little to do with organizing — perhaps you think it’s solely a matter of making more money or spending less. In theory, both of those things should help you get out of debt; in reality, humans are irrational. To get ahead on your debt repayment, you’ll need to add a little rationality to your approach:

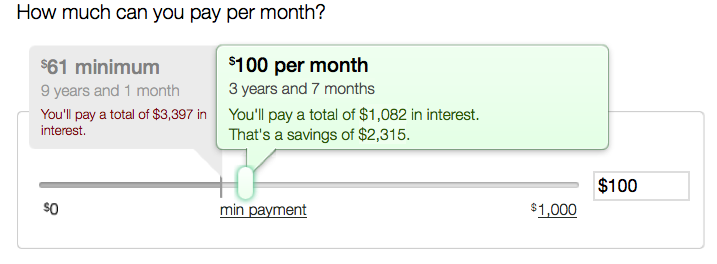

- Stop paying only the minimums — Recognize that just because your bill tells you that $34 is the minimum you have to pay doesn’t mean that’s what you should pay. The less you pay each month, the more interest you’ll pay over time, and the longer it will take you to pay off your debt. It’s in each lender’s interest for you to pay as little as possible beyond the minimum, because it keeps you indebted (and them in business), and because the minimums are so small, they seem inconsequential, leading you to take on more debt. Obviously, your goal is to pay off all unsecured, revolving debt each month; if you can’t, at least throw as much money at your debt as possible.

- Let your right hand know what the left hand is doing — If you have money in savings or investments earning low interest, but credit card or other debt at high interest, consider applying the former to the latter. If you’re earning less than 1% on $1000 but racking up interest at 13% on $1000 in credit card debt, you are losing money. Of course it’s always important to have a liquid (that is, accessible) financial cushion for emergencies, but letting debt pile up each month while low-earning funds wallow, you may be penny wise but pound foolish. Make sure your savings/investing brain is talking to your debt-payment brain by getting a reality check; use the National Foundation for Credit Counseling “Debt or Invest” calculator to see where your money will best serve you.

- Make sure your head and heart converse — Being rational is important, but if you’re in a constant struggle against your instincts, it will be hard to stick to a repayment plan. Pull up your most recent statement for every credit card and take note of the interest rates. If you have three credit cards, for example, you might have three different amounts at three different rates. Now that you’re not paying merely the minimum, you might be tempted to take the total amount you’ve earmarked to pay off debt and divide it equally among those three credit cards every month. Not so fast! There are better methods that work, either logically or psychologically, and both have advantages and disadvantages.

The Snowball Method — With this strategy, you pay the minimum on all debts except the smallest, and throw all the rest of your budgeted debt-reduction funds toward paying off that smallest debt. Armed with this bit of success, you’ll rebalance your efforts and take all the money you’d been putting against the smallest balance, and now apply it (plus what you were already applying) to the next-lowest balance, and so on. This method has a psychological reward — by focusing on the smallest debt owed, you’ve got something in your “win” column to motivate you to stay committed to the plan. But it’s not particularly logical — by focusing on balances rather than interest rates, your total debt keeps growing.

The Debt Avalanche Method — Line up your debts by interest rate, pay the minimum toward all but the highest-rate debt, and put all of your available money (salary, birthday money, funds raised from selling your books or your plasma, etc.) toward the highest rate debt. This method is logical, but it lacks the immediate sense of victory of the Snowball Method.

Still not sure how much to put toward your individual debts? There are some great no-cost debt calculators available to help you, including:

Mint — If you’re using Mint as a complete financial dashboard service, its Financial Goals feature is ideal for paying off specific debts — one or many. Once you sync the service with your accounts, you can select which accounts you want to include in your debt payoff goals. Mint will already know your interest rate and minimum payment, and will display how your payoff options will impact interest owed over time.

As you make monthly payments, because Mint will already be tracking your money, the system will display how you’re progressing toward your monthly goal (telling you, for example, that you’ve paid “$73 toward your goal of $200 for the month) and how you’re progressing toward your overall goal.

If you have multiple types of debt, like personal debt, business debt and medical debt, you can create multiple goals and view them separately or on one screen. However, note that the goals element of the dashboard service is only viewable from a browser, not from the Mint app.

Ready for Zero — As with Mint, once you sync all of your accounts, Ready for Zero knows your account details: balance, minimum payment, interest rate, etc., and auto-updates when you make payments, add debt, etc. It has similar sliders for setting your approach to your goals, but Ready for Zero’s app seems to be more seamlessly integrated with the browser version, and overall, offers much more variety of display views and reminders. If visual feedback helps you stay motivated, this is a great option.

Of course, if you’re experiencing crushing debt, organizing your information and game plan is just one aspect of financial recuperation. Debt counseling is an important option, but there are a variety of predatory and/or irresponsible so-called debt counselors out there. Begin your search with the National Foundation for Credit Counseling to find an NFCC-Certified Consumer Credit Counselor.

11) Lower Your Interest Rates

You can’t walk into Target and tell the cashier you’d like a discount on toothpaste, or warn the front desk clerk at your hotel that you’d prefer to pay only one-third the hotel tax. You can’t just ask for better deals! Or can you?

There’s little chance of getting your bank to bump your measly .087% savings account interest rate up to 5%, let alone double-digits. That’s just not how banking works. But credit card interest rates are more complex. Sure, the rate you’re charged is dependent upon your credit history, credit score and earning power, but the credit card industry is highly competitive. If you have an unblemished payment history and have been a solid customer, you can try to request a better interest rate.

First, log into your online account for each lender and see if there are already options for things like changing your payment date, requesting a higher credit limit, or getting a lower interest rate. (Don’t get a higher limit for ego’s sake; you don’t need it.) You may be able to handle this with a few clicks. If not, call your lender, be cheerfully polite, and once you’ve identified yourself with your name, account number and all matter of ridiculous levels of proof, tell the representative something like:

I’ve been a loyal customer of [credit card company], pay my bills on time and have been generally happy, but I’ve been receiving offers in the mail from other credit card companies with lower APRs. To be as financially responsible as possible, I want a lower rate on my card. Before I cancel my card with [your company] and switch, I wanted to see what you could do to help me.

And then shut up. You might get a grumpy rep and a rejection, or you might get good news. Either way, you’re out nothing except your time.

If requesting a change in interest rate from your own lender doesn’t work, you can always initiate a balance transfer, either to one of your other cards or a new credit card, for 0% or a very low rate, but balance transfers come with their own caveats:

- There are fees attached, usually 2-5% of the value of the transfer; this fee is added on top of your transferred debt and is subject to the same interest rates that apply to the transferred amount.

- These are short-term interest reduction periods, usually for 9-18 months; any unpaid debt as of the end of the transfer period will be charged interest at whatever the card’s normal rate might be.

- You should only transfer debt to cards that already have a zero balance, and do not charge new purchases on the card until the transferred debt is paid off. Otherwise, with multiple concurrent interest rates on one card, your progress towards repayment will be muddied.

12) Ask and Ye Shall Receive…Better Deals and Discounts

If you’ve ever seen those long, convoluted blog and Facebook posts about extreme couponing, you may think you don’t have what it takes to lower your costs. However, getting good deals doesn’t have to be complicated. Whether you’re trying to buy something at a lower price or reduce the cost of a service for which you’re already paying, try these options:

Let your fingers do the walking. The next time you’re going to buy something online, stop at your favorite search engine first and type in “[name of store where you’ll be shopping anyway] discount” and you’ll be amazed at the number of coupon code sites that will pop up, including:

From free shipping to percentage discounts, it often takes no more than a few extra minutes to find a rewarding promotional code to use at checkout.

Ask for a better rate. Using the same kind of script described above for lowering your interest rates, call your phone or cable company, or similar service provider, and explain that you’ve been a loyal customer for [X number of] years, have been offered discounts by other providers, or have seen lower rates and inducements the company has offered to new customers, and ask what can be done to keep you happy.

Ramit Sethi of I Will Teach You To Be Rich walks through how to have these kinds of conversations with confidence.

In 2014, NPR’s This American Life did an interesting segment on the concept of the “Good Guy” discount — and how sometimes, just asking for a price break can work. What could it hurt?

Threaten (politely) to cancel your service. This is the next level up from merely asking. It takes a little more aplomb, and may require you asking to get transferred to the Retention Department, but state your case, reference competitor pricing, and then be quiet. At first, they will inevitably try to up-sell you to services you don’t want or need. But stand your ground and it’s more likely that not that you’ll be offered six months or more of discounted service. I have one client who merely calls to cancel her satellite radio service every time she’s billed and achieves a discount in return for her few minutes of effort; with many of my clients, we set aside a “canceling” session a few times a year to see how many discounts we can get.

David Bach, better known for his Finish Rich financial advice empire, wrote a great book a few years ago called Fight for Your Money: How to Stop Getting Ripped Off and Save a Fortune. It’s a superior resource for developing the skills necessary to master a system that’s gamed in favor of large companies.

Too anxious to talk to reps personally? That’s OK, as you can use the same approach online. You’ll often find that if you go into your online account for an entertainment, dating, or gaming service (e.g., Hulu, Netflix, Match, X-Box Live) and “cancel” your account, you’ll get a pop-up notice offering a discount if you’ll keep your account active. Sometimes, the cancelation will go through, but you’ll receive an email within the day, inducing you to reactivate.

And, of course, you can put any of your newfound windfall toward debt-reduction or savings goals!

Next time, in the final post of this series, we’ll look at ways to organize how you get paid, how to make your spending habits boost your return on investment, and fun options to learn more about mastering your money.

Follow Me